Quick summary: If you are a salaried individual, freelancer, or HUF paying monthly rent of more than ₹50,000 to a landlord, the law requires you — the tenant — to deduct TDS from the rent, deposit it with the government, and then issue a TDS certificate called Form 16C to your landlord. This rule, under Section 194-IB of the Income Tax Act, 1961, surprises many urban tenants who have never had any TDS obligation before. The TDS rate is currently 2% (reduced from 5% by the Finance Act (No. 2), 2024, effective 1 October 2024). You do not need a TAN to comply — your PAN is sufficient. This article explains the entire process, step by step.

What Is Form 16C?

Form 16C is a TDS (Tax Deducted at Source) certificate issued by a tenant to a landlord as proof that TDS has been deducted from the rent paid and deposited with the Central Government. It is issued under Section 194-IB of the Income Tax Act, 1961, read with Rule 31AA of the Income Tax Rules, 1962.

The concept is straightforward: just like an employer deducts TDS from your salary and issues you Form 16, and just like a bank deducts TDS from your FD interest and issues you Form 16A — when you, as a tenant, deduct TDS from the rent you pay, you must issue your landlord Form 16C as their official proof of that deduction.

For the landlord, Form 16C is important because it allows them to claim the TDS as a credit when filing their own ITR — reducing or offsetting the tax they owe on rental income. Without it, the landlord may end up paying tax on income for which TDS has already been deducted and deposited.

Who Needs to Deduct TDS and Issue Form 16C?

Section 194-IB applies to any individual or Hindu Undivided Family (HUF) tenant who:

- Is paying rent to a resident landlord (not an NRI)

- Is paying rent that exceeds ₹50,000 per month (or part of a month)

- Is not required to get their accounts audited under Section 44AB of the Income Tax Act (i.e., is not a business or professional with high turnover)

This covers a very large category of urban tenants — salaried employees, freelancers, consultants, and HUFs who rent homes or office spaces at a premium. If you live in a metro city and pay ₹55,000, ₹80,000, or ₹1,00,000 a month in rent, this law applies to you.

Who Does NOT Fall Under Section 194-IB?

Companies, partnership firms, LLPs, trusts, and individuals or HUFs who are required to have their books audited under Section 44AB — these entities deduct TDS on rent under a different section, Section 194-I, using a different form. Section 194-IB is specifically and only for individual and HUF tenants who are not in that audit category.

Similarly, if the rent you pay is ₹50,000 or less per month, Section 194-IB does not apply — no TDS, no Form 16C required.

Does It Apply to Both Residential and Commercial Rent?

Yes. Section 194-IB applies to rent paid for both residential and commercial properties — flats, houses, offices, shops — as long as the monthly rent exceeds ₹50,000 and the other conditions are met.

The TDS Rate Under Section 194-IB

The current TDS rate under Section 194-IB is 2%, applicable from 1 October 2024 onwards. This was reduced from the earlier rate of 5% by the Finance Act (No. 2), 2024 (Union Budget 2024). For all rent payments or credits made on or after 1 October 2024, TDS must be deducted at 2%.

So for FY 2025-26 (April 2025 to March 2026), the applicable rate is 2% for all tenants whose last-month rent deduction falls after 1 October 2024 — which means effectively all tenancies running through FY 2025-26.

If the landlord does not provide their PAN: TDS must be deducted at 20% (under Section 206AA), subject to a maximum of the rent payable for the last month of the financial year. This is a very steep rate — always collect your landlord’s PAN before the tenancy begins.

GST exclusion: If the landlord charges GST separately on the rent (applicable where the landlord is GST-registered and the property is used for commercial purposes), TDS should be deducted only on the base rent amount, excluding the GST component.

The Key Timing Rule: TDS Is Deducted Once a Year

This is the most important feature of Section 194-IB that distinguishes it from most other TDS provisions: TDS on rent is deducted only once in a financial year — not monthly.

The deduction happens at the time of:

- Payment or credit of rent for the last month of the financial year (i.e., March rent, for a tenancy that continues through the year), OR

- Payment or credit of rent for the last month of tenancy, if you vacate the property before the financial year ends — whichever is earlier

This means if you pay ₹60,000 monthly rent from April 2025 to March 2026 (12 months), you do not deduct TDS every month. Instead, you deduct 2% of the total annual rent in March 2026 (when you pay the last month’s rent), and that one deduction covers the entire year.

Example: Ravi pays ₹70,000 per month in rent from April 2025 to March 2026.

Total annual rent = ₹70,000 × 12 = ₹8,40,000

TDS to be deducted in March 2026 (at the time of paying March rent) = 2% × ₹8,40,000 = ₹16,800

Ravi pays his landlord ₹70,000 − ₹16,800 = ₹53,200 for March, and deposits ₹16,800 as TDS.

One important cap: The TDS deducted cannot exceed the rent payable for the last month of tenancy. If the TDS calculated on the full annual rent exceeds the last month’s rent, it is capped at the last month’s rent. In most normal situations, 2% of 12 months’ rent is well within the last month’s rent.

What if you vacate mid-year? If you vacate in, say, October 2025, you deduct TDS in October (the last month of tenancy), calculated on the total rent paid from April to October 2025.

Pro Tip: Use our FREE TDS calculator to know how much TDS to pay.

Form 26QC: The Step That Comes Before Form 16C

Similar to property transactions where Form 26QB precedes Form 16B, here you must first file Form 26QC before you can issue Form 16C to your landlord.

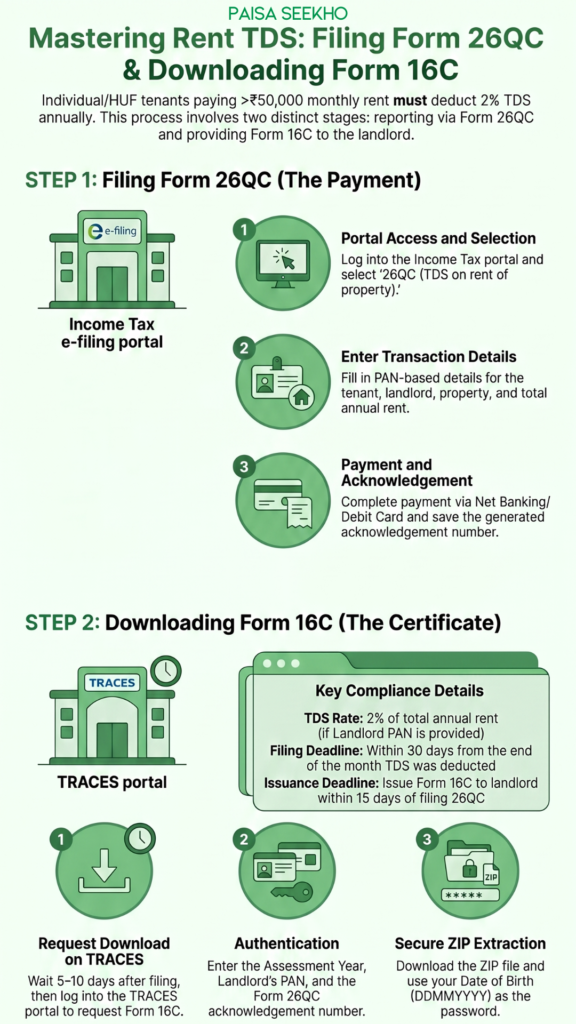

Form 26QC is a challan-cum-statement — it combines the TDS return with the payment in a single online form. It is filed on the Income Tax e-filing portal (incometax.gov.in) and simultaneously reports the rent transaction and deposits the TDS with the government.

Think of it this way:

- Form 26QC = the payment + report you send to the government

- Form 16C = the proof/certificate you then download from TRACES and give to your landlord

Due Date for Filing Form 26QC

Form 26QC must be filed within 30 days from the end of the month in which TDS was deducted. Since TDS is usually deducted in March (the last month of the financial year), the due date is typically 30 April of the following year.

For example: If you deducted TDS in March 2026, Form 26QC must be filed by 30 April 2026.

If you vacate mid-year: TDS is deducted in the last month of tenancy, and Form 26QC is due within 30 days from the end of that month.

How to File Form 26QC (Step-by-Step)

- Log into the Income Tax e-filing portal (incometax.gov.in) using your PAN and password.

- Go to e-File → e-Pay Tax → New Payment and select 26QC (TDS on rent of property).

- Fill in the form with the following details:

- Tenant details: Your name, PAN, address, and contact information

- Landlord details: Name, PAN, and address (PAN is mandatory; without it, TDS is at 20%)

- Property details: Address of the rented property

- Rental period: Start and end date of the tenancy for which TDS is being deducted

- Total rent paid: The aggregate rent for the full period (not just the last month)

- TDS amount: 2% of total rent paid (or as applicable)

- Date of deduction

- Choose your payment mode — net banking, debit card, etc.

- After successful payment, an acknowledgement number is generated. Save this — you’ll need it to download Form 16C.

No TAN required. Tenants deducting TDS under Section 194-IB are specifically exempted from obtaining a TAN. Your PAN is sufficient to complete this entire compliance chain.

Multiple Landlords

If the property is owned by more than one person (e.g., two co-owners sharing the rental income), the tenant must file a separate Form 26QC for each co-owner based on their respective ownership share or as specified in the rental agreement.

How to Download Form 16C from TRACES

Once Form 26QC is filed and processed (allow 5 to 10 working days), you can download Form 16C from the TRACES portal (tdscpc.gov.in).

Step-by-step:

- Go to TRACES (tdscpc.gov.in) and log in or register as a taxpayer using your PAN.

- Navigate to Downloads → Form 16C.

- Enter the Assessment Year, your landlord’s PAN, and the acknowledgement number from your Form 26QC filing.

- Submit the request and check status under Downloads → Requested Downloads.

- Once status shows “Available,” download the ZIP file. The password to open it is your date of birth in DDMMYYYY format.

- Print the Form 16C PDF or share it digitally with your landlord.

Due date for issuing Form 16C: Within 15 days from the due date of filing Form 26QC. So if Form 26QC was due by 30 April, Form 16C must be given to the landlord by 15 May.

What Does Form 16C Contain?

As confirmed by the Income Tax Department’s TRACES portal, Form 16C contains:

- Name and address of the tenant (deductor)

- Name and PAN of the landlord (deductee)

- Assessment year

- Nature of payment (rent)

- Address of the rented property

- Total rent paid during the financial year

- Amount of TDS deducted

- Date of deduction and date of deposit with the government

- Challan details confirming the TDS payment

- A unique TRACES certificate number

Like all other TDS certificates in this series, a Form 16C prepared manually — without a TRACES certificate number and watermark — is not a legally valid document.

Section 194-IB vs Section 194-I: Which Applies to You?

One of the most common points of confusion is the difference between Section 194-IB and Section 194-I. Both deal with TDS on rent, but they apply to completely different categories of tenants.

| Section 194-IB | Section 194-I | |

| Who deducts TDS | Individual/HUF tenants NOT liable to tax audit | Companies, firms, trusts, and individuals/HUFs liable to tax audit |

| Threshold | Monthly rent > ₹50,000 | Annual rent > ₹6,00,000 (₹50,000/month effective from FY 2025-26) |

| TDS rate | 2% (from 1 October 2024) | 2% (plant & machinery); 10% (land, building, furniture) |

| TDS form | Form 26QC | Quarterly TDS return (Form 26Q) |

| TDS certificate | Form 16C | Form 16A |

| TAN required? | No — PAN is enough | Yes |

| When deducted | Once a year (last month’s rent) | Monthly/periodically |

If you are a salaried employee, a freelancer, or run a small business that doesn’t go through tax audit, and you pay rent above ₹50,000 a month, you fall under Section 194-IB — and Form 16C is your responsibility.

Penalties for Non-Compliance

Missing TDS compliance on rent can be costly. Here is what the Income Tax Act prescribes:

| Default | Consequence |

| Failure to deduct TDS | Interest at 1% per month from the date it should have been deducted until the date of actual deduction |

| Deducting TDS but not depositing it | Interest at 1.5% per month from the date of deduction to the date of deposit |

| Late filing of Form 26QC | Late fee at ₹200 per day under Section 234E (capped at TDS amount) |

| Non-filing or incorrect Form 26QC | Penalty of ₹10,000 to ₹1,00,000 under Section 271H |

| Late issuance of Form 16C | Penalty at ₹100 per day under Section 272A(2)(g) |

Beyond financial penalties, a tenant who fails to deduct TDS when required may be treated as an assessee in default under Section 201 — meaning the tax department can demand the TDS directly from the tenant, along with accumulated interest.

What the Landlord Should Do With Form 16C

If you are the landlord receiving Form 16C from your tenant:

- Check the details: Verify that your PAN, the rent amount, the property address, and the TDS figure are all correct.

- Cross-check with Form 26AS / AIS: Log into the Income Tax portal and check whether the TDS appears in your consolidated tax credit statement. Allow about 7 to 10 days after the tenant files Form 26QC for it to reflect.

- Claim TDS credit in your ITR: When filing your income tax return, report the rental income under Income from House Property (or under the relevant head) and claim the TDS credit in Schedule TDS-2. This credit reduces your final tax payable.

- If TDS is not reflecting in Form 26AS: Contact your tenant immediately. Only the tenant can fix this by filing a correction on the portal. A mismatch cannot be resolved by the landlord alone.

Remember: Even after TDS is deducted, the landlord must report the full gross rent in their ITR (not the net amount they received after TDS). The TDS simply means a portion of the tax has already been paid on their behalf.

Practical Situations: Common Scenarios Explained

- Scenario 1 — You pay ₹45,000 per month: Section 194-IB does not apply. Rent is below ₹50,000/month. No TDS, no Form 26QC, no Form 16C required.

- Scenario 2 — You pay ₹65,000 per month for the full year: Section 194-IB applies. Deduct TDS in March at 2% of total rent: 2% × (₹65,000 × 12) = ₹15,600. File Form 26QC by 30 April. Issue Form 16C to landlord by 15 May.

- Scenario 3 — You pay ₹60,000 per month but vacate in November: TDS is deducted in November (last month of tenancy) at 2% of total rent paid (April to November = 8 months): 2% × (₹60,000 × 8) = ₹9,600. File Form 26QC within 30 days of November-end (by 30 December). Issue Form 16C by 14 January.

- Scenario 4 — Landlord refuses to give PAN: TDS must be deducted at 20%, subject to a cap of the last month’s rent. On ₹70,000 monthly rent (12 months total = ₹8,40,000), 20% TDS = ₹1,68,000 — but capped at ₹70,000 (last month’s rent). Strongly advise landlords to share PAN to avoid this situation.

- Scenario 5 — Two co-owners share the rental income: File a separate Form 26QC for each co-owner based on their share. Two separate Form 16C certificates must then be issued, one to each co-owner.

Important: Form 16C Is Becoming Form 132

Under the Income Tax Act, 2025 (effective from 1 April 2026) and the Income Tax Rules, 2026, Form 16C is being merged into a new unified certificate. According to the Income Tax Department’s official FAQ:

- Form No. 132 replaces Form 16C (along with Forms 16B, 16D, and 16E) from Tax Year 2026-27 onwards

- The underlying provision shifts from Section 194-IB (old Act) to Section 393(3) [Table: S.No. 2(ii)] of the new Income Tax Act, 2025

- Form 26QC is merged into Form 141 (Schedule B/C)

- Form 132 must still be downloaded from TRACES and issued to the landlord within 15 days of the Form 141 due date

- The threshold (₹50,000/month) and general compliance steps remain the same

For FY 2025-26 (rent paid up to March 2026): continue using Form 26QC and issuing Form 16C as described in this article.

From Tax Year 2026-27 (rent from April 2026 onwards): use Form 141 and issue Form 132 to your landlord.

Frequently Asked Questions

1. I pay ₹55,000 rent per month. Does Section 194-IB apply to me?

Yes, if you are an individual or HUF tenant not liable to tax audit. The ₹50,000/month threshold is crossed, so you must deduct 2% TDS and comply with Form 26QC and Form 16C obligations.

2. Do I need to deduct TDS every month?

No. Under Section 194-IB, TDS is deducted only once in a financial year — at the time of paying or crediting the rent for the last month of the year (typically March) or the last month of tenancy if you vacate early.

3. I am a salaried employee with no business. Do I still need to follow this?

Yes. Section 194-IB applies to individual tenants regardless of whether they are salaried, self-employed, or a freelancer, as long as the monthly rent exceeds ₹50,000 and the tenant is not covered by tax audit.

4. Do I need a TAN for this?

No. Tenants under Section 194-IB are specifically exempted from obtaining a TAN. Your PAN is sufficient to file Form 26QC and download Form 16C.

5. What if my landlord already pays taxes and doesn’t want TDS to be deducted?

Regardless of the landlord’s personal tax status, if the threshold conditions are met, deducting TDS is your legal obligation as a tenant. Your landlord can claim the deducted TDS as credit while filing their ITR.

6. Does TDS under Section 194-IB include GST?

No. If GST is separately mentioned in the rent agreement and invoice, TDS is deducted only on the base rent amount, excluding the GST portion.

7. I missed deducting TDS for this year. What should I do?

File Form 26QC as soon as possible and pay the TDS along with applicable interest (1% per month for late deduction and 1.5% per month for late deposit). Also pay the late filing fee under Section 234E (₹200 per day). The sooner you file, the lower the accumulated penalties.

8. My landlord has two co-owners. How do I handle this?

File a separate Form 26QC for each co-owner based on their ownership share (or as per the rental agreement). Issue a separate Form 16C to each co-owner.

Key Takeaways

- Form 16C is the TDS certificate a tenant must issue to a landlord when monthly rent exceeds ₹50,000 and the tenant is an individual or HUF not liable to tax audit.

- The current TDS rate under Section 194-IB is 2% (reduced from 5% by the Finance Act (No. 2), 2024, effective 1 October 2024).

- Without the landlord’s PAN, TDS jumps to 20% — always collect the PAN upfront.

- TDS is deducted only once a year — on the last month’s rent at the end of the financial year (or last month of tenancy if vacating early).

- The compliance chain: deduct TDS → file Form 26QC within 30 days → download Form 16C from TRACES → issue to landlord within 15 days of the Form 26QC due date.

- No TAN required — PAN is sufficient.

- For multiple co-owners, file a separate Form 26QC and issue a separate Form 16C for each co-owner.

- From Tax Year 2026-27 (rent from April 2026 onwards), Form 16C is replaced by the unified Form No. 132 under the Income Tax Act, 2025.

Sources: Income Tax Department, Government of India — Form 16 and Form 16A; Income Tax Department — Form No. 132 (Earlier Form No. 16B/16C/16D/16E) FAQ; Taxguru.in — Section 194-IB: TDS Rate Reduced on Rent to 2% wef 01st October 2024; EY India — Recent updates regarding compliance on payment of rent under Section 194-IB.

This article is for general information and does not constitute tax or legal advice. For your specific situation, consult a chartered accountant or tax professional.