Quick summary: If you earn interest from a fixed deposit (FD), recurring deposit (RD), or similar savings, your bank is required to deduct TDS (Tax Deducted at Source) automatically once your interest crosses a certain limit. But if your total income is too low to be taxed, you shouldn’t have to pay that TDS in the first place. Form 15G and Form 15H are the official self-declaration forms that let you tell your bank: “Don’t deduct TDS from my interest, my income is below the taxable limit.” Form 15G is for people below 60 years of age. Form 15H is for senior citizens aged 60 and above. Both forms must be submitted fresh at the start of every financial year.

Why Does TDS Get Deducted on Your Interest Income at All?

Banks and financial institutions are legally required to deduct TDS on interest income once it crosses a set threshold limit, even if your total income for the year is below the taxable level. This is governed by Section 194A of the Income Tax Act, 1961.

As per the revised thresholds that took effect from 1 April 2025 (i.e., from FY 2025-26 onwards, as amended by the Finance Act, 2025):

| Who Earns the Interest | Where the FD/Deposit Is Held | TDS Kicks In When Annual Interest Exceeds |

| General taxpayers (below 60 years) | Bank, co-operative bank, or post office | ₹50,000 |

| Senior citizens (60 years or above) | Bank, co-operative bank, or post office | ₹1,00,000 |

| Anyone | Other non-banking entities | ₹10,000 |

When interest exceeds these limits, the bank deducts TDS at 10% (or 20% if your PAN is not on record with the bank). This happens whether or not you actually owe any tax.

The problem: many people, retirees, homemakers, students, or anyone with a modest income, have FD interest income but their total income is below the taxable limit. They shouldn’t be paying TDS at all. And that’s exactly what Form 15G and Form 15H exist to solve.

What Are Form 15G and Form 15H?

Both forms are self-declaration forms submitted to your bank (or other deductor) under Section 197A of the Income Tax Act, 1961, read with Rule 29C of the Income Tax Rules, 1962. By submitting them, you declare that your income is below the taxable limit and your tax liability is nil, so the bank should not deduct TDS on your interest income.

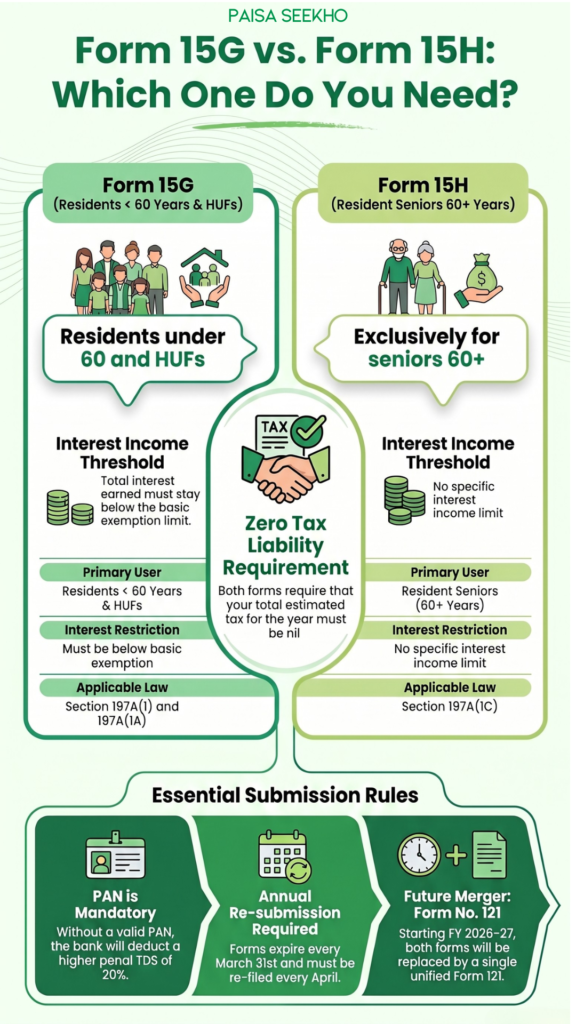

- Form 15G is for resident individual taxpayers below 60 years of age, and for Hindu Undivided Families (HUFs).

- Form 15H is exclusively for resident senior citizens aged 60 years or above.

You submit the form directly to the institution that pays you interest, your bank, post office, or even the EPFO. You do not submit it to the Income Tax Department.

Who Can Submit Form 15G? (Eligibility Conditions)

To be eligible to submit Form 15G, all three of the following conditions must be satisfied:

- You are a resident Indian. Non-Resident Indians (NRIs) cannot submit this form.

- You are below 60 years of age (individuals), or you are a HUF. Companies and firms are not eligible.

- Your estimated total income for the financial year, including the interest income in question, results in zero tax liability, meaning your total income is below the basic exemption limit.

There is an additional condition specific to Form 15G (not Form 15H):

- The aggregate amount of interest income on which you’re claiming non-deduction of TDS should also not exceed the basic exemption limit applicable to you.

In plain terms: for Form 15G, both your total income and the interest income itself must stay within the zero-tax zone. Failing to meet any of these conditions means you are not eligible to submit the form.

Example: Meena, 35, earns ₹2,00,000 from freelancing and ₹40,000 as FD interest in FY 2025-26. Her total income is ₹2,40,000. Under the old tax regime, the basic exemption limit is ₹2,50,000. Both her total income and her interest amount are below this limit, and her tax liability is nil, she can submit Form 15G to her bank.

Who Can Submit Form 15H? (Eligibility Conditions)

Form 15H has a more relaxed set of conditions than Form 15G. To be eligible:

- You are a resident Indian.

- You are 60 years of age or above during the financial year.

- Your total estimated income for the year results in zero tax liability, i.e., your tax payable is nil.

Notice the key difference from Form 15G: Form 15H does not require that the interest income itself be below the basic exemption limit. A senior citizen’s tax bill can be nil even if their FD interest is relatively high, because senior citizens benefit from a higher basic exemption limit (₹3,00,000 for those aged 60–79, and ₹5,00,000 for those aged 80 and above under the old tax regime), and they can also claim deductions under Section 80C, Section 80D, and Section 80TTB (which allows a deduction of up to ₹50,000 on interest income for senior citizens).

Example: Mr. Sharma, 65, earns ₹2,80,000 in FD interest and ₹50,000 from other sources in FY 2025-26, a total of ₹3,30,000. His interest exceeds the ₹1,00,000 TDS threshold so the bank would normally deduct TDS. But after claiming ₹1,50,000 under Section 80C and using the senior citizen basic exemption limit of ₹3,00,000, his taxable income is nil. He is eligible to submit Form 15H and stop the TDS deduction.

Form 15G vs Form 15H: Key Differences at a Glance

| Form 15G | Form 15H | |

| Who should file | Resident individuals below 60 years; HUFs | Resident senior citizens aged 60 years or above |

| Can senior citizens use it? | No | Yes, exclusively |

| Tax liability condition | Must be nil | Must be nil |

| Interest income condition | Interest amount must also not exceed basic exemption limit | No such additional restriction |

| Applicable law | Section 197A(1) and 197A(1A), Income Tax Act | Section 197A(1C), Income Tax Act |

| HUF eligible? | Yes, via Form 15G | No |

| NRIs eligible? | No | No |

| Validity | One financial year only | One financial year only |

Where Can You Submit Form 15G and Form 15H?

These forms can be submitted to any entity that pays you income subject to TDS and is listed under Section 197A. The most common places are:

- Banks, for interest on fixed deposits, recurring deposits

- Post offices, for interest on post office deposits and schemes

- EPFO (Employees’ Provident Fund Organisation), for PF withdrawals (Form 15G only, since PF withdrawal eligibility applies to non-senior citizens typically)

- Insurance companies, for certain insurance payouts

- Mutual fund companies, for income from units

You must submit a separate form to each institution where you earn interest income. One form submitted to one bank does not cover another bank or the post office. If you have FDs in two different banks, you need to submit to both.

When to Submit?

There is no strict due date under the law for submitting these forms, but best practice is to submit at the very beginning of each financial year, ideally in April. This ensures that TDS is not deducted from the first interest credit of the year.

If you submit mid-year, TDS that has already been deducted for earlier quarters cannot be refunded by the bank, the bank has already deposited it with the government. You’d need to file an Income Tax Return to claim that TDS back as a refund. Submitting early avoids this inconvenience entirely.

Both Forms Are Valid for One Year Only

This is the most common mistake people make: Form 15G and Form 15H are valid only for the financial year in which they are submitted. They expire on 31 March every year.

You must re-submit them at the start of every new financial year if your eligibility conditions continue to be met. There is no automatic renewal.

What If You Submit a False Declaration?

These are legal declarations and not casual requests. Making a false statement in Form 15G or Form 15H is treated seriously by the Income Tax Department. Under Section 277 of the Income Tax Act, a false declaration can attract prosecution, including:

- If the tax sought to be evaded exceeds ₹25 lakh: imprisonment of not less than 6 months, which may extend to 7 years, plus a fine.

- In other cases: imprisonment of 3 months to 2 years, plus a fine.

Only submit these forms if you are genuinely eligible, i.e., your estimated total income and resulting tax liability are truly nil for the year.

PAN Is Mandatory

Your PAN must be mentioned correctly in both forms. If you don’t provide PAN:

- The form is invalid and will not be accepted.

- The bank is required to deduct TDS at a higher rate of 20% instead of 10%.

- As per CBDT Circular No. 03/2011, in the absence of PAN, Form 15G/15H and any other exemption certificates are treated as invalid, and the higher (penal) TDS rate applies.

Before submitting, make sure your PAN and date of birth are correctly updated in your bank’s records. Some banks may also ask for a self-attested PAN copy along with the form.

How to Submit: Online and Offline Options

Offline (at the bank branch):

Fill in Part I of the form (the declaration part), sign it, and submit it to your bank branch along with a self-attested copy of your PAN card. Keep a copy and ask for an acknowledgement.

Online (via net banking or mobile app):

Most major banks now allow you to submit Form 15G and Form 15H online through their net banking portals or mobile apps under the “Tax” or “TDS” section. This is convenient, faster, and generates a digital acknowledgement.

For EPF withdrawals:

Log in to the EPFO Member Portal, initiate an online withdrawal claim, and upload Form 15G during the claim process (if eligible).

When you submit Form 15G/15H across multiple banks, Part I asks you to declare how many similar forms you’ve submitted to other institutions and the aggregate income they cover. Fill this in honestly, it helps the tax department cross-verify your total interest income.

What If TDS Has Already Been Deducted?

If you forgot to submit the form at the start of the year and TDS has already been deducted, the bank cannot refund it, it has already been deposited with the government on your behalf. However, that money is not lost. When you file your Income Tax Return (ITR), the TDS will appear in your Form 26AS and Annual Information Statement (AIS). If your actual tax liability is nil, the TDS will be reflected as excess tax paid, and you will receive a refund from the Income Tax Department after your ITR is processed.

Moral of the story: submit on time and avoid the refund wait. But if you’ve missed it, filing your ITR is the way to get your money back.

Important: Form 15G and 15H Are Being Replaced by Form 121

This is a change that directly affects anyone who has to submit these forms from FY 2026-27 onwards.

Under the Income Tax Act, 2025 (which takes effect from 1 April 2026), and the accompanying Income Tax Rules, 2026, Form 15G and Form 15H are being merged into a single unified form called Form No. 121. According to the Income Tax Department’s official FAQ on Form No. 121:

- Form No. 121 is the new statutory declaration form under Section 393(6) of the Income Tax Act, 2025, which corresponds to the old Section 197A.

- It merges Form 15G (for those below 60 and HUFs) and Form 15H (for senior citizens) into one form, removing confusion about which to use.

- The eligibility conditions remain substantially the same, nil tax liability is the core requirement, with the additional interest-income condition retained for non-senior citizens.

- The key improvement is a unified, better-structured format aligned with the new “Tax Year” terminology used in the Income Tax Act, 2025.

For FY 2025-26 (i.e., the current year, for returns due in 2026): you should continue using Form 15G or Form 15H, as applicable, at your bank. Form 121 applies from Tax Year 2026-27 onwards, for income earned from April 2026 onwards.

Frequently Asked Questions (FAQs)

1. Can a senior citizen submit Form 15G?

No. Senior citizens (aged 60 and above) must submit Form 15H. Form 15G is only for individuals below 60 and HUFs.

2. Do I need to submit these forms to every bank I have an FD in?

Yes. You must submit a separate form to each institution where you earn interest income. One submission does not cover multiple banks or the post office.

3. Are these forms valid for multiple years?

No. Form 15G and Form 15H are valid only for the financial year in which they are submitted. You must renew them at the start of every financial year.

4. Can I submit Form 15G or 15H if I am an NRI?

No. These forms are only for resident Indians. NRIs are not eligible.

5. What if my income goes above the taxable limit during the year after I’ve already submitted the form?

If your actual income ends up crossing the taxable limit during the year, you must inform your bank and stop claiming the TDS exemption. Continuing to claim it when you’re no longer eligible can lead to penalties.

6. Does submitting Form 15G or 15H mean I don’t need to file an ITR?

No. These forms are only for preventing TDS deduction at the source. If your income exceeds the basic exemption limit or if you are otherwise required to file an ITR (for example, if you have multiple income sources), you still need to file your return. The forms are not a substitute for ITR filing.

7. What if I have deposits in multiple branches of the same bank?

Threshold limits under Section 194A are calculated on the aggregate interest from all branches of the same bank. So if your total interest across all branches of one bank exceeds ₹50,000 (or ₹1,00,000 for senior citizens), TDS applies even if individual branches pay less. You submit the form to the bank (not each branch separately), and it covers all branches under that bank.

8. What happens to Form 15G and 15H from FY 2026-27?

They are replaced by Form No. 121 under the Income Tax Act, 2025. The eligibility conditions remain similar, but both older forms are merged into one.

Key Takeaways

- Form 15G (below 60, and HUFs) and Form 15H (senior citizens aged 60+) let eligible taxpayers stop their bank or institution from deducting TDS on interest income.

- For FY 2025-26, banks must deduct TDS once interest exceeds ₹50,000 (non-senior citizens) or ₹1,00,000 (senior citizens), thresholds raised from the previous year by the Finance Act, 2025.

- Form 15G has two conditions: nil total tax liability, and interest income must not exceed the basic exemption limit. Form 15H only requires nil tax liability, the relaxed condition makes it easier for many senior citizens to qualify.

- Both forms are valid for one financial year only and must be submitted fresh each year, ideally at the start of April.

- PAN is mandatory. Without it, the form is invalid and the bank will deduct TDS at 20%.

- Making a false declaration can lead to prosecution under Section 277 of the Income Tax Act.

- From Tax Year 2026-27 (income earned from April 2026), both forms will be replaced by the unified Form No. 121 under the new Income Tax Act, 2025.

Sources: Income Tax Department, Government of India – Form No. 121 (Earlier Form Nos. 15G & 15H) FAQ; Taxguru.in – Budget 2025: Section 194A TDS Thresholds Revised Effective April 2025; ICICI Bank – Form 15G/15H FAQs.

This article is for general information and does not constitute tax advice. For your specific situation, consult a chartered accountant or tax professional.