Quick summary: Form 10-IE and Form 10-IEA both deal with choosing between India’s old and new income tax regimes, but they served opposite purposes at different points in time. Form 10-IE is no longer used at all. Today, only Form 10-IEA matters, and only if you have business or professional income and want to opt out of the new tax regime (which is now the default). If you’re a salaried employee with no business income, you don’t need either form, you simply tick a box inside your ITR.

This article breaks down exactly how these two forms differ, who needs to file Form 10-IEA today, and how to do it correctly.

A Quick Recap: Old Regime vs New Regime

Before getting into the forms, it helps to understand why they exist at all.

India currently has two ways to calculate your income tax:

- Old tax regime: Higher tax rates, but you can claim deductions and exemptions, like Section 80C (investments), Section 80D (health insurance), HRA (House Rent Allowance), and home loan interest.

- New tax regime: Lower tax rates, but you lose access to most of those deductions and exemptions (with a few exceptions, like the standard deduction and NPS contributions under Section 80CCD(2)).

Since the new regime was introduced, the government has changed which one applies by default, and that change is exactly what created the need for these two forms.

What Was Form 10-IE?

Form 10-IE was introduced when the new tax regime first launched (under Section 115BAC) for FY 2020-21 (AY 2021-22). Back then, the old regime was the default. If you wanted to use the new regime instead, and you had income from business or profession, you had to actively tell the tax department by filing Form 10-IE before filing your ITR.

If you were a salaried individual without business income (filing ITR-1 or ITR-2), you didn’t need Form 10-IE at all, you could simply pick the new regime directly inside your ITR.

Form 10-IE is no longer in use. The Union Budget 2023 changed the rules from FY 2023-24 (AY 2024-25) onwards, making the new regime the default for everyone. Since you no longer need to “opt in” to something that’s already the default, Form 10-IE was discontinued.

What Is Form 10-IEA?

Form 10-IEA was introduced to handle the opposite situation. Since the new tax regime became the default from AY 2024-25 onwards, taxpayers who prefer the old regime now have to actively opt out, and that’s done by filing Form 10-IEA.

According to the Income Tax Department, Form 10-IEA was notified vide Notification No. 43/2023 dated 21st June 2023, and is applicable from Assessment Year 2024-25 onwards.

Form 10-IEA is used for two purposes:

- Opting out of the new tax regime (i.e., choosing the old regime), or

- Re-entering the new tax regime after having opted out earlier

Form 10-IE vs Form 10-IEA: Key Differences

| Form 10-IE | Form 10-IEA | |

| Purpose | To opt into the new tax regime | To opt out of the new tax regime (or re-enter it) |

| Status | Discontinued from AY 2024-25 onwards | Currently active and applicable |

| Default regime at the time | Old regime was default | New regime is default |

| Applicable years | AY 2021-22 to AY 2023-24 | AY 2024-25 onwards |

| Who had to file it | Individuals/HUFs with business or professional income who wanted the new regime | Individuals/HUFs/AOPs/BOI/AJP with business or professional income who want the old regime |

| Who was exempt | Salaried taxpayers without business income (could choose directly in ITR) | Salaried taxpayers without business income (can still choose directly in ITR) |

| Number of times it can be used | Could be filed each year by eligible taxpayers | Can be used to opt out only once in a lifetime if you have business/professional income |

In short: Form 10-IE belongs to the past. Form 10-IEA is what you need to know about today.

Who Needs to File Form 10-IEA?

This is where most of the confusion happens, so let’s be precise. According to the Income Tax Department’s own FAQs:

You must file Form 10-IEA if both of these apply to you:

- You have income under the head “Profits and Gains of Business or Profession,” and

- You want to opt for (or continue with) the old tax regime, instead of the new default regime

This typically means you’re filing ITR-3 (for business/professional income) or ITR-4 (for presumptive taxation). For Association of Persons, Body of Individuals, or Artificial Juridical Persons filing ITR-5, Form 10-IEA applies in a similar way.

Who Does NOT Need to File Form 10-IEA?

If you’re a salaried employee, pensioner, or someone earning only from salary, house property, capital gains, or other sources, with no business or professional income, you do not need to file Form 10-IEA at all, regardless of which regime you prefer.

You simply select your preferred regime directly while filling out ITR-1 or ITR-2, by answering the question on whether you wish to opt out of the new tax regime. You can make this choice fresh every single year, there’s no lifetime restriction for non-business taxpayers.

The “Once in a Lifetime” Rule, Read This Carefully

This is the single most important rule to understand if you have business or professional income, because getting it wrong can permanently affect your tax planning:

- If you have business/professional income and you opt out of the new regime (i.e., choose the old regime) by filing Form 10-IEA, you can only switch back to the new regime once in the future, by filing Form 10-IEA again with the “re-entering” option.

- Once you exit the old regime after having entered it, you can never opt for the old regime again, unless you stop having business or professional income altogether.

- This restriction does not apply to taxpayers without business/professional income, they can switch between regimes every year, with no limits.

In other words, if you run a business or are a professional (like a freelancer, doctor, or consultant), think carefully before switching back and forth, you effectively get one “free pass” to return to the new regime, and after that, the old regime door closes permanently (as long as you continue to have business income).

How to File Form 10-IEA Online: Step-by-Step

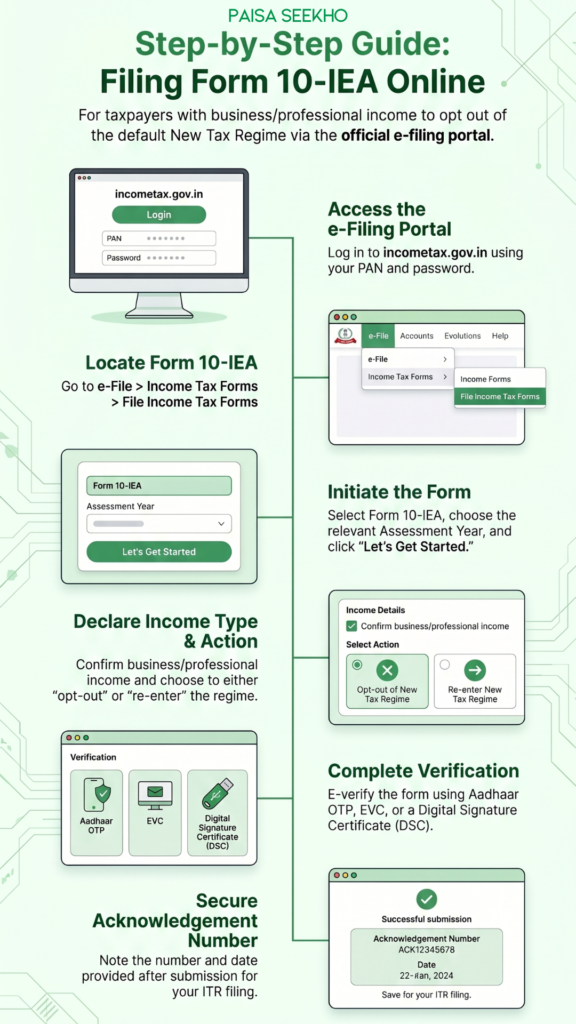

Form 10-IEA can only be submitted online through the Income Tax Department’s e-filing portal, there’s no offline option.

- Log in to the e-filing portal (incometax.gov.in) using your PAN and password.

- Go to e-File → Income Tax Forms → File Income Tax Forms.

- Under “Persons with Business/Professional Income,” select Form 10-IEA, or search for it directly.

- Select the relevant Assessment Year and click Continue.

- Review the list of documents/details required, then click “Let’s Get Started.”

- Answer “Yes” when asked if you have income under the head “Profits and Gains from Business or Profession” during the assessment year.

- Choose whether you’re opting out of the new regime or re-entering it (if you’d previously opted out).

- Select the applicable due date for filing your return of income under Section 139(1).

- Fill in the remaining details and confirm the Verification tab.

- E-verify the form using Aadhaar OTP, EVC (Electronic Verification Code), or a Digital Signature Certificate (DSC).

- Once submitted and verified, you’ll receive an acknowledgement number, note this down carefully, since you’ll need to mention it (along with the filing date) in your ITR.

What Happens If You File Late or Skip It

This is where Form 10-IEA gets strict. According to the Income Tax Department:

- Form 10-IEA must be filed on or before the due date for filing your return under Section 139(1). Filing it after this date means the form is treated as invalid.

- If your Form 10-IEA is invalid (filed late, or with an incorrect due date selected), you will not get the benefit of the old tax regime for that assessment year, your return will be processed under the new (default) regime instead.

- Form 10-IEA cannot be revised or withdrawn within the same year once filed. If you’ve made an error, your only option is to file it correctly in a subsequent assessment year.

- It is strongly advised to file Form 10-IEA before filing your ITR, not after, since you need the acknowledgement number and filing date to mention in your return.

Common Mistakes to Avoid

- Confusing Form 10-IE with Form 10-IEA. Form 10-IE is obsolete, don’t use outdated guides that reference it for current filings.

- Filing it every year unnecessarily. If you’ve already opted out of the new regime in an earlier year and want to continue with the old regime, you don’t need to file Form 10-IEA again every year, only when you want to change your choice.

- Switching regimes casually without understanding the lifetime restriction. If you have business income, treat the decision to move from the old regime back to the new regime as a one-time, careful decision.

- Missing the due date. Unlike some other compliance steps, there’s no flexibility here, a late Form 10-IEA simply doesn’t count, and you’ll be taxed under the new regime by default.

- Not e-verifying the form. An unverified form isn’t treated as filed.

Frequently Asked Questions

1. Is Form 10-IE still relevant for any taxpayer today?

No. Form 10-IE was used only up to AY 2023-24, when the old regime was still the default. It has been completely discontinued and replaced by Form 10-IEA.

2. Do salaried employees need to file Form 10-IEA?

No, not if you have no business or professional income. You can choose your tax regime directly in ITR-1 or ITR-2 each year, without filing any separate form.

3. Can I file Form 10-IEA after submitting my ITR?

It’s strongly discouraged. You need the Form 10-IEA acknowledgement number to correctly fill in your ITR, so it should be filed before, not after.

4. How many times can I switch between regimes if I have business income?

You can opt out of the new regime once, and then switch back to the new regime once more. After that one switch back, you cannot opt for the old regime again unless you no longer have business or professional income.

5. What happens if I file Form 10-IEA after the ITR due date?

The form is treated as invalid, and you will not get the benefit of the old tax regime for that assessment year, your tax will be computed under the new regime by default.

6. Do I need to file Form 10-IEA every year to stay in the old regime?

No. Once you’ve opted out of the new regime, you continue under the old regime in subsequent years without needing to file the form again, unless you want to switch back.

Key Takeaways

- Form 10-IE is history, it was used to opt into the new regime when the old regime was default, and stopped being relevant from AY 2024-25 onwards.

- Form 10-IEA is current, it’s used to opt out of (or re-enter) the new regime, which is now the default for all taxpayers.

- Only taxpayers with business or professional income (filing ITR-3, ITR-4, or ITR-5) need to file Form 10-IEA. Salaried taxpayers choose their regime directly in their ITR.

- If you have business income, switching out of the new regime and back again is allowed only once in a lifetime, after that, you’re locked into the new regime as long as you have business income.

- File Form 10-IEA before your ITR and before the due date, a late filing is treated as invalid, with no exceptions.

Sources: Income Tax Department, Government of India – FAQs on New Tax vs Old Tax Regime; Income Tax Department – Form 10-IEA FAQ; Income Tax Department – Form 10-IEA User Manual.

This article is for general information and does not constitute tax advice. For your specific situation, consult a chartered accountant or tax professional.