TL;DR: Key Takeaways on Building Credit Score Without Credit Card

If you want to start building your financial footprint today, here is the quick summary of your best options:

- The Authorized User Hack: You can piggyback on a family member’s good credit score by becoming an “authorized user” on their existing credit card account.

- Consumer Durable Loans: Buying a smartphone or a laptop on a “No-Cost EMI” from a retail store is the easiest way to generate your first active loan account.

- Secured Loans: Taking a small loan against your Fixed Deposit (FD) or a Gold Loan allows you to build credit with almost zero risk of rejection.

- Buy Now, Pay Later (BNPL): Modern BNPL apps report to credit bureaus. Using them for small, daily purchases and paying them off instantly builds a healthy repayment history.

- Patience is Key: A credit score is not built overnight. It typically takes 6 to 12 months of consistent, on-time payments for a credit bureau to generate a reliable score.

Introduction

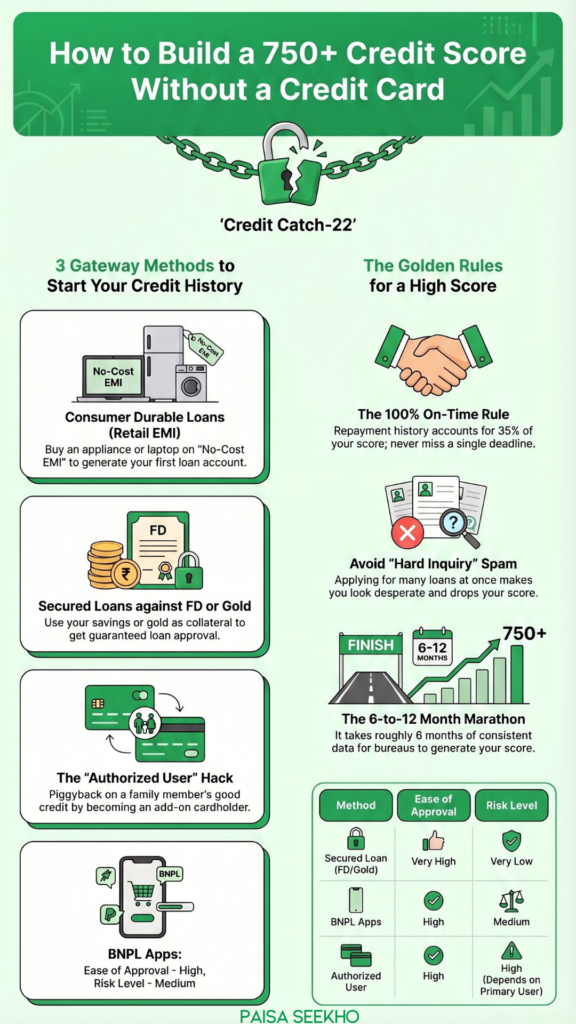

It is the classic financial Catch-22: You walk into a bank to apply for a personal loan or a home loan, and the manager rejects you because you do not have a credit history. They advise you to get a credit card first to build your score. But when you try to apply for a credit card, they reject you again—because you do not have a credit score!

If you are a student, a recent graduate, or someone who simply hates the idea of plastic debt, breaking into the formal financial system can feel incredibly frustrating. You are labeled as a “New-to-Credit” (NTC) borrower, essentially an invisible ghost to the credit bureaus like CIBIL, Experian, and Equifax.

But here is a financial secret the banks rarely advertise: You do not actually need a credit card to prove you are a trustworthy borrower.

According to recent financial guidelines and market trends in 2026, building a stellar 750+ credit score is entirely achievable through alternative lending methods, strict financial discipline, and a timely loan repayment plan. In this comprehensive guide, we are going to break down exactly how you can establish a rock-solid credit profile from absolute scratch, without ever swiping a credit card.

Why is it Hard to Build a CIBIL Score From Scratch in India?

To understand the solution, you must first understand the problem. A credit score (which ranges from 300 to 900) is a mathematical grade that reflects your past behavior with borrowed money. Lenders use it to judge the “5 C’s of Credit”: Character, Capacity, Capital, Collateral, and Conditions.

If you have never borrowed money, the bureaus have zero data on you. They cannot tell if you are a responsible saver or a reckless spender. For traditional banks, “no data” is treated almost the same as “bad data.” Because they cannot assess your risk, they simply refuse to lend to you.

To break this cycle, you need to find lenders who are willing to take a small risk on you, allowing you to generate that crucial first line of data.

How Can Consumer Durable Loans and BNPL Help Build Your Credit Score Without a Credit Card?

The easiest way to enter the credit system is through the things you already plan to buy.

1. Consumer Durable Loans (The Retail EMI)

Imagine you need a new laptop for work or a refrigerator for your home. Instead of paying ₹40,000 in cash upfront, you walk into an electronics store and opt for a “Consumer Durable Loan” (often marketed as No-Cost EMI by NBFCs like Bajaj Finserv or Home Credit).

- These lenders specialize in New-to-Credit (NTC) customers. They require very basic income proof and minimal documentation.

- The moment you sign the EMI contract, an active loan account is opened in your name.

- By paying your ₹4,000 EMI perfectly on time every month for 10 months, you generate a flawless repayment history. The NBFC reports this to CIBIL, and your credit score is officially born!

2. Buy Now, Pay Later (BNPL) Apps

If you do not need a big-ticket appliance, you can use modern fintech. Apps like Amazon Pay Later, Flipkart Pay Later, or Simpl act as digital micro-loans. When you order groceries or a shirt, you choose to pay later.

Behind the scenes, these apps partner with banks to issue you a micro-credit line. If you use BNPL responsibly and clear your dues before the 5th of every month, this active, positive data is consistently fed to the credit bureaus, boosting your score rapidly.

What is the “Authorized User” Hack to Build a Credit Score Without a Credit Card?

What if you do not want to take a loan or use a BNPL app? You can use a brilliant strategy known as “Piggybacking.”

If your parent or spouse has an excellent credit score and a credit card with a flawless repayment history, you can ask them to add you as an Authorized User (often called an Add-on Cardholder).

Here is why this works:

- You get a physical card with your name on it, but the primary account holder is legally responsible for the bill.

- Most major Indian banks report the payment history of that specific card to the credit bureaus under both the primary user’s PAN and the authorized user’s PAN.

- Even if you lock the add-on card in a drawer and never spend a single rupee on it, the primary user’s good financial habits (paying their bills on time) will automatically reflect on your fresh credit report, building your score by proxy!

(Warning: This is a double-edged sword. If the primary user defaults or misses a payment, it will instantly damage your new credit score as well. Only piggyback on someone who is highly financially disciplined).

How Do Secured Loans (Gold or FD) Function as a Credit Building Tool?

If you have some savings but no credit history, you hold the ultimate key to unlocking a high CIBIL score. Lenders are terrified of losing money, but if you provide “Collateral,” their fear drops to zero.

1. Loan Against Fixed Deposit (FD)

Instead of breaking your ₹1 Lakh FD to pay for an emergency, you can walk into your bank and ask for an “Overdraft or Loan against FD.”

The bank will easily give you a loan of ₹90,000 without even checking your CIBIL score because your actual FD money secures the loan. You then slowly repay this ₹90,000 loan over a year. Because it is a formal loan, the bank reports your timely EMI payments to CIBIL, building your score rapidly at a very low interest rate.

2. Gold Loans

Similar to FD loans, Gold Loans are heavily collateralized. Lenders like Muthoot or Manappuram rarely reject an applicant because they hold the physical gold. Taking a small gold loan for six months and strictly adhering to the timely loan repayment plan is a fantastic, surefire way to establish your creditworthiness in the formal banking system.

What Financial Discipline Rules Must You Follow to Maintain Your New CIBIL Score?

Getting your first loan or BNPL account is only step one. The real challenge is keeping that score high. A credit score is incredibly fragile; it takes a year to build but only one bad month to destroy.

If you want to cross the 750+ mark, you must adopt absolute financial discipline:

- The 100% On-Time Rule: Your repayment history accounts for roughly 35% of your total credit score. Paying an EMI even two days late can trigger a “Days Past Due” (DPD) flag on your report. Automate your EMI payments (via e-NACH) so they deduct automatically from your bank account.

- Do Not “Hard Inquiry” Spam: Every time you apply for a new loan, the lender pulls your credit report. This is called a “Hard Inquiry,” and it drops your score by a few points. If you apply for five different loans in a single week hoping one gets approved, you will look desperate to the bureaus, and your score will crash.

- Mix Your Credit: Eventually, the bureaus want to see that you can handle different types of debt. Once you have successfully managed a consumer durable loan, successfully managing a different type of loan (like a small auto loan) later on will improve your “Credit Mix,” pushing your score even higher.

Conclusion: Patience and Persistence

Building a credit score without a credit card is not a myth; it is simply a matter of strategic financial planning. The days of needing an elite, plastic credit card to prove your worth to a bank are over.

Whether you choose to buy a washing machine on a No-Cost EMI, utilize a BNPL app for your monthly groceries, or leverage a small loan against your Fixed Deposit, the core principle remains the same: Borrow responsibly, and repay ruthlessly on time.

Remember, the journey from an “NTC” (New-to-Credit) ghost to a prime borrower with an 800+ CIBIL score is a marathon, not a sprint. It requires at least six to eight months of flawless payment history. Be patient, stick to your timely repayment plans, and soon, the same banks that rejected you will be lining up to offer you their best home loan interest rates.

Frequently Asked Questions (FAQs): Credit Score Without a Credit Card

Q1: Can I really get a 750+ credit score without ever owning a credit card?

Yes, absolutely. Credit bureaus calculate your score based on your repayment history across all types of credit, not just credit cards. Managing a personal loan, auto loan, or consumer durable EMI perfectly can easily push your score past 750.

Q2: Does paying my rent or electricity bill on time increase my CIBIL score?

In India, standard utility bills (like electricity or water) and regular rent payments are generally not reported to credit bureaus like CIBIL. Therefore, paying them on time will not build your credit score, though missing them could lead to legal trouble.

Q3: How long does it take to generate a CIBIL score for a first-time borrower?

Once you take your very first loan (like a consumer durable EMI), it typically takes the credit bureaus about 6 months of consistent data collection to generate your initial three-digit credit score.

Q4: Can I use an Education Loan to build my credit score?

Yes! If you took an education loan, the repayment period (which usually starts after you graduate and secure a job) acts as a powerful credit-building tool. Paying those massive EMIs on time proves extreme financial responsibility to the bureaus.

Q5: Does BNPL (Buy Now, Pay Later) actually report to credit bureaus in India?

Yes. Regulated BNPL platforms (like Amazon Pay Later or Simpl) partner with registered NBFCs and banks. Every time you use their service, it is treated as a micro-loan, and your repayment behavior is strictly reported to CIBIL and Experian.

Q6: Will becoming an authorized user put my parent’s credit score at risk?

Yes. If you become an authorized user (add-on cardholder) on your parent’s card, and you recklessly spend money that cannot be repaid, your parent is legally liable for the debt. If the bill is missed, both your new credit score and your parent’s established score will crash.

Q7: What happens if I default on a small ₹15,000 consumer durable loan?

The size of the loan does not matter; the default does. If you default on a tiny smartphone EMI, it leaves a permanent “Write-off” or “Settled” remark on your credit report. This will severely damage your score and likely prevent you from getting a massive home loan years down the line.

Q8: How can I check my credit score for free in 2026?

As per RBI regulations, you are entitled to one completely free, detailed credit report every year directly from the official websites of the four major bureaus (CIBIL, Experian, Equifax, and CRIF High Mark). You can also use regulated financial platforms to check your basic score monthly for free.

Q9: Is it better to have no credit history or a bad credit history?

Having no credit history (being an NTC borrower) is slightly better than having a bad credit history. A blank slate means a bank simply cannot judge you yet. A bad credit history means the bank has mathematical proof that you are a high-risk defaulter, making future borrowing nearly impossible.

Q10: Are Peer-to-Peer (P2P) lending platforms good for building credit?

Yes. Taking a small micro-loan from regulated P2P lending platforms is another alternative for new-to-credit borrowers. These platforms report your repayment behavior to credit bureaus, allowing you to build your financial footprint through non-traditional lending channels.

Source: