TL;DR: Key Takeaways on the Gold Loan Boom

If you are in a rush and need the facts fast, here is the summary of why gold loans are winning:

- Massive Growth: The gold loan market is now bigger than the personal loan market, reaching ₹1.6 lakh crore by late 2025.

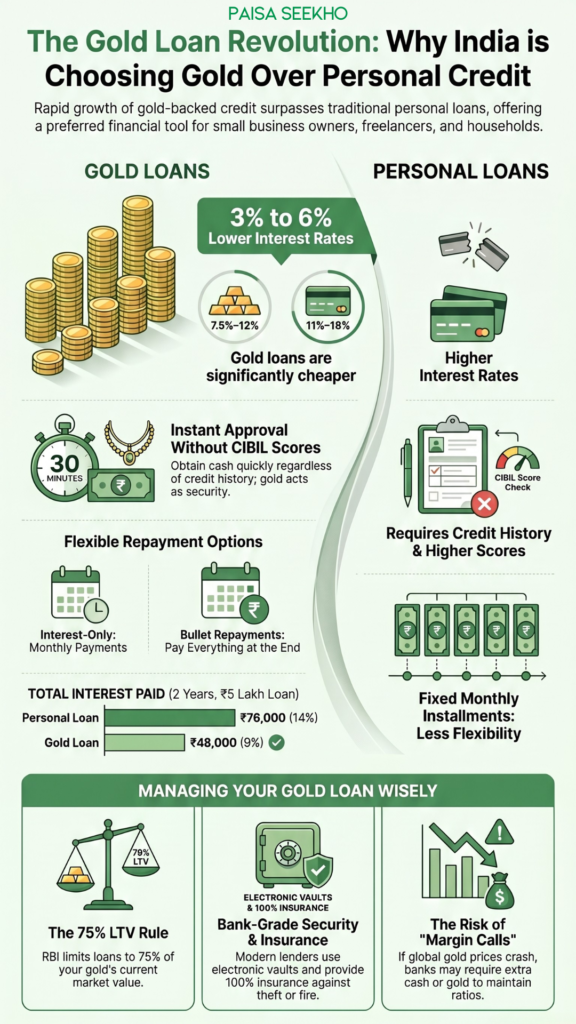

- Cheaper Interest: Because you are giving the bank “collateral” (security), gold loan interest rates are usually 2% to 5% lower than unsecured personal loans.

- Instant Cash: You can walk into a branch with a necklace and walk out with cash or a bank transfer in 30 minutes. Personal loans often take days.

- The CIBIL Factor: Even if you have a zero or low CIBIL score, you can get a gold loan because the bank has your gold as a guarantee.

- Flexible Repayment: Many gold loans allow you to pay only the interest every month and pay the entire principal at the very end.

- The Risk: If the price of gold crashes globally, the bank might ask you to deposit more gold or more cash to maintain the “Loan-to-Value” ratio.

Introduction

If you walk into any neighborhood market in India today, you will notice something interesting. Right next to the big bank branches, there are now dozens of bright, shiny offices belonging to companies like Muthoot Finance, Manappuram, or IIFL. Even the massive banks like SBI and HDFC have put up huge posters in their windows saying: “Get a loan against your gold in just 30 minutes!”

For a long time, taking a “Gold Loan” was seen as a last resort. People felt a bit of shame in “pawning” their family jewelry. It was something people did only in extreme emergencies.

But as we enter 2026, the data tells a completely different story. A massive cultural and financial shift has happened in India.

According to a shocking new report from December 2025, India’s gold loan market has exploded. The total amount of money people have borrowed against their gold has grown by a staggering 3.8 times since 2017. Even more surprisingly, for the first time in history, the total value of outstanding gold loans has surpassed the total value of traditional personal loans!

India is currently sitting on a ₹1.6 lakh crore gold loan mountain.

Why is this happening? Why are millions of middle-class Indians choosing to lock their jewelry in a bank vault instead of just taking a simple personal loan? In this comprehensive, easy-to-understand guide, we are going to dive deep into the world of gold-backed credit. We will explain the math, the benefits, the risks, and why 2026 is officially the “Year of the Gold Loan.”

1. What Exactly is a Gold Loan and How Does it Work?

A gold loan is a “Secured Loan.”

Think of it like this: If you ask a friend for ₹10,000, they might say no because they aren’t sure if you will pay them back. But if you give that friend your expensive smartphone to keep until you pay the money back, they will say yes instantly. The smartphone is the “security.”

In a gold loan, your Gold Jewelry (or gold coins) acts as that security.

- You take your gold to a bank or an NBFC (Non-Banking Financial Company).

- Their expert checks the purity of your gold (it usually needs to be 18 to 22 karats).

- The bank calculates the current market value of that gold.

- The bank gives you a loan, usually up to 75% of the gold’s value. This 75% limit is set by the RBI and is called the Loan-to-Value (LTV) Ratio.

If your gold is worth ₹1 Lakh, the bank will give you a loan of up to ₹75,000. You pay back the money with interest, and once the loan is fully paid, the bank returns your jewelry to you safely.

2. The 3.8x Growth: Why Did Gold Loans Surpass Personal Loans?

The December 2025 data shows that the gold loan portfolio in India hit ₹1.6 lakh crore. To put that in perspective, that is more than the entire annual budget of several Indian states!

There are three major reasons why this specific type of credit has become more popular than personal loans in 2026:

Reason A: The “Post-Pandemic” Small Business Boom

After the pandemic, millions of Indians started small home-businesses, cloud kitchens, and digital agencies. These entrepreneurs often need “Quick Capital” to buy inventory or pay for marketing.

Getting a traditional business loan requires three years of tax returns (ITR) and massive paperwork. A gold loan requires nothing but the gold in your hand. For a small business owner, the speed of a gold loan is worth more than anything else.

Reason B: The CIBIL Struggle

As we discussed in our previous guides, getting a personal loan requires a high CIBIL score (usually 750+). If you are a student, a freelancer, or someone who once missed a credit card payment, a personal loan will be rejected.

But a gold loan company doesn’t care about your past mistakes. They have your gold. This “Financial Inclusion” has allowed 16 crore new borrowers—especially women and rural residents—to enter the formal banking system for the first time.

Reason C: Drastic Improvements in Security

In the past, people were afraid that the “pawn shop” would steal their jewelry or replace their real diamonds with glass.

Today, the industry is dominated by massive, regulated companies. They use Electronic Vaults, provide 100% insurance on your jewelry, and have CCTV cameras everywhere. This professionalization has removed the “shame” and the “fear” associated with the product.

3. Gold Loan vs. Personal Loan: Which One is Cheaper?

This is the most important question for any Paisaseekho reader. Let’s look at the math.

When a bank gives you a Personal Loan, they are taking a risk. If you lose your job and stop paying, the bank has nothing to take from you. To cover this risk, they charge high interest rates, usually ranging from 11% to 18%.

When a bank gives you a Gold Loan, their risk is almost zero. If you don’t pay, they simply sell your gold in an auction and recover their money. Because their risk is lower, they pass that benefit to you.

- Gold Loan Interest Rates: Currently range from 7.5% to 12%.

The Math of Savings:

If you borrow ₹5 Lakhs for 2 years:

- On a Personal Loan at 14%, you pay roughly ₹76,000 in total interest.

- On a Gold Loan at 9%, you pay roughly ₹48,000 in total interest.

By choosing a gold loan, you are saving ₹28,000—which is enough to buy a brand new smartphone or pay for a family vacation!

5. The Repayment Advantage: Why Gold Loans Are More “Flexible”

If you take a personal loan, the bank forces you into a “Strict EMI” structure. You must pay back a part of the principal and a part of the interest every single month. If you miss one month, your CIBIL score is ruined.

Gold loans in 2026 offer three different ways to pay, making them perfect for people with irregular incomes (like farmers or freelancers):

Option 1: The Standard EMI

Just like a car loan, you pay a fixed amount every month until the loan is over.

Option 2: The “Interest-Only” Payout

This is a favorite for small business owners. You only pay the interest every month. This keeps your monthly out-go very low. You pay the entire original loan amount (the principal) in one big lump sum at the very end of the year when your business makes a profit.

Option 3: The Bullet Repayment

You don’t pay anything for the whole year—no interest, no principal. At the end of the loan term (say 12 months), you pay everything back in one go. While the interest adds up, this is perfect for someone who is waiting for a specific future payment (like a crop harvest or a year-end bonus).

6. Understanding the Risks: What is the “LTV Margin Call”?

While gold loans are amazing, they are not magic. There is one specific risk you must understand: Gold Price Volatility.

When you take a loan, the bank keeps a “Margin.” If your gold is worth ₹1 Lakh, they give you ₹75,000 (75% LTV). They keep that 25% gap as a safety net in case the price of gold falls.

The Margin Call:

Imagine the global economy stabilizes and the price of gold drops by 20%. Suddenly, your gold is only worth ₹80,000. Now, your ₹75,000 loan represents almost 94% of the gold’s value.

The RBI says banks cannot let the LTV go that high. The bank will send you a message called a “Margin Call.” They will ask you to:

- Pay back a part of the loan immediately to bring the ratio down.

- OR, deposit more gold jewelry to increase the security.

If you cannot do either, the bank has the legal right to sell your jewelry in an auction to recover their money. Therefore, always try to borrow a bit less than the maximum limit (aim for 60% LTV instead of 75%) to give yourself a safety cushion.

7. How to Get the Best Gold Loan Interest Rates in 2026

If you have decided that a gold loan is right for you, do not just walk into the first shop you see. Use these three expert tips to get the best deal:

1. Check the “Gram Rate”:

Every day, the price of gold changes. Different banks use different “valuation” methods. One bank might give you ₹3,500 per gram, while another might give you ₹3,800. Always ask: “How much cash will I get for exactly 10 grams of 22k gold?”

2. Watch the Processing Fees:

Some NBFCs offer a very low interest rate but charge a heavy 2% “Processing Fee” and another ₹500 for “Appraisal Fees.” A public sector bank like SBI or PNB might have a slightly higher interest rate but often charges a flat ₹200 to ₹500 fee, making it cheaper overall.

3. Ask About Insurance:

Ensure the bank provides you with a carbon-copy receipt that lists every single item you deposited, its weight, and its purity. More importantly, ask for a written guarantee that your gold is insured against fire and theft while it is in their vault.

Conclusion: Gold is Your Financial Freedom

The data from December 2025 is clear: India is falling in love with gold loans all over again.

By surpassing the personal loan market, gold-backed credit has officially become a mainstream financial tool for the modern Indian family. It has successfully moved from being a “sign of distress” to a “sign of smart financial planning.”

If you own gold, you are sitting on an invisible emergency fund. In a high-interest world where banks are becoming stricter with CIBIL scores and personal loan approvals, your gold is your “Fast Pass” to instant, affordable liquidity. Whether you are scaling a business, paying for a medical emergency, or simply consolidating higher-interest credit card debt, a gold loan is often the smartest move you can make in 2026.

Frequently Asked Questions (FAQs): Gold Loans in India

Q1: Is a gold loan better than a personal loan?

In most cases, yes. Gold loans are usually 3% to 5% cheaper than personal loans. They are also much faster to get (often approved in 30 minutes) and do not require a high CIBIL score.

Q2: What is the maximum “Loan-to-Value” (LTV) for a gold loan?

The Reserve Bank of India (RBI) currently allows banks and NBFCs to lend up to 75% of the market value of the gold you deposit.

Q3: Can I get a gold loan if I don’t have a job or a salary slip?

Yes. Since the loan is secured by your gold, most lenders do not ask for income proof, ITR, or salary slips. You only need a valid ID proof (Aadhaar/PAN) and the physical gold.

Q4: What happens if I can’t pay back my gold loan?

If you default on your payments and ignore the bank’s reminders, the lender has the legal right to auction your gold to recover the principal and the pending interest. Any extra money left over from the auction after settling the debt must be returned to you.

Q5: Will my gold be safe in the bank vault?

Yes. Regulated banks and NBFCs store your jewelry in high-security, fire-proof electronic vaults. The gold is also 100% insured. When you pay back the loan, you get back the exact same jewelry in the exact same condition.

Q6: Does a gold loan impact my CIBIL score?

Yes. Even though it is a secured loan, it is a formal credit product. If you pay your interest and principal on time, your CIBIL score will improve. If you default, your score will drop, making it harder to get a home loan or car loan in the future.

Q7: Can I use gold coins or gold biscuits to get a loan?

Most lenders accept gold jewelry and specially minted gold coins issued by banks. However, many private NBFCs do not accept raw gold biscuits or bars to prevent money laundering and purity issues.

Q8: What is the minimum and maximum tenure for a gold loan?

Gold loans are typically short-term. The minimum tenure can be as low as 7 days, and the maximum is usually 12 to 36 months.

Q9: Can I take back a part of my jewelry if I pay back a part of the loan?

Yes, this is called “Partial Release.” If you deposited four gold bangles and you pay back 25% of the loan, most banks will allow you to take back one bangle while keeping the rest as security for the remaining balance.

Q10: Why did gold loans grow 3.8x since 2017?

The growth was driven by a combination of digital banking improvements, a massive increase in gold prices (which allowed people to borrow more money for the same amount of gold), and a rising demand for quick, paperwork-free capital for small businesses.