TL;DR: Key Takeaways on the RBI 1-Hour Delay UPI Rule

If you are short on time and just want the quick facts, here is the summary of the RBI’s explosive new proposal:

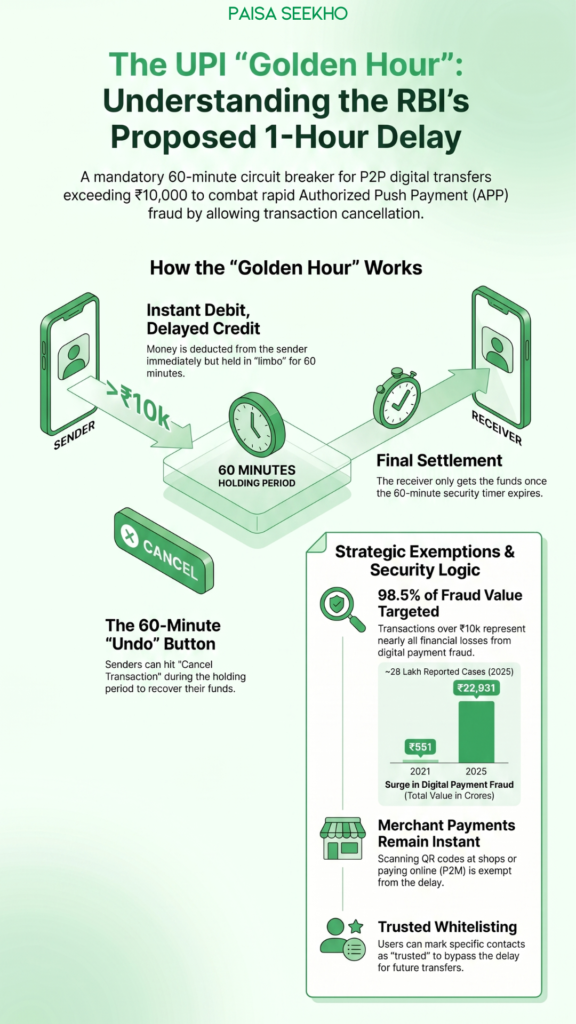

- The Core Rule: The RBI wants to introduce a mandatory one-hour delay for person-to-person (P2P) digital transfers (like UPI and IMPS) that are above ₹10,000.

- How it Works: The money will be deducted from your account instantly, but the receiver will only get it after 60 minutes.

- The “Undo” Button: During this 1-hour “Golden Hour,” the sender will have the option to hit cancel and get their money back.

- Why ₹10,000? Data shows that transactions above ₹10k account for only 45% of frauds by volume, but a staggering 98.5% of frauds by value.

- Merchant Exemption: Do not panic! Scanning a QR code at a grocery store, a petrol pump, or paying an online merchant will remain instant. This delay primarily targets transfers between two individual people.

- The Whitelist Hack: You will be able to “whitelist” trusted friends or family members so that future transfers to them remain completely instant.

Introduction

We have all been there. You are transferring money to a contractor, a landlord, or maybe someone selling a used laptop online. You type in the amount, enter your secret 4-digit UPI PIN, and hit send. Instantly, a green checkmark appears on your screen. The money is gone.

But what if, two minutes later, you realize you made a terrible mistake? What if that “customer care executive” on the phone was actually a scammer?

Right now, if you send money via UPI (Unified Payments Interface), there is no “undo” button. The money travels from your bank account to the receiver’s bank account in milliseconds. That incredible speed is exactly what made India’s digital payment system the envy of the entire world. However, that same speed has also become a massive weapon for cybercriminals.

To fix this, the Reserve Bank of India (RBI) dropped a massive bombshell in April 2026. They released a new discussion paper proposing a mandatory 1-hour delay on digital payments exceeding ₹10,000.

If implemented, this rule will fundamentally change how we send money in India. It is a classic battle between speed and security. On one hand, it could save millions of innocent people from losing their life savings. On the other hand, it could severely disrupt the convenience of instant payments.

In this comprehensive Paisaseekho guide, we are going to break down this proposed RBI rule in simple, everyday English. We will explore exactly how the delay will work, why the RBI thinks it is necessary, and weigh the pros and cons so you can decide if this is a brilliant idea or a massive digital headache.

1. What Exactly is the “RBI 1-Hour Delay UPI” Rule?

Let us imagine the RBI’s proposal has officially become law. How will this actually look on your smartphone screen?

Suppose you need to send ₹15,000 to your cousin for a family function. You open Google Pay, PhonePe, or Paytm, enter your cousin’s UPI ID, and type in ₹15,000. You enter your PIN.

Here is what happens next under the new system:

- Instant Debit: You will get an SMS from your bank saying, “₹15,000 has been debited from your account.” Your balance will drop immediately.

- The Holding Pen: Your cousin will NOT receive the money. Instead, the money will be held in a digital “limbo” or holding area by your bank for exactly 60 minutes.

- The Cancellation Window: On your app screen, you will likely see a countdown timer that says: “Security Cooling Period Active.” Next to it, there will be a big red “Cancel Transaction” button.

- Final Settlement: If you do nothing for 60 minutes, the timer runs out, the transaction clears, and your cousin finally receives the ₹15,000 in their bank account.

The RBI calls this 60-minute window the “Golden Hour.” It is a deliberate pause designed to break the psychological grip of a scammer.

2. Why is the RBI Doing This? (The ₹23,000 Crore Crisis)

To understand why the RBI wants to slow down our world-class payment system, you have to look at the terrifying rise of cybercrime.

According to data from the National Cyber Crime Reporting Portal (NCRP), the total value of digital payment frauds in India jumped from ₹551 crore in 2021 to a mind-blowing ₹22,931 crore in 2025. There were nearly 28 lakh reported cases of fraud in 2025 alone.

But the type of fraud has changed.

Ten years ago, a hacker would try to break into your bank’s computer system to steal your money. Today, hackers do not attack the bank; they attack you.

The Rise of “Authorized Push Payment” (APP) Frauds

Almost all major frauds today are behavioral crimes. Scammers use psychological manipulation to make you voluntarily transfer the money yourself.

Here are the three most common examples:

- The Fake Electricity Scam: You get a scary SMS saying your home’s electricity will be cut off in 30 minutes because your previous bill bounced. Panicking, you call the number provided, and a “customer care agent” guides you to urgently transfer ₹20,000 to avoid sitting in the dark.

- The Digital Arrest Scam: A person pretending to be a CBI or Customs officer calls you on a video call. They claim your Aadhaar card was found in a package containing illegal drugs. They threaten you with “Digital Arrest” and demand you transfer ₹5 Lakhs to a “government safe account” to prove your innocence.

- The Deepfake Friend Scam: You get a video call from a close friend (whose face and voice have been cloned using AI). They claim they are in a hospital after a car crash and desperately need you to transfer ₹50,000 immediately.

In all these scenarios, the scammer creates extreme panic. They do not let you think logically. You transfer the money, the scammer instantly withdraws it from an ATM, and the money is gone forever.

The RBI realized that once the money is transferred, recovering it is almost impossible. The only way to stop this is to add a “circuit breaker” into the system. A one-hour delay gives the victim time to hang up the phone, call their real friends or family, realize they have been scammed, and smash the “Cancel” button before the criminal gets the cash.

3. What are the RBI 1-Hour Delay UPI Rule Exemptions?

The moment the RBI announced this discussion paper, a wave of panic swept across social media. People asked, “If I go to buy a TV for ₹40,000, do I have to stand at the electronics shop for an hour waiting for the payment to clear?”

The answer is No.

The RBI is very smart about this. They know that slowing down daily commerce would ruin the economy. Therefore, the proposed 1-hour delay will primarily apply only to Person-to-Person (P2P) transfers.

The Merchant Exemption

If you scan a verified business QR code at a grocery store, a restaurant, an electronics shop, or pay online on Amazon or Swiggy, the transaction will remain 100% instant, regardless of whether the amount is ₹10 or ₹1 Lakh.

The “Whitelisting” Hack

What if you need to pay your rent of ₹25,000 to your landlord every month? Having your landlord wait an hour every single time is annoying.

To solve this, the RBI proposed a Whitelisting Mechanism. Inside your banking app, you will be able to mark specific people (like your landlord, your spouse, or your parents) as “Trusted Beneficiaries.” Once a person is on your whitelist, any future payments you send them (no matter how large) will bypass the 1-hour delay and go through instantly.

4. The Pros: Why the Delay is a Brilliant Idea

If you look at this rule purely from a safety perspective, it is a massive win for the consumer.

1. The Ultimate Panic Button

For the first time in Indian banking history, everyday users will have a genuine “Undo” button. If you accidentally type ₹50,000 instead of ₹5,000 and hit send, you no longer have to beg the receiver to send the money back. You just cancel it.

2. Protecting Vulnerable Senior Citizens

Our parents and grandparents are the prime targets of digital arrest and impersonation scams. They are not as tech-savvy and are easily intimidated by fake police callers. Giving them a 60-minute cooling-off period to consult with their children could single-handedly save the life savings of millions of senior citizens.

3. Killing the “Mule Account” Network

Scammers never use their own bank accounts. They use “Mule Accounts” (accounts opened using stolen identities of poor villagers). When you send money to a scammer, they instantly transfer that money across five different mule accounts in two minutes to hide the trail. If the initial transfer is paused for an hour, the bank’s fraud detection software gets time to analyze the receiver’s account. If the receiving account looks suspicious, the bank can proactively block the transfer.

5. The Cons: Why Bankers and Fintechs are Worried

While the intention behind the rule is noble, the banking and tech industry has responded with serious skepticism. Here are the major problems with the proposal:

1. It Kills the “Instant” Magic of UPI

The reason UPI became the most successful digital payment system on the planet is speed. We have been trained to expect sub-second settlements. Introducing friction, even for a good reason, feels like a massive step backward. Many fintech leaders argue that if you make UPI annoying to use, people will just go back to using physical cash for large transactions.

2. A Massive Operational Nightmare for Banks

Right now, the computers at the National Payments Corporation of India (NPCI) and your bank process a transaction and instantly forget about it.

If this rule passes, the bank’s servers will have to hold the money in suspense, run a 60-minute timer, track thousands of pending cancellations, and then release the funds. UPI processes over 800 million transactions every single day. Holding even a tiny fraction of these for an hour requires a totally different IT architecture and massive, expensive server upgrades for the banks.

3. Scammers Will Just Adapt

Criminals are clever. Critics point out that if a scammer can convince a victim to transfer ₹5 Lakhs, they can easily convince the victim to bypass the delay.

For example, the scammer will just say on the phone: “Sir, to complete the police verification immediately, please add this account to your ‘Trusted Whitelist’ first, and then send the money.” Once the victim whitelists the scammer, the 1-hour delay is bypassed, and the money is stolen anyway.

4. The Business Delay

Not all business is done through registered merchant QR codes. A lot of small, informal business owners (like independent freelancers, local plumbers, or freelance wedding photographers) accept payments via their personal UPI numbers. If they finish a job and demand ₹15,000, they will have to awkwardly wait around for an hour to ensure the customer doesn’t cancel the payment before leaving.

6. What Else is the RBI Proposing to Stop Fraud?

The 1-hour delay is the headline grabber, but the RBI’s discussion paper also suggested several other powerful tools to put control back in your hands:

- The “Kill Switch”: The RBI wants every banking app to have a giant, easy-to-find “Kill Switch.” If you suspect you are being scammed, you hit this button, and it instantly blocks all digital payments from your account (UPI, Net Banking, Debit Cards) until you visit a branch to unlock it.

- Extra Authentication for the Elderly: For senior citizens making transfers above ₹50,000, the RBI suggests requiring a secondary approval from a pre-designated “trusted family member” before the money leaves the account.

- Capping Mule Accounts: The RBI proposed a strict cap on “unverified” bank accounts. Any account that hasn’t undergone strict KYC checks will not be allowed to receive more than ₹25 Lakhs in a year, severely hurting the money-laundering operations of big scam syndicates.

Conclusion: A Necessary Friction

So, is the RBI’s proposed 1-hour delay on digital payments a good idea?

The answer depends on who you ask. If you are a young, tech-savvy millennial who frequently sends large amounts of money to friends to split bills, this rule will feel like an incredibly annoying speedbump.

But if you look at the broader picture—a country where ₹23,000 crore was stolen from innocent, hard-working people in a single year—the perspective changes. The RBI’s proposal marks a historical shift in India’s digital journey: a shift from “Speed-First” to “Security-First.” Yes, waiting an hour for a large payment to clear is inconvenient. But the slight inconvenience of a cooling-off period is a very small price to pay to ensure that your parents, your friends, and even you are protected from a momentary lapse in judgment that could drain your life savings.

As the RBI gathers feedback from the public and banks throughout early 2026, it is highly likely we will see a refined version of this rule implemented soon. Until then, the best defense against digital fraud remains your own common sense: never share your PIN, never download screen-sharing apps on a stranger’s advice, and always remember that a real police officer will never ask you for a UPI transfer.

Frequently Asked Questions (FAQs) About the RBI 1-Hour Delay Rule

Q1: Is the 1-hour delay on UPI payments already active?

No. As of April 2026, it is just a “discussion paper” proposed by the Reserve Bank of India. The RBI is gathering feedback from banks and the public before making it an official, mandatory rule.

Q2: Which payments will be delayed under this new rule?

The proposed delay will apply to person-to-person (P2P) digital transfers (which includes UPI, IMPS, and NEFT) that exceed ₹10,000 per transaction.

Q3: If I buy a laptop for ₹40,000 at a retail store using UPI, will I have to wait an hour?

No! Payments made to verified merchants (Person-to-Merchant or P2M transactions), such as scanning a QR code at a shop, buying groceries, or paying on an e-commerce website, will remain 100% instant.

Q4: Can I cancel the payment during the 1-hour delay?

Yes. That is the entire purpose of the rule. During the 1-hour “Golden Hour” holding period, the sender will have the option to hit a cancel button in their banking app to stop the transfer and get their money back.

Q5: Will the money be deducted from my account immediately?

Yes. If you send ₹15,000, your bank account balance will immediately drop by ₹15,000. However, the receiver’s bank will hold the money and only credit it to their account after the 1-hour timer expires.

Q6: Why did the RBI choose ₹10,000 as the limit?

According to the National Cyber Crime Reporting Portal (NCRP), transactions above ₹10,000 make up only 45% of total fraud cases by volume, but they account for a massive 98.5% of total money lost. Targeting this specific amount tackles the biggest financial losses without disrupting small, daily transactions.

Q7: What if I need to send money urgently for a medical emergency?

The RBI has proposed a “Whitelisting” feature. You will be able to mark trusted individuals (like family members or regular vendors) in your banking app. Once whitelisted, payments to them will bypass the 1-hour delay and go through instantly, even if the amount is huge.

Q8: What is an “Authorized Push Payment” (APP) fraud?

APP fraud happens when a scammer uses psychological tricks (like pretending to be a bank official or a police officer) to scare you into voluntarily transferring money to them. Because you authorized the payment yourself with your PIN, traditional bank security systems do not block it.

Q9: Does this rule apply to NEFT and RTGS as well?

While the primary focus is on instant payment rails like UPI and IMPS (because that is where the frauds happen fastest), the broad wording of the RBI discussion paper suggests that the 1-hour cooling-off period could be applied across all major digital fund transfer mechanisms for individual accounts.

Q10: What is the “Kill Switch” proposed by the RBI?

Along with the delay, the RBI wants banks to introduce a “Kill Switch” feature. If a customer realizes their phone is hacked or they are being scammed, they can hit this switch to instantly disable all outgoing digital payments (UPI, cards, net banking) across all their connected devices.