TL;DR: Key Takeaways on Car Loans Interest Rates in April 2026

If you are at the dealership right now, here is the quick breakdown of the market:

- The Rate Range: Most top banks are offering interest rates between 8.75% and 11.00%, depending on your credit score and the type of vehicle.

- The EV Advantage: “Green Car Loans” for electric vehicles are roughly 0.10% to 0.25% cheaper than standard petrol/diesel car loans.

- Processing Fees: Expect to pay between 0.50% and 1% of the loan amount, though many banks (like SBI) often waive this for existing “Pre-approved” customers.

- The CIBIL Factor: If your score is above 750, you can negotiate for the “floor rate.” If it’s below 700, expect a risk premium of at least 1% to 2% on top of the base rate.

- Fixed vs. Floating: Most car loans in India are fixed-rate. However, some PSU banks like PNB offer floating-rate options that might benefit you if the RBI cuts rates later in 2026.

Introduction

April 2026 has arrived, and for many, it’s the season of new beginnings—and new cars. Whether you are eyeing a rugged SUV for weekend getaways or a sleek electric sedan for your daily commute, the biggest hurdle isn’t choosing the color; it’s choosing the right financier.

The Indian auto loan market is currently navigating a high-interest rate environment. With the global “energy shock” and domestic inflation staying sticky, the Reserve Bank of India (RBI) has kept the Repo Rate elevated. Consequently, banks have adjusted their lending rates upward, making your monthly EMI slightly heavier than last year.

However, competition among top lenders like SBI, HDFC, ICICI, and PNB remains fierce. From “Green Car Loans” for EVs to processing fee waivers for high-CIBIL scorers, banks are pulling out all the stops to win your business.

In this comprehensive guide, we compare the latest car loan interest rates, processing charges, and hidden costs as of mid-April 2026.

1. Comparing the Big Four: Car Loan Rates in April 2026

When choosing a lender, you need to look beyond just the percentage. Please note that these are the rates as of 13 April, 2026. Here is how the top four players in the Indian market stack up right now:

State Bank of India (SBI)

SBI remains the benchmark for affordable car loans. Their “New Car Loan Scheme” is highly popular due to its transparency.

- Interest Rate: 8.85% to 9.75% (Fixed).

- Processing Fee: Nil to 0.50% (often waived for digital applications via YONO).

- Feature: No pre-payment penalty after 12-24 months.

HDFC Bank

HDFC specializes in speed. Their “ZipDrive” instant car loans are designed for existing customers who want an approval letter in minutes.

- Interest Rate: 9.10% to 10.50%.

- Processing Fee: Flat fee ranging from ₹3,500 to ₹6,500.

- Feature: High funding (up to 100% on-road price for select models).

ICICI Bank

ICICI Bank offers highly customized EMI structures, including “Step-up” EMIs for young professionals whose income is expected to grow.

- Interest Rate: 9.25% to 11.00%.

- Processing Fee: 1% of the loan amount.

- Feature: Extensive tie-ups with luxury car brands for special promotional rates.

Punjab National Bank (PNB)

As a PSU bank, PNB often provides the most competitive “floor” rates, especially for government employees and high-net-worth individuals.

- Interest Rate: 8.75% to 9.60%.

- Processing Fee: 0.25% to 0.50%.

- Feature: Offers a specific “PNB Green Car” loan with a 0.20% discount for EVs.

2. What Are the Exact Car Loan Interest Rates and Processing Charges for Top Banks in April 2026?

While we discussed the general features of the major players above, the numbers are what truly matter when you are sitting at the dealership. To give you the most accurate picture, we have compiled the latest, updated data (as of mid-April 2026) across both private and public sector banks.

If you are planning to take a standard loan of ₹5 Lakhs for a tenure of 5 years, here is exactly what you can expect in terms of interest rates, your estimated monthly EMI, and those sneaky processing fees:

| Bank Name | Interest Rate (p.a.) | Estimated EMI (₹5 Lakh, 5 Years) | Processing Fee |

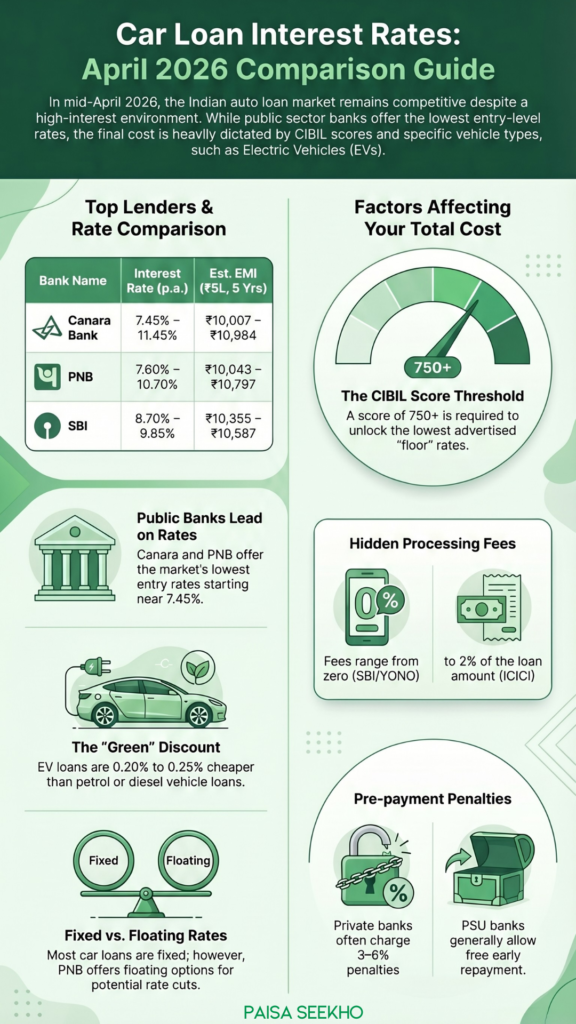

| Canara Bank | 7.45% – 11.45% | ₹10,007 – ₹10,984 | 0.25% |

| Punjab and Sind Bank | 7.50% – 14.00% | ₹10,019 – ₹11,634 | 0.25% |

| Punjab National Bank (PNB) | 7.60% – 10.70% | ₹10,043 – ₹10,797 | Up to 0.25% |

| Bank of Baroda | 7.60% – 11.35% | ₹10,043 – ₹10,959 | Up to ₹2,000 |

| Federal Bank | 7.60% – 9.00% | ₹10,198 onwards | Up to 1% |

| HDFC Bank | 8.15% onwards | ₹10,174 onwards | Up to 0.5% |

| ICICI Bank | 8.50% onwards | ₹10,258 onwards | Up to 2% |

| State Bank of India (SBI) | 8.70% – 9.85% | ₹10,355 – ₹10,587 | ₹750 – ₹1,500 |

Note: The rates mentioned above are updated as of April 13, 2026. Keep in mind that “onwards” indicates the absolute lowest floor rate, which is typically reserved for pre-approved customers with exceptional CIBIL scores (750+).

A Quick Analysis of the Numbers

Looking at the data, Canara Bank and Punjab and Sind Bank are currently offering the lowest entry-level interest rates in the market, pushing the EMI for a ₹5 Lakh loan down to the ₹10,000 mark.

However, notice the massive range in the public sector banks. While Punjab and Sind Bank starts at a highly attractive 7.50%, it can stretch all the way up to 14.00% if your credit profile is poor. In contrast, SBI has a much tighter, more predictable range (8.70% to 9.85%), meaning the “worst-case scenario” rate at SBI is still heavily capped, protecting you from massive EMI shocks.

When comparing these, do not forget to factor in the Processing Fee column. A 2% processing fee at ICICI Bank on a ₹10 Lakh loan is ₹20,000 upfront, whereas Bank of Baroda caps this at just ₹2,000, saving you ₹18,000 before you even start paying your EMIs!

3. Factors That Will Decide Your Final Interest Rate

The “headline rate” you see in advertisements is almost never what you get. Banks use a Risk-Based Pricing model. Your actual interest rate will be determined by four key factors:

- Credit (CIBIL) Score: This is the most important factor. A score of 750+ gets you the lowest rate. A score of 650 might result in an interest rate that is 1.5% higher.

- Vehicle Category: Loans for hatchbacks and sedans are standard. Loans for luxury cars (above ₹25 Lakhs) or commercial vehicles often attract a higher “Commercial Risk” premium.

- The EV Incentive: As part of the national push for green mobility, almost every bank now offers a “Green Loan.” These are specifically for Electric Vehicles and are generally 20-25 basis points (bps) lower than regular rates.

- Loan Tenure: Interestingly, a 3-year loan might have a lower interest rate than a 7-year loan because the bank’s risk of your default increases over a longer period.

4. Hidden Costs: Don’t Forget the Fine Print

The interest rate is just one part of the cost. When you sign that loan agreement, keep an eye out for these three “silent” expenses:

- Processing Fees: This is an upfront cost. While 1% sounds small, on a ₹20 Lakh loan, that is ₹20,000 gone before you even drive the car. Always ask for a waiver or a flat-fee cap.

- Foreclosure/Pre-payment Charges: If you get a bonus and want to pay off your loan early, most private banks will charge you 3% to 6% of the remaining principal as a “penalty.” PSU banks like SBI and PNB generally do not charge this for individual borrowers.

- Documentation & Stamp Duty: These are small state-level charges (usually ₹500 to ₹2,500) required to create a “Hypothecation” (the bank’s legal claim) on your car’s RC (Registration Certificate).

5. Conclusion: Is April 2026 a Good Time to Borrow?

Borrowing in a high-interest environment requires strategy. While rates are higher than they were a few years ago, the stability of the Indian economy makes car loans a safe bet for most salaried professionals.

The Winning Strategy:

If you have a high CIBIL score, do not settle for the dealer’s “preferred” financier. Dealers often get a commission to push you toward specific private banks. Instead, walk into your own bank branch with a copy of your salary slip and your CIBIL report. Ask for their “best rate” for an existing customer. You will be surprised how much you can save simply by comparing and negotiating.

Frequently Asked Questions (FAQs): Car Loan Interest Rates

Q1: What is the lowest car loan interest rate in April 2026?

Currently, public sector banks like PNB and SBI are offering the lowest “floor rates,” starting at approximately 8.75% to 8.85% for individuals with a CIBIL score above 750.

Q2: Are EV car loans cheaper than petrol car loans?

Yes. Most banks offer a “Green Car Loan” incentive, providing a 0.20% to 0.25% discount on the standard interest rate to encourage the adoption of electric vehicles.

Q3: Does my CIBIL score really affect my car loan EMI?

Absolutely. Banks use risk-based pricing. A person with a 780 CIBIL score might get a loan at 8.85%, while someone with a 680 score might be charged 10.50%. Over a 5-year loan of ₹10 Lakhs, this difference can cost you over ₹50,000 in extra interest.

Q4: Can I get 100% on-road funding for a car?

Some private banks like HDFC and ICICI offer 100% on-road funding (which includes insurance and registration) to “Elite” or “Pre-approved” salary account holders. However, most standard loans cover 80% to 90% of the ex-showroom price.

Q5: What is the maximum tenure for a car loan in India?

Most banks allow a maximum tenure of 7 years (84 months). While a longer tenure reduces your monthly EMI, it significantly increases the total interest you pay to the bank.

Q6: Are there any hidden charges in a car loan?

Beyond interest, you must account for Processing Fees (0.5% to 1%), Documentation Charges, and potential Foreclosure Penalties if you decide to close the loan early.

Q7: Is it better to take a car loan from a bank or the dealer’s finance partner?

Dealer finance is convenient and fast, but bank-direct loans are almost always cheaper. Dealers often have “mark-ups” or commissions built into the rate they offer you. Always compare the dealer’s quote with a quote from your own bank.

Q8: Can I transfer my high-interest car loan to another bank?

Yes, this is called a Car Loan Balance Transfer. If you find a bank offering a rate that is at least 1% lower than your current rate, you can switch. However, factor in the foreclosure charges of your old bank and the processing fees of the new bank before making the move.

Q9: Do I need a co-applicant for a car loan?

If your individual income is not enough to meet the bank’s “Debt-to-Income” ratio, you can add a spouse or parent as a co-applicant to club your incomes and increase your loan eligibility.

Q10: Will my car loan interest rate go down if the RBI cuts the Repo Rate?

Most car loans in India are Fixed Rate loans, meaning your EMI stays the same for the entire tenure regardless of RBI moves. Only “Floating Rate” car loans (rare in the private sector but available at some PSU banks) will benefit from an RBI rate cut.

Source