TL;DR: Key Takeaways on Bank Interest TDS in 2026

If you are heading to the bank today and just need the fast facts, here is your summary:

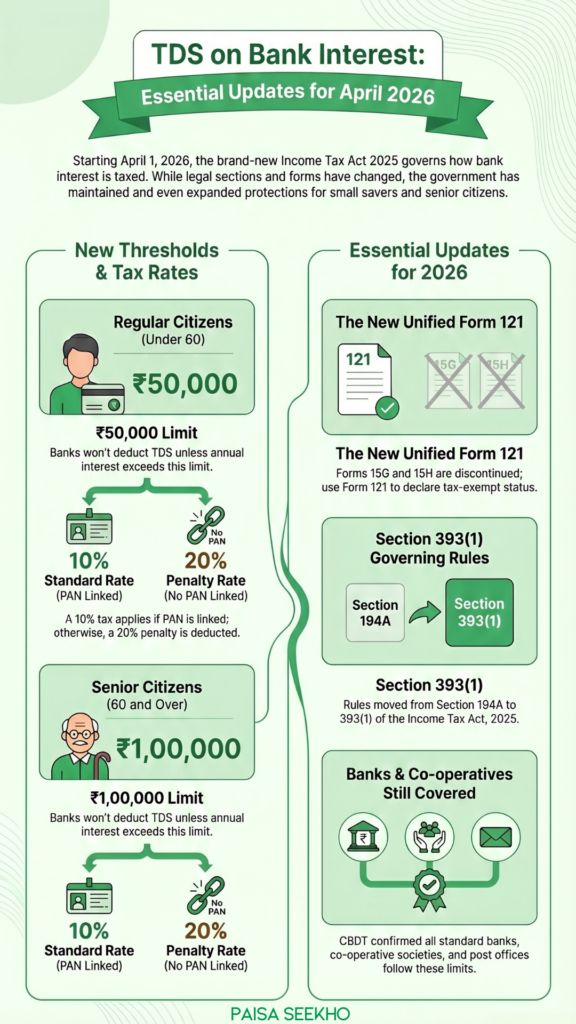

- The New Law: The rules for TDS on bank interest have moved from the old Section 194A to the brand-new Section 393(1) of the Income Tax Act, 2025.

- The Panic is Over: The Income Tax Department has officially clarified that the definition of a “banking company” still covers all your standard and co-operative banks. Nothing changes for the depositor.

- The General Limit: For regular citizens (below 60 years), banks will not deduct any TDS until your total interest income crosses ₹50,000 in the financial year.

- The Senior Citizen Limit: For senior citizens (60 years and above), the TDS-free threshold remains at a highly generous ₹1,00,000 per year.

- The Deduction Rate: If you cross the limit, the bank deducts 10% as TDS. If you haven’t linked or submitted your PAN, they will deduct a massive 20%.

- The Form Upgrade: The old Forms 15G and 15H are officially dead. To stop the bank from deducting TDS, you must now submit the unified Form 121.

Introduction

If you rely on the interest from a Fixed Deposit (FD) or a savings account to supplement your monthly income, April 1, 2026, probably brought a wave of anxiety.

With the massive rollout of the brand-new Income Tax Act, 2025, rumors immediately started swirling across social media. The new legal code tweaked the official definition of a “banking company.” This minor change in legal wording sparked widespread panic among depositors. People feared that certain banks and co-operative societies would lose their tax exemptions and start aggressively deducting Tax Deducted at Source (TDS) on every single rupee of interest earned, destroying the monthly cash flow of millions of senior citizens.

Thankfully, the Income Tax Department (CBDT) stepped in on March 30, 2026, to clear the air.

If you have money sitting in a bank, a post office, or a co-operative society, the rules governing how your interest is taxed have shifted to a new section, but the fundamental protections remain completely intact. In this comprehensive, jargon-free guide, we will break down exactly what happened, explain the new limits under the 2025 Act, and show you the brand-new form you need to submit to protect your interest income from the taxman.

What Caused the Confusion Under the New Income Tax Act 2025?

To understand the panic, we need to look at the legal wording of the new law.

Under the old 1961 Act, the definition of a “banking company” was incredibly broad. It explicitly included massive commercial banks governed by the Banking Regulation Act, 1949, and specifically name-dropped other financial institutions under Section 51.

When the new Income Tax Act, 2025 was drafted, the government tried to make the legal text shorter and cleaner. Under the new Section 402, they defined a “banking company” but forgot to explicitly mention those extra institutions from Section 51.

This omission terrified accountants and investors. They assumed that because co-operative banks and certain post office institutions were no longer “explicitly named,” they would no longer be legally allowed to offer the ₹50,000/₹1,00,000 threshold exemptions and would have to deduct TDS from the very first rupee of interest.

The CBDT Clarification

Just two days before the new law went live, the Central Board of Direct Taxes (CBDT) issued a massive sigh of relief via their official social media channels. They clarified that Section 51 of the Banking Regulation Act inherently covers these institutions anyway. Therefore, they still automatically qualify as “banking companies” under the new 2025 Act.

The Bottom Line: Your local co-operative bank and post office will continue to offer you the exact same TDS protections as massive commercial banks like SBI or HDFC.

What Are the Prescribed Limits for TDS on Bank Interest in 2026?

Under the new 2025 Act, the rules for deducting tax on your interest income (other than securities) are legally governed by Section 393(1).

The government wants to ensure that small savers and retirees are not burdened by unnecessary tax paperwork. Therefore, they force the bank to ignore small amounts of interest. The bank will only trigger the TDS mechanism if your combined interest earnings cross specific thresholds:

1. For Regular Citizens (Below 60 Years)

If you are a non-senior citizen, the TDS exemption limit on bank and post office deposits is ₹50,000 per financial year.

(Note: This is a massive win for investors, as this limit was recently bumped up from the old ₹40,000 benchmark to ₹50,000 starting FY 2025-26).

2. For Senior Citizens (60 Years and Above)

The government provides a massive safety net for the elderly who rely entirely on FD interest for survival. If you are a senior citizen, banks will not deduct a single rupee of TDS until your total interest income crosses ₹1,00,000 per financial year.

Important Warning on “Branch-Wise” Calculation:

In the old days, smart investors would open three different FDs at three different branches of the exact same bank to keep the interest at each branch below the limit. You can no longer do this. Because all modern banks operate on a Core Banking System (CBS), the system calculates your interest across all branches of that bank combined based on your PAN card.

How Much TDS Gets Deducted and How Can You Avoid It?

If your total interest pushes past the ₹50,000 or ₹1 Lakh threshold, the bank has a legal obligation to step in and act as a tax collector for the government.

- The Standard Rate (10%): If your PAN is actively linked to your bank account, the bank will deduct 10% of your total interest income and send it to the Income Tax Department. (For example, if you earn ₹60,000 in interest, the bank deducts ₹6,000 and deposits ₹54,000 into your account).

- The Penalty Rate (20%): If you have neglected to submit your PAN card to the bank, the government punishes you by forcing the bank to deduct a massive 20% TDS.

How to Legally Stop the Bank from Deducting TDS

What if you earn ₹80,000 in FD interest, but you have no other salary or business income? Because your total income is far below the basic ₹3 Lakh/₹4 Lakh tax-free slab, you theoretically owe zero tax to the government. It is completely unfair for the bank to deduct 10% TDS, forcing you to wait a whole year to claim a refund.

The government knows this, which is why they offer a self-declaration escape route.

For decades, Indians used Form 15G and Form 15H. However, as part of the April 2026 overhaul, these old forms have been permanently retired. If you want to prevent the bank from deducting TDS this year, you must submit the newly introduced Form 121. This is a unified self-declaration form. By signing and submitting Form 121 to your bank (which can easily be done through your net banking app), you are legally declaring to the government: “My total estimated annual income is below the taxable limit, so please do not touch my bank interest.”

Does TDS Mean Your Final Tax Liability is Settled?

This is the biggest, most dangerous misconception among Indian taxpayers.

Millions of people assume that because the bank deducted 10% TDS, their tax obligations on that FD are completely settled, and they don’t need to report the interest when filing their Income Tax Return (ITR). This is entirely false.

TDS is merely an “Advance Tax.” It is a mechanism for the government to collect revenue throughout the year to prevent mass tax evasion.

Your Fixed Deposit interest is fully taxable. It gets added to your total income under the head “Income from Other Sources.” If you are a high-earning corporate employee sitting in the 30% tax bracket, the bank only deducted 10%. When you file your ITR at the end of the year, you are legally required to calculate your total tax at the 30% rate, subtract the 10% the bank already paid on your behalf, and pay the remaining 20% directly to the government.

If you hide this interest income, the tax department’s advanced AI systems (which track every single TDS deduction linked to your PAN via your Annual Information Statement) will instantly catch the discrepancy and send you a penalty notice.

Conclusion:

The transition to the Income Tax Act, 2025, initially caused a few sleepless nights for depositors, but the final outcome is highly positive.

By clarifying the rules, the CBDT has ensured that the foundational protections for small savers and senior citizens remain perfectly intact. The thresholds of ₹50,000 and ₹1,00,000 provide massive breathing room for middle-class families trying to beat inflation with safe banking products.

As we navigate this new financial year, your action plan is simple: ensure your PAN is officially linked to every single bank account you own to avoid the 20% penalty rate, calculate your estimated total income for the year, and if you fall below the taxable slab, log into your banking app today and submit the new Form 121 before your first interest payout hits!

Frequently Asked Questions (FAQs): TDS on Bank Interest

Q1: What is the new section for TDS on bank interest under the 2025 Act?

Starting April 1, 2026, the rules governing TDS on interest income (other than securities) have been moved from the old Section 194A to the new Section 393(1) of the Income Tax Act, 2025.

Q2: Will my bank deduct TDS if my interest is ₹45,000?

No. For regular citizens (below 60 years), banks will only deduct TDS if your total interest from that bank exceeds ₹50,000 in a single financial year. Since your interest is ₹45,000, no TDS will be deducted.

Q3: What is the TDS exemption limit for senior citizens in 2026?

For senior citizens (aged 60 and above), the TDS exemption threshold on bank and post office deposits is a highly generous ₹1,00,000 per financial year.

Q4: Did the new 2025 tax law remove TDS exemptions for co-operative banks?

No. This was a massive rumor. The Income Tax Department explicitly clarified that institutions covered under Section 51 of the Banking Regulation Act (like co-operative banks) are still classified as “banking companies” and will continue to offer the standard ₹50k/₹1 Lakh threshold exemptions.

Q5: How much TDS does the bank deduct if I cross the limit?

If your interest exceeds the threshold, the bank will deduct 10% of your total interest income as TDS. However, if you have not provided your PAN card to the bank, they are legally forced to deduct a massive 20%.

Q6: What happened to Form 15G and Form 15H?

As part of the April 2026 tax overhaul, Forms 15G and 15H have been permanently discontinued. They have been replaced by a single, unified self-declaration form called Form 121.

Q7: Who should submit the new Form 121 to the bank?

You should submit Form 121 if your total estimated annual income (including the bank interest) is below the basic tax-free exemption limit. Submitting this form legally instructs the bank not to deduct any TDS from your interest payouts.

Q8: If I have two FDs in two different branches of SBI, how is the limit calculated?

Modern banks use a Core Banking System (CBS) linked directly to your PAN. The bank will combine the interest earned from Branch A and Branch B. If the combined total crosses the ₹50,000 threshold, the bank will deduct TDS, even if individual branch payouts were small.

Q9: Does TDS apply to interest earned in a normal savings account?

Yes, the threshold limit (₹50,000 or ₹1 Lakh) applies to the aggregate interest earned from both Fixed Deposits (FDs), Recurring Deposits (RDs), and your standard savings accounts held with that specific bank.

Q10: Since the bank already deducted 10% TDS, is my FD interest completely tax-free now?

Absolutely not. TDS is only an advance tax. You must report all your bank interest under “Income from Other Sources” when filing your Income Tax Return. If your total income places you in a higher tax slab (e.g., 20% or 30%), you must pay the remaining balance tax directly to the government.

Source: