Quick summary: Some companies generate large profits as shown in their financial accounts and even distribute dividends to shareholders, but pay little or no income tax. They manage this by claiming various deductions, exemptions, and incentives under the Income Tax Act. The concept of Minimum Alternate Tax (MAT) under Section 115JB was designed precisely to address this. It says: regardless of how many deductions a company claims, it must pay tax on at least 15% of its “book profit” (the profit shown in its accounts as per the Companies Act). Form 29B is the audit report, certified by a Chartered Accountant, that formally computes and certifies this book profit figure. Filing it correctly is a mandatory compliance step for companies subject to MAT.

The Problem MAT Was Designed to Solve

To understand Form 29B, you first need to understand why MAT exists.

Under the normal provisions of the Income Tax Act, companies compute their taxable income by starting with their net profit and then applying various deductions, exemptions, and allowances. A company might, for example, claim accelerated depreciation on newly purchased machinery, carry forward losses from earlier years, or avail of incentives for operating in a Special Economic Zone. After all of these adjustments, a company’s taxable income under normal income tax provisions can be significantly lower than the profit it actually reported to its shareholders.

In extreme cases, a profitable company could end up with zero or near-zero taxable income and therefore pay no meaningful income tax, even while distributing healthy dividends. These entities became known as “zero-tax companies,” and they created a perception of unfairness in the tax system.

MAT was introduced to address this phenomenon. These were entities that, despite generating substantial book profits and often distributing dividends to shareholders, managed to reduce their taxable income to negligible or zero levels under the normal provisions of the Income Tax Act.

The solution: Section 115JB of the Income Tax Act, which creates a parallel tax computation based on the company’s book profit (profit as per the accounts prepared under the Companies Act) rather than its Income Tax Act taxable income. If the tax computed on book profit is higher than the tax computed under normal provisions, the company pays the higher amount.

What Is Minimum Alternate Tax (MAT)?

MAT under Section 115JB works like this:

Every company must compute its tax liability in two ways simultaneously:

- Normal tax: computed on taxable income as per the normal Income Tax Act provisions, after all deductions, exemptions, and allowances

- MAT: computed at 15% of the book profit (as certified in Form 29B), plus applicable surcharge and 4% Health and Education Cess

The company then pays whichever amount is higher.

For FY 2025-26, the effective MAT rate for domestic companies, including surcharge and cess, is:

- Approximately 17.01% for companies with book profit between ₹1 crore and ₹10 crore (15% + 7% surcharge + 4% cess)

- Approximately 17.47% for companies with book profit above ₹10 crore (15% + 12% surcharge + 4% cess)

For foreign companies, the applicable rate differs.

From Assessment Year 2020-21, the threshold is clearly stated: every company where the income is less than 15% of the book profit is required to obtain a report from a Chartered Accountant in Form 29B.

What Is Book Profit?

“Book profit” in Section 115JB is not the same as the net profit in your Profit and Loss account. It starts with the net profit per P&L (as prepared under the Companies Act) and then requires specific additions and deductions as prescribed by Section 115JB(2).

Mandatory Additions to Net Profit

The following amounts, if already debited to the Profit and Loss account, must be added back to arrive at book profit:

- Income tax paid or payable, and provision for income tax

- Dividend paid or proposed (equity or preference)

- Amounts transferred to any reserves other than statutory reserves (such as transfer to general reserve, capital redemption reserve, or similar)

- Provisions for unascertained or contingent liabilities (such as provision for doubtful debts, general provision)

- Provision for losses of subsidiary companies

- Deferred tax charged to P&L (net debit)

- Expenditure relating to income that does not form part of total income (income that is otherwise exempt)

- Notional losses on mark-to-market valuation of derivatives

Permitted Deductions from Net Profit

The following amounts are deducted to arrive at book profit:

- Amounts withdrawn from reserves or provisions where such amounts were added back in an earlier year

- Income that does not form part of total income under Section 10 (such as agricultural income, dividends received before abolition of DDT, and similar exempt items) to the extent credited to P&L

- Brought forward loss or unabsorbed depreciation, whichever is lower, as per the company’s own books of accounts (not the Income Tax Act computation; this is a subtle but important distinction)

- Notional gains on mark-to-market valuation of derivatives

- Amount of deferred tax credited to P&L (net credit)

- Profits of a sick industrial company up to the year it ceases to be sick (under certain conditions)

The final figure after all these additions and deductions is the book profit on which MAT is computed.

A Worked Example

Consider Horizon Private Limited for FY 2025-26:

| Item | Amount |

| Net profit per Profit and Loss Account (Companies Act) | ₹1,00,00,000 |

| ADD: Income tax provision debited to P&L | ₹5,00,000 |

| ADD: Provision for doubtful debts | ₹2,00,000 |

| ADD: Transfer to general reserve | ₹10,00,000 |

| Subtotal | ₹1,17,00,000 |

| LESS: Exempt income (long-term capital gains on equity under Section 10(38), where applicable) | ₹8,00,000 |

| LESS: Brought forward book loss (lower of book loss or unabsorbed depreciation as per books) | ₹15,00,000 |

| Book Profit as per Section 115JB | ₹94,00,000 |

MAT = 15% of ₹94,00,000 = ₹14,10,000 (plus surcharge and cess as applicable)

Normal tax on taxable income: say ₹20,00,000 taxable income at 25% tax rate = ₹5,00,000 (plus cess)

Since MAT (₹14,10,000) is higher than normal tax (₹5,00,000), Horizon pays ₹14,10,000 as its tax for the year.

MAT credit: The excess of MAT over normal tax, which is ₹9,10,000, becomes a credit that the company can carry forward for up to 15 years and use to reduce its tax in future years when normal tax exceeds MAT.

This example is simplified and illustrative. Actual book profit computation involves many more line items depending on the company’s specific financial statements.

What Is Form 29B?

Form 29B is the prescribed audit report under Rule 40B of the Income Tax Rules, 1962, which must be obtained and filed by a company subject to Section 115JB. Form 29B is considered a significant audit report. A Chartered Accountant issues this report. Many people struggle with Minimum Alternate Tax (MAT) compliance. So, this form helps companies to certify their book profits.

It serves three specific purposes:

- Certification: The CA formally certifies that the book profit has been computed correctly in accordance with Section 115JB, after examining the company’s accounts and records.

- Compliance documentation: It provides the Income Tax Department with a verified document to assess whether the company has paid the correct amount of tax under MAT.

- MAT credit validation: It supports the company’s claim for MAT credit in future years by establishing the authenticated book profit and MAT figure for the current year.

Form 29B is not filed by the company directly. It is prepared and submitted electronically on the Income Tax e-filing portal by the CA using their Digital Signature Certificate (DSC). The company must then accept the form through their own portal login to complete the filing.

Structure of Form 29B: Parts A, B, and C

Form 29B consists of three parts: Part A, Part B, and Part C. While Part A applies to all business organizations in India, the applicability of Parts B and C is contingent on specific conditions.

Part A: Contains the general computation of book profit applicable to all companies. This includes the starting point (net profit as per P&L), all the additions and deductions prescribed under Section 115JB(2), and the final book profit figure. The CA certifies all these items here.

Part B: Applicable specifically to companies that have adopted Ind AS (Indian Accounting Standards), the Indian version of International Financial Reporting Standards. For Ind AS companies, additional adjustments are required per Section 115JB(2A) because Ind AS and the older Indian GAAP (Generally Accepted Accounting Principles) treat certain transactions differently. Part B captures these Ind AS-specific additions and deductions.

Part C: Applicable to companies for the year of first adoption of Ind AS (the “convergence year”) and subsequent years. It captures adjustments under Section 115JB(2C) relating to the convergence date: the specific point at which a company transitions its financial reporting from Indian GAAP to Ind AS. This transition creates one-time adjustments that need to be correctly reflected in the book profit computation.

The CA’s report section in Form 29B (as per Rule 40B) includes:

- An examination statement: the CA certifies that they have examined the accounts, records, balance sheet, and profit and loss account of the company

- A declaration that the book profit has been computed in accordance with Section 115JB

- Any qualifications or observations

- CA’s name, address, membership number, Firm Registration Number (FRN), UDIN, date, and place of signing

Who Must File Form 29B?

Only companies are eligible to file Form 29B. Filing is mandatory if the company is subject to MAT provisions under Section 115JB. Certification from a Chartered Accountant (CA) is mandatory.

This covers:

- Private limited companies

- Public limited companies

- One Person Companies (OPCs)

- Government companies and Public Sector Undertakings (PSUs)

- Foreign companies with a Permanent Establishment in India (subject to specific conditions)

Important: According to Section 115JB of the Income Tax Act of 1961, enterprises that are subject to the Minimum Alternate Tax (MAT), including those that are experiencing losses, are required to submit Form 29B. A business must have its accounts audited and file Form 29B even if it is losing money if it is required to pay taxes under section 115JB.

This is counterintuitive. Why would a loss-making company need to file Form 29B? Because book profit under Section 115JB can sometimes be positive even when the company reports a loss under normal tax provisions. For example, if the company has large provisions or reserve transfers that get added back in the book profit computation, the book profit may be positive despite an accounting loss in some scenarios.

Who does NOT need Form 29B:

- LLPs (Limited Liability Partnerships): LLPs are covered by AMT under Section 115JC, not MAT. They file Form 29C instead.

- Partnership firms: similarly covered by AMT, not MAT.

- Individuals, HUFs, AOPs, BOIs: not companies; not subject to Section 115JB.

- Companies that pay tax under normal provisions at a rate exceeding 15% of their book profit: since MAT does not trigger, Form 29B technically does not apply, though most companies file it as a matter of standard practice and compliance risk management.

MAT Credit: Carrying Forward and Setting Off

When a company pays MAT in a year (because MAT is higher than normal tax), the difference between MAT and normal tax is called MAT credit. This credit can be:

- Carried forward for up to 15 years

- Set off against the company’s tax liability in a future year when the normal tax computed under regular provisions exceeds the MAT for that year

In that future year, the company can reduce its tax payment by the available MAT credit balance (up to the extent that normal tax exceeds MAT for that year).

If a company pays MAT, the excess of MAT over normal tax can be carried forward for 15 years and set off in future years when regular tax becomes more than MAT.

The claim for MAT credit is made in Schedule MATC of the company’s ITR-6. The accumulated balance of MAT credit must be disclosed in the ITR every year, even in years when it is not being utilised, to preserve the carry-forward entitlement.

Why MAT Credit Matters

For companies in the growth phase, it is common to pay MAT for several years while investing heavily (and therefore claiming large deductions like accelerated depreciation). Once the company matures and its normal tax liability rises above the MAT threshold, the accumulated MAT credit can substantially reduce the cash tax outflow in those later years. Tracking and claiming MAT credit correctly is a meaningful tax planning tool.

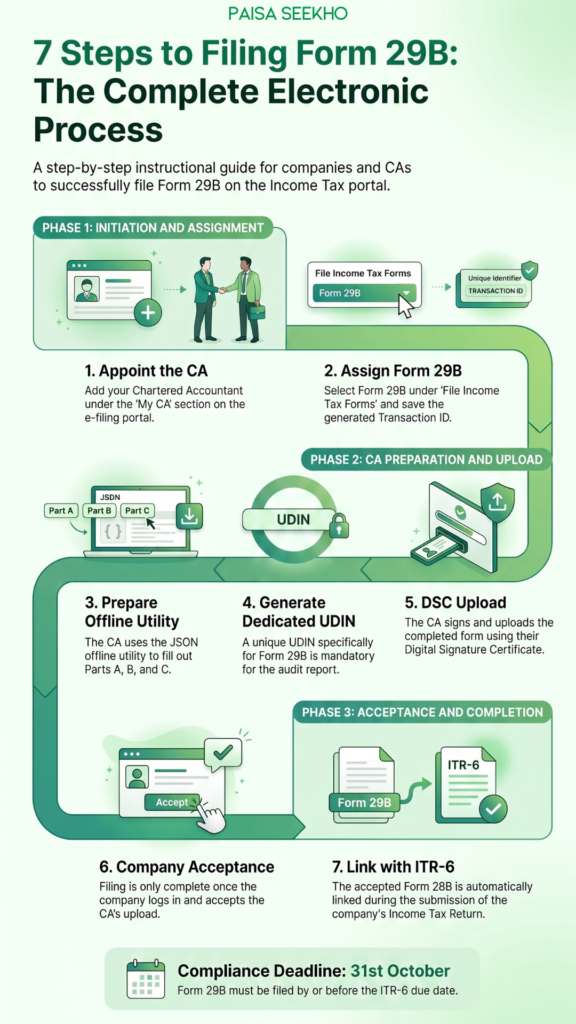

Step by Step Filing Process for Form 29B

The filing process is entirely electronic. Here is how it works:

- Step 1: The company logs into the Income Tax e-filing portal (incometax.gov.in) and goes to My CA under Authorised Partners. They add the CA who will file Form 29B.

- Step 2: The company goes to e-File → Income Tax Forms → File Income Tax Forms and selects Form 29B. They assign it to the appointed CA. A transaction ID is generated; the company should save this.

- Step 3: The CA receives the assignment and accepts it through their own portal login. They prepare the Form 29B using the offline utility (JSON utility), filling in all three parts as applicable to the company.

- Step 4: The CA generates a UDIN on the ICAI portal (udin.icai.org) specifically for the Form 29B report. A separate UDIN is required for Form 29B; the UDIN generated for the Section 44AB tax audit report (Form 3CA/3CB with Form 3CD) does not cover Form 29B.

- Step 5: The CA uploads the completed Form 29B using their Digital Signature Certificate (DSC) on the e-filing portal.

- Step 6: The company receives a notification that the CA has uploaded Form 29B. The company must log in and accept the form. Until the company accepts, the filing is not complete.

- Step 7: The accepted Form 29B is then linked with the company’s ITR-6 when the return is filed.

Due Dates for Form 29B

Form 29B must be filed before or along with the company’s Income Tax Return for the relevant assessment year. For companies that are required to get a tax audit done under Section 44AB, the ITR-6 filing due date is 31 October of the assessment year. Form 29B must be filed by or before that date.

For FY 2025-26 (AY 2026-27): Form 29B is due by 31 October 2026.

Some sources reference an earlier requirement that Form 29B be obtained one month before the return due date. However, the Income Tax Department’s official FAQ confirms that Form 29B must be furnished with or before the income tax return. The safest approach is to complete Form 29B well in advance of the ITR filing date so that the accepted form is ready before the company files its return.

Penalty for Non-Filing or Late Filing

Section 271BA of the Income Tax Act imposes a penalty for failure to obtain the audit report in Form 29B or failure to file it before the due date. The penalty for late filing of Form 29B can be as high as Rs 1,00,000 in some cases. However, Section 273B states that if you can state an appropriate reason for failing to file the form on the due date, you are not liable for any penalty under Section 271BA.

Accepted “reasonable causes” include sudden death or serious illness of the responsible person, loss of accounts due to fire or theft, or other circumstances genuinely beyond the company’s control. Not knowing about the requirement or simply being busy does not qualify.

Beyond the penalty, failing to file Form 29B can lead to:

- Denial of MAT credit claims in future years

- Heightened scrutiny during assessment

- Potential recomputation of MAT liability by the assessing officer without the benefit of the CA’s certified book profit

Form 29B vs Form 29C: What Is the Difference?

Section 115JC introduces Alternate Minimum Tax (AMT) for non-corporate taxpayers such as individuals, HUFs, partnerships, LLPs, and AOPs who claim deductions under Chapter VI-A Part C. These taxpayers must pay AMT at 18.5% (plus surcharge and cess) on adjusted total income if it exceeds regular tax liability. To comply, they must file Form 29C, an audit report certified by a Chartered Accountant.

| Form 29B | Form 29C | |

| Applicable to | Companies only | Non-corporate entities: individuals, HUFs, firms, LLPs, AOPs claiming specified deductions |

| Legal section | Section 115JB | Section 115JC |

| Tax type | Minimum Alternate Tax (MAT) | Alternate Minimum Tax (AMT) |

| Tax rate | 15% of book profit | 18.5% of adjusted total income |

| Basis of computation | Book profit (net profit per Companies Act plus/minus adjustments) | Adjusted total income (regular income plus deductions claimed under Chapter VI-A Part C) |

| When triggered | Company’s normal tax is lower than 15% of book profit | Non-corporate taxpayer’s normal tax is lower than 18.5% of adjusted total income |

| Credit carry-forward | 15 years | 15 years |

The practical relevance of AMT (Form 29C) for individuals and LLPs is most significant for those claiming deductions under infrastructure-linked provisions like Sections 80-IA, 80-IB, 80-IC, and similar. Most small businesses and professionals are unlikely to be affected by AMT since those special deductions are less commonly applicable at their scale.

How Form 29B Connects to the Tax Audit Process

Form 29B is separate from the tax audit report under Section 44AB (Forms 3CA/3CB with Form 3CD). However, in practice, the two are closely linked:

- A company required to file Form 29B is also almost always required to file a tax audit report under Section 44AB, since being a company with MAT liability implies accounts of a scale that would typically trigger the audit threshold

- Both require a CA with a Certificate of Practice

- Both are filed electronically on the same portal

- Both require separate UDINs

- Both must be filed and accepted by the company before the ITR-6 is submitted

A CA handling a company’s tax audit will typically also prepare and file Form 29B as part of the same engagement. However, they are distinct statutory compliances with distinct penalty provisions.

For a detailed understanding of the broader tax audit process, including what Form 3CD covers, see our articles on Form 3CA vs Form 3CB and the Form 3CD tax audit report explained.

Common Mistakes to Avoid

Incorrect starting point for book profit computation.

The starting point must be the net profit per the Profit and Loss Account prepared as per the Companies Act, not the income tax computation. Using the wrong figure as the starting point cascades errors through the entire computation.

Missing Ind AS adjustments (Parts B and C).

For Ind AS-adopting companies, Parts B and C of Form 29B are not optional. Omitting them when they are applicable creates an incomplete and technically deficient form.

Using the same UDIN as the tax audit report.

A separate UDIN is mandatory for Form 29B. The UDIN for the Section 44AB tax audit report does not extend to cover Form 29B.

Not tracking MAT credit year-wise.

MAT credit must be claimed correctly in Schedule MATC of ITR-6 every year. Failure to properly disclose the accumulated credit balance in each year’s return can jeopardise the ability to claim it in future years.

Company not accepting the form after CA uploads.

The CA uploads Form 29B; the company must separately log in and accept it. If the company does not accept, the form is treated as not filed. This is a surprisingly common oversight.

Treating losses as automatic exemption from MAT.

A company reporting a loss on its books may still have a positive book profit after the Section 115JB additions. Always compute the book profit even for loss-making companies to verify whether MAT applies.

MAT Under the Income Tax Act, 2025

India’s Income Tax Act, 2025 (effective from 1 April 2026, i.e., from Tax Year 2026-27) will carry forward the concept of MAT for companies, since ensuring minimum tax from profit-making companies remains a core policy objective. The specific section references will change as part of the broader renumbering of the Income Tax Act.

For FY 2025-26 (AY 2026-27): Form 29B continues to apply under Section 115JB as described in this article. All companies subject to MAT must file Form 29B by 31 October 2026.

The transition to the new Act’s equivalent provisions, with any restructured form, will apply from Tax Year 2026-27 (income earned from April 2026 onwards). Keep track of CBDT notifications and ICAI guidance as the new framework becomes operational. Our article on the April 2026 financial rule changes covers the broader context of what changes under the new Income Tax Act.

Frequently Asked Questions

1. Does Form 29B apply to every company?

No. It applies only to companies for which Section 115JB is triggered, meaning their normal income tax liability is lower than 15% of their book profit. Companies that pay normal tax above this threshold are not required to file Form 29B, though many file it anyway as a precautionary measure.

2. Is Form 29B required even if the company makes a loss?

Potentially yes. A company incurring a loss under the Income Tax Act’s normal provisions must still compute its book profit per Section 115JB. If the book profit is positive (because of mandatory additions to the net loss figure), MAT applies and Form 29B must be filed.

3. Can Form 29B be revised?

No, Form 29B cannot be revised once submitted. However, some sources indicate that a fresh filing may be possible in specific circumstances. Given the stakes involved, it is critical to get the form right before submission. Consult your CA before accepting the form on the portal.

4. Is a UDIN required for Form 29B?

Yes. A separate UDIN must be generated by the CA specifically for the Form 29B audit report. The UDIN for the Section 44AB tax audit report is different and does not cover Form 29B.

5. What if the company does not have a tax audit but is subject to MAT?

If a company’s turnover does not cross the Section 44AB threshold (₹1 crore for business, ₹10 crore with 95% digital threshold), a formal tax audit under Section 44AB is not required. However, Form 29B is still required for MAT compliance under Section 115JB. The two compliance requirements are independent of each other.

6. Can MAT credit be set off against dividend distribution tax (DDT)?

No. MAT credit can only be set off against normal income tax liability in future years. It cannot be applied against DDT (which was abolished from FY 2020-21 in any case), minimum surcharge, or any other tax.

7. How is MAT credit different from a regular tax credit?

Regular TDS credits (shown in Form 26AS) are credits for tax already collected by a deductor on your behalf and are applied directly against your tax payable for the year. MAT credit is a prospective credit: it arises when MAT exceeds normal tax, and it can only be used in a future year when normal tax exceeds MAT. It does not reduce your current year’s tax liability.

Key Takeaways

- MAT under Section 115JB ensures that companies pay tax on at least 15% of their book profit, even if their taxable income under normal provisions is significantly lower due to deductions and exemptions.

- Book profit is the net profit per the Companies Act Profit and Loss Account, adjusted by specific additions (income tax provisions, reserve transfers, provisions for contingencies, deferred tax, etc.) and deductions (exempt income, brought forward book losses, deferred tax credits, etc.) as prescribed under Section 115JB(2).

- Form 29B is the CA-certified audit report that formally computes and certifies book profit. It must be obtained and filed electronically before the company’s ITR-6 is submitted.

- Form 29B has three parts: Part A (universal), Part B (Ind AS-specific adjustments under Section 115JB(2A)), and Part C (convergence-year adjustments under Section 115JB(2C)).

- It applies to companies only. LLPs and other non-corporate entities subject to Alternate Minimum Tax (Section 115JC) file Form 29C instead.

- When MAT paid exceeds normal tax, the excess becomes MAT credit, which can be carried forward for 15 years and set off when normal tax subsequently exceeds MAT.

- A separate UDIN is mandatory for Form 29B; the tax audit UDIN does not suffice.

- Due date for FY 2025-26 (AY 2026-27): 31 October 2026. Non-filing attracts a penalty of up to ₹1,00,000 under Section 271BA.

Sources: Income Tax Department, Government of India: Form 29B FAQ; Taxguru: Form 29B and 29C: Audit Reports for Computing MAT and AMT under Income Tax Act; ClearTax: Form 29B of Income Tax Act; TaxConcept: Report of CA on Computing Book Profits, Form 29B.

This article is for general information only and does not constitute tax or professional advice. Consult a practising Chartered Accountant for guidance specific to your company’s situation.