Quick summary: Every time you deposit large amounts of cash in a bank, buy a property, invest heavily in mutual funds, or make big credit card payments, the institution involved is legally required to report that transaction to the Income Tax Department. The document used to make this report is called Form 61A, also known as the Statement of Financial Transactions (SFT). Form 61A is not filed by individual taxpayers. It is filed by banks, companies, registrars, mutual funds, and others. But every individual taxpayer needs to understand it, because the data from Form 61A feeds directly into their Annual Information Statement (AIS) and can trigger tax notices if their declared income does not match their high-value financial activity.

What Is Form 61A?

Form 61A is the prescribed format for the Statement of Financial Transactions (SFT), filed under Section 285BA of the Income Tax Act, 1961, read with Rule 114E of the Income Tax Rules, 1962.

It was introduced as part of a broader effort by the Income Tax Department to create a data trail around high-value transactions in the economy. The goal is simple: if you are spending or investing large amounts of money, and that money is not consistent with the income you have declared in your tax return, the department wants to know about it.

Before Form 61A, there was a similar concept called the Annual Information Return (AIR), introduced in 2004 under the same Section 285BA. The Finance Act, 2014 expanded the scope significantly and renamed it the Statement of Financial Transactions, effective April 1, 2015. Form 61A replaced the older AIR format and covers a broader range of transactions.

The key thing to understand: Form 61A is not filed by the person who makes the transaction. It is filed by the entity that records or facilitates it. So if you deposit ₹12 lakh in cash in your bank account, you do not file Form 61A. Your bank does. The transaction then appears in your AIS, and the Income Tax Department can cross-check it against your ITR.

The Bigger Picture: How Form 61A Connects to Your AIS

Every taxpayer registered on the Income Tax e-filing portal can view their Annual Information Statement (AIS) by logging in and navigating to the AIS section. The AIS shows a consolidated view of all financial transactions reported against your PAN by various entities during the year.

The data in your AIS comes primarily from two sources: TDS/TCS reported by deductors (which you can also see in Form 26AS), and SFT data reported by entities via Form 61A.

When you buy a property, your sub-registrar files Form 61A. When you invest ₹12 lakh in mutual funds, the fund house files Form 61A. When your company pays you dividends, the company files Form 61A. All of this appears in your AIS.

Before filing your ITR, you should review your AIS carefully. If a high-value transaction appears in your AIS but the corresponding income is missing from your ITR, the Income Tax Department’s automated systems will flag the discrepancy. This can result in a notice under Section 143(1)(a) or a scrutiny assessment under Section 143(2).

Who Must File Form 61A? The Reporting Entities

The obligation to file Form 61A falls on specific categories of entities, called reporting entities, as listed under Rule 114E. These include:

1. Banking companies and co-operative banks:

Banks report high-value cash deposits in savings and current accounts, time deposits (FDs and RDs), purchase of demand drafts and pay orders using cash, and foreign exchange transactions.

2. Post offices:

Post offices report cash deposits in post office savings accounts, time deposits, and recurring deposits above the threshold.

3. Nidhi companies:

Nidhi companies (mutual benefit finance companies) must report high-value deposits received from their members.

4. Companies issuing shares, debentures, or bonds:

Any company that receives ₹10 lakh or more from any single person during the year for acquiring its shares (including share application money), debentures, or bonds must report those investors in Form 61A.

5. Companies buying back their own shares:

When a company buys back shares and pays ₹10 lakh or more to any shareholder, it must report the transaction.

6. Mutual funds:

Mutual fund registrars or trustees must report investments where a person invests ₹10 lakh or more in units of a single mutual fund scheme during the year.

7. Sub-registrars and Inspector-Generals of Registration:

Property registration authorities must report the purchase of immovable property where the transaction value is ₹30 lakh or more.

8. Authorised dealers, money changers, and offshore banking units under FEMA:

These entities report foreign currency purchase and sale transactions above ₹10 lakh.

9. Credit card issuers:

Banks and NBFCs that issue credit cards must report: cash payments of ₹1 lakh or more against a credit card bill, and aggregate annual credit card payments of ₹10 lakh or more (by any mode).

10. Persons liable for audit under Section 44AB:

Businesses and professionals who are required to get a tax audit done must report cash receipts of ₹2 lakh or more from any single person in a single transaction for the sale of goods or services. This is the one category that may catch small and medium businesses by surprise.

If you run a business where cash sales above ₹2 lakh per transaction occur, and your turnover or receipts cross the Section 44AB audit threshold (₹1 crore for businesses, ₹10 crore with 95% digital transactions, or ₹50 lakh for professionals), you are a reporting entity under Rule 114E. For more on who falls under Section 44AB, see our guide on Form 3CA vs Form 3CB and the Form 3CD tax audit report explained.

11. Recognised stock exchanges:

Transactions in listed securities above ₹10 lakh per year are reported by the stock exchange or the clearing corporation.

12. Companies paying dividends:

Companies must report dividends paid to shareholders during the financial year, regardless of amount (no minimum threshold for this type), to facilitate pre-filling of ITR income fields. This falls under newer SFT types (SFT-015) introduced for pre-filling purposes.

13. Banks and financial institutions paying interest:

Banks, post offices, and similar institutions report interest credited or paid to depositors to enable pre-filling of interest income in the AIS (SFT-016). This is why your FD interest now appears automatically in your AIS. For what this means from the bank’s TDS perspective, see our guide on Form 16A explained.

What Transactions Must Be Reported? Thresholds at a Glance

The following table summarises the key specified financial transactions under Rule 114E and their reporting thresholds:

| SFT Type | Transaction | Reporting Entity | Threshold |

| SFT-001 | Cash deposits in savings accounts | Banks, co-op banks, post offices | ₹10 lakh aggregate in a year |

| SFT-002 | Cash deposits in time deposits (FDs, RDs) | Banks, co-op banks, post offices, Nidhi companies | ₹10 lakh aggregate in a year |

| SFT-003 | Cash payment of credit card bills | Banks, NBFCs (credit card issuers) | ₹1 lakh per bill payment in cash OR ₹10 lakh aggregate in the year |

| SFT-004 | Cash purchase of bank drafts, pay orders, prepaid instruments | Banks, co-op banks, post offices | ₹10 lakh aggregate in a year |

| SFT-005 | Receipt of share application money or purchase of shares | Company issuing shares | ₹10 lakh per person in a year |

| SFT-006 | Purchase of units of mutual funds | Mutual fund registrar or trustee | ₹10 lakh per person per scheme |

| SFT-007 | Foreign exchange purchase or sale | Banks, authorised dealers, money changers under FEMA | ₹10 lakh aggregate in a year |

| SFT-008 | Purchase or sale of immovable property | Sub-registrar, Inspector-General of Registration | ₹30 lakh or more per transaction |

| SFT-009 | Cash deposits or withdrawals in current accounts, overdraft accounts | Banks, co-op banks | ₹50 lakh aggregate in a year |

| SFT-010 | Credit card payments (by any mode, not just cash) | Banks, NBFCs (credit card issuers) | ₹10 lakh aggregate in a year |

| SFT-011 | Purchase of debentures or bonds | Company issuing debentures/bonds | ₹10 lakh per person in a year |

| SFT-012 | Cash receipts from sale of goods or services | Persons liable to audit under Section 44AB | ₹2 lakh per transaction |

| SFT-013 | Purchase and sale of listed securities | Stock exchanges, depositories, clearing corporations | ₹10 lakh per person per year |

| SFT-014 | Buyback of shares | Company buying back shares | ₹10 lakh per person in a year |

| SFT-015 | Dividend income paid to shareholders | Company | Reported per person (no fixed threshold for individual reports) |

| SFT-016 | Interest income paid or credited to depositors | Banks, post offices, NBFCs | Reported per person (for AIS pre-filling) |

Important note on aggregation: For most transaction types, the threshold is checked on the aggregate across all accounts of the same type held by the same person in the same institution during the financial year. For example, if you hold two savings accounts in the same bank and deposit ₹6 lakh in each, the aggregate ₹12 lakh crosses the ₹10 lakh threshold and the bank must report it.

A Practical Example: What Gets Reported and How It Affects You

Consider Ramesh, who works in a private company in Pune and earns ₹8 lakh per year in salary. During FY 2025-26:

- He deposits ₹11 lakh cash in his savings account (received from renting out a property)

- He buys a flat worth ₹45 lakh and pays ₹5 lakh in cash for registration

- He invests ₹12 lakh in a mutual fund scheme

What gets reported in Form 61A?

- His bank reports the ₹11 lakh cash deposit (SFT-001: crosses ₹10 lakh threshold)

- The sub-registrar reports the ₹45 lakh property purchase (SFT-008: crosses ₹30 lakh threshold)

- The mutual fund registrar reports the ₹12 lakh investment (SFT-006: crosses ₹10 lakh threshold)

All three appear in Ramesh’s AIS when he logs into the IT portal. His declared income is ₹8 lakh in salary. The Income Tax Department’s system now sees ₹11 lakh in cash deposits, a ₹45 lakh property purchase, and ₹12 lakh in mutual fund investments reported against his PAN. If Ramesh does not explain the source of the ₹11 lakh cash (rental income) and declare it in his ITR, he is likely to receive a notice asking him to reconcile his income with his financial activity.

This is how Form 61A, which Ramesh never filed himself, directly affects him.

How to File Form 61A: The Process for Reporting Entities

The filing process is technical and handled entirely online. Reporting entities must:

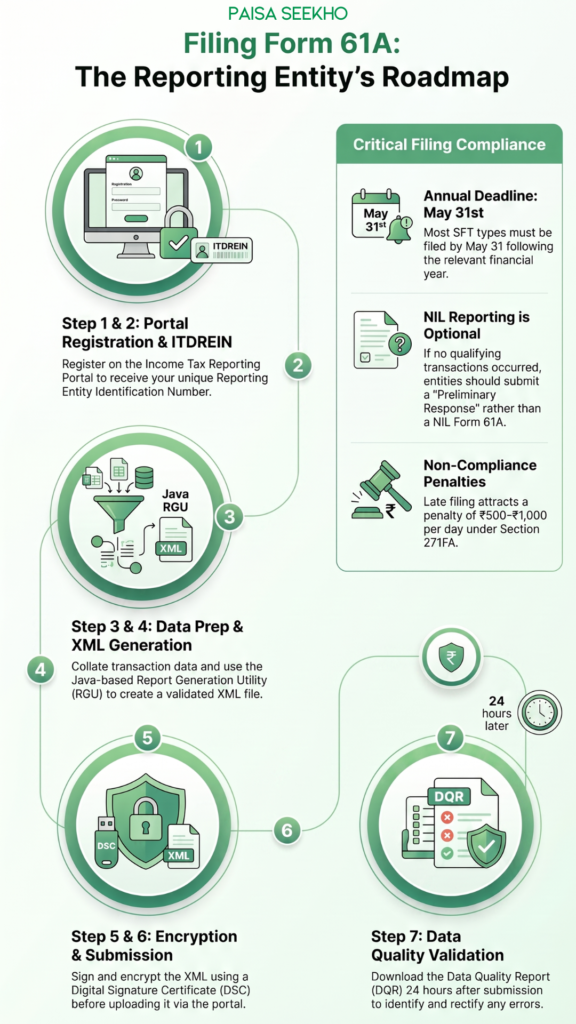

Step 1: Register on the Reporting Portal.

Log into the Income Tax e-filing portal (incometax.gov.in) and navigate to Pending Actions → Reporting Portal. Select “New Registration” and complete the entity registration process. During registration, provide the details of the Designated Director (the person responsible for overseeing Section 285BA compliance) and the Principal Officer (the person who submits the SFT). Contact details (email and mobile) must be accurate for all communications.

Step 2: Obtain ITDREIN.

Once registered, the entity receives an Income Tax Department Reporting Entity Identification Number (ITDREIN). This is a unique ID used for all Form 61A filings by that entity. Note that once assigned, ITDREIN cannot be deactivated.

Step 3: Prepare the SFT data.

Collate all specified financial transactions for the year, organised by the applicable SFT type. This involves matching customer or investor PAN details, transaction amounts, dates, and other required fields.

Step 4: Generate the XML file.

Download the Report Generation Utility (RGU) from the reporting portal. This is a Java-based desktop utility. Fill in the transaction data in the utility, run the built-in validation to check for errors, and then click “Generate XML.” Save the file with a “.xml” extension.

Step 5: Sign and encrypt using DSC.

Use the Generic Submission Utility to sign and encrypt the XML file using the entity’s Digital Signature Certificate (DSC) of the Designated Director or Principal Officer.

Step 6: Upload to the Reporting Portal.

Log back into the reporting portal using the entity’s credentials and the ITDREIN. Upload the signed and encrypted file. On successful submission, an acknowledgement number is generated.

Step 7: Check the Data Quality Report (DQR).

Wait at least 24 hours after uploading before downloading the DQR, which validates the data quality of the submission. Any errors flagged must be corrected and resubmitted.

Due Dates for Form 61A

| Transaction Type | Filing Frequency | Due Date |

| Most SFT types (cash deposits, property, shares, debentures, foreign exchange, credit card, etc.) | Annual | 31 May following the financial year |

| Transactions in listed securities (SFT-013) and units of mutual funds (SFT-006) | Half-yearly | 31 October (for April to September) and 31 May (for October to March) |

For FY 2025-26:

- Annual SFT filings (all types except listed securities and mutual funds): due by 31 May 2026

- Half-yearly SFT for H2 (October 2025 to March 2026): also due by 31 May 2026

The Income Tax Department’s Reporting Portal usually displays a reminder as the deadline approaches. For FY 2025-26, the portal has already notified entities to file early to avoid last-minute technical issues from high server traffic near the deadline.

Do You Need to File a NIL Form 61A?

This is a commonly asked question. The Income Tax Department’s Reporting Portal has officially clarified: “There is no requirement to file ‘NIL’ report in Form 61A for any SFT.”

If a reporting entity (such as a bank, company, or Section 44AB assessee) had no specified financial transactions crossing the applicable thresholds during the year, it is not required to file Form 61A at all. The entity can instead submit an SFT Preliminary Response on the portal indicating “Not Applicable.”

However, this is different from Form 61B (for Prescribed Reporting Financial Institutions under the Common Reporting Standard): for Form 61B, NIL filing is mandatory for all qualifying institutions even if there are no reportable accounts.

Correction Statement: What to Do If Errors Are Found

If a reporting entity discovers an error in a submitted Form 61A (wrong PAN, wrong amount, missing transactions), they can file a Correction Statement to the original submission. The correction statement must reference the original statement’s acknowledgement number and clearly indicate what is being corrected.

Entities have 30 days to rectify a defective filing after receiving a notice from the Income Tax Department about the defect.

Penalties for Non-Compliance

| Default | Penalty |

| Failure to file Form 61A by the due date | ₹500 per day under Section 271FA |

| Continued failure after notice under Section 285BA(5) | ₹1,000 per day from expiry of the notice period |

| Filing with inaccurate information, discovered but not rectified | ₹50,000 flat penalty under Section 271FAA |

The Section 271FAA penalty of ₹50,000 applies specifically when the reporting entity knows or discovers the inaccuracy but fails to inform the tax authorities within 10 days, or fails to follow due diligence procedures in verifying information.

The Income Tax Department can also issue notices to persons who are required to file but have not done so, directing them to file within 30 days. Continued default after such a notice escalates the per-day penalty from ₹500 to ₹1,000.

Form 61A vs Form 61B: What Is the Difference?

| Form 61A | Form 61B | |

| What it covers | Specified Financial Transactions (SFTs) under Section 285BA | Reportable Accounts under the Common Reporting Standard (CRS) and FATCA |

| Who files | Banks, companies, mutual funds, registrars, Section 44AB assessees, and others under Rule 114E | Prescribed Reporting Financial Institutions (RFIs) participating in international information exchange |

| Purpose | Domestic tax compliance: tracking high-value transactions by Indian residents | International tax compliance: identifying foreign account holders and reporting to foreign tax authorities |

| NIL filing required? | No | Yes: even if no reportable accounts exist |

| Due date | 31 May (annual); 31 October and 31 May (half-yearly) | 31 May for each calendar year |

Most businesses and institutions readers of PaisaSeekho will be concerned with Form 61A, not Form 61B.

What Individual Taxpayers Should Know

If you are an individual taxpayer (not a bank or company), you never file Form 61A yourself. But here is what you should do because of it:

Check your AIS before filing your ITR.

Log into the Income Tax portal, go to the AIS section, and download your AIS for the relevant financial year. It will show all Form 61A entries reported against your PAN. Reconcile each entry with what you are reporting in your ITR.

Report all income corresponding to high-value transactions.

If your AIS shows a ₹15 lakh FD deposit, make sure the interest from that FD is in your ITR. If it shows a ₹45 lakh property purchase, check that the source of funds is explainable from your declared income. For understanding how FD interest is handled from a TDS perspective, see our guide on Form 15G vs Form 15H which explains when TDS is deducted on FD interest and how to prevent it.

Respond to AIS entries you disagree with.

If an entry in your AIS is incorrect (for example, a transaction is attributed to your PAN by mistake), you can submit feedback on the IT portal. Mark the entry as “incorrect” or “duplicate” and provide the correct information. This triggers a review by the department.

For Section 44AB assessees:

If you are a business or professional subject to tax audit, remember that your own obligation to report cash sales above ₹2 lakh per transaction (SFT-012) means you are yourself a reporting entity. This responsibility exists alongside, and is separate from, the tax audit itself. For the intersection with tax audit compliance, refer to our Form 3CD guide.

Form 61A and the New Income Tax Act, 2025

Under India’s Income Tax Act, 2025 (effective from 1 April 2026), the SFT framework under Section 285BA of the old Act is being carried forward into the new Act under revised section references. The obligation to report specified financial transactions in the prescribed format (Form 61A for the current financial year) continues.

The data captured via Form 61A continues to feed into the AIS of individual and corporate taxpayers under the new framework, and the department’s cross-matching of SFT data with ITR income declarations remains a central pillar of compliance enforcement.

For FY 2025-26 (transactions between April 2025 and March 2026): Form 61A continues to be the applicable form, with a due date of 31 May 2026 for most transaction types.

Frequently Asked Questions

1. Do I as an individual taxpayer need to file Form 61A?

Only if you are a person covered under Section 44AB (i.e., your business or professional income triggers a tax audit) and you have received cash payments of ₹2 lakh or more per transaction from any customer. For most individual salaried taxpayers and small investors, Form 61A is not your obligation to file. It is filed by banks, companies, and registrars about your transactions.

2. How do I know if a transaction has been reported against my PAN in Form 61A?

Log into the Income Tax e-filing portal (incometax.gov.in) and check your Annual Information Statement (AIS). All SFT data filed by reporting entities against your PAN appears in the AIS.

3. My bank reported a cash deposit in my AIS through Form 61A. Is that a problem?

Not automatically. If the deposit corresponds to income you have already declared in your ITR (for example, rental income, agricultural income, or a gift from relatives), you need to ensure the ITR reflects that income. If the deposit is not explained by your declared income, the department may seek clarification.

4. What if two different entities report the same transaction against my PAN?

This can happen, for example, when both a bank and a sub-registrar report aspects of the same property purchase. Review your AIS carefully and, if an entry seems duplicated or incorrect, submit feedback on the portal.

5. I am a CA running a firm with gross receipts above ₹50 lakh. Am I a reporting entity?

Yes. Professionals with gross receipts above ₹50 lakh fall under Section 44AB and are reporting entities under Rule 114E. If you receive cash of ₹2 lakh or more in a single transaction from any client, you must report that transaction in Form 61A (SFT-012).

6. My mutual fund statements show various SIP investments. Will all of these be reported?

Only if the aggregate investment in a single mutual fund scheme by you crosses ₹10 lakh in the financial year. Individual SIP instalments of ₹5,000 per month add up to ₹60,000 in a year, which is well below the threshold. However, if you make a lump sum of ₹10 lakh or more in one scheme, that will be reported.

7. What is ITDREIN and do I need one?

ITDREIN (Income Tax Department Reporting Entity Identification Number) is required only by entities that file Form 61A. Individual taxpayers do not need an ITDREIN.

8. Can the same person be both a reporting entity and a regular taxpayer?

Yes. A partnership firm or individual business subject to Section 44AB is simultaneously a regular income taxpayer (filing ITR-3 or ITR-4) and a reporting entity (filing Form 61A if they have qualifying cash transactions). Both obligations must be met independently.

Key Takeaways

- Form 61A is the Statement of Financial Transactions (SFT), filed under Section 285BA of the Income Tax Act read with Rule 114E, by reporting entities (banks, companies, registrars, mutual funds, and Section 44AB assessees) to report high-value transactions to the Income Tax Department.

- It is not filed by individual taxpayers making the transactions. It is filed by the institution that records or facilitates the transaction.

- Reported data feeds directly into the taxpayer’s Annual Information Statement (AIS), which the department uses to cross-check declared income against actual financial activity.

- Key thresholds: ₹10 lakh for most bank/investment transactions, ₹30 lakh for property purchases, ₹50 lakh for current account cash deposits, ₹2 lakh per transaction for cash receipts by Section 44AB businesses.

- Annual filing due date: 31 May following the financial year. Half-yearly for mutual funds and listed securities: 31 October and 31 May.

- No NIL filing is required for Form 61A if a reporting entity had no qualifying transactions.

- Penalties: ₹500/day for late filing, escalating to ₹1,000/day after notice; ₹50,000 for inaccurate reporting.

- Individual taxpayers must review their AIS before filing their ITR and ensure all high-value transactions appearing there are reconciled with their declared income.

Sources: Income Tax Department, Government of India: Statement of Financial Transaction (SFT); Income Tax Department Reporting Portal (Project Insight); ClearTax: Form 61A; Taxguru: SFT Form 61A on Share Issues for FY 2025-26.

This article is for general information only and does not constitute tax or legal advice. For guidance specific to your reporting obligations, consult a practising Chartered Accountant or tax professional.