Quick summary: When a business or professional is required to get a tax audit done under Section 44AB of the Income Tax Act, the Chartered Accountant submits an audit report in either Form 3CA or Form 3CB. Attached to both is a detailed statement called Form 3CD. This is the actual working document of the tax audit: 44 clauses that together capture your business’s income, expenses, TDS compliance, depreciation, deductions, cash transactions, GST breakup, and much more. The Income Tax Department uses Form 3CD as a risk-assessment tool to decide which taxpayers to scrutinise further. This guide explains what Form 3CD is, what each section covers, the most important clauses to get right, and what is changing for AY 2026-27.

What Is Form 3CD?

Form 3CD is a statement of particulars prescribed under Rule 6G(2) of the Income Tax Rules, 1962. It is a mandatory annexure to both Form 3CA and Form 3CB. Whether a company uses Form 3CA or a sole proprietor uses Form 3CB, both must attach a completed Form 3CD. There is no separate Form 3CD for companies versus firms; the form is the same for everyone.

In plain terms, Form 3CD is a standardised checklist of financial and compliance information that the CA must certify about the taxpayer’s accounts. It runs to 44 numbered clauses (some with multiple sub-clauses), covering everything from basic business details and accounting methods to TDS defaults, cash transaction limits, related-party payments, GST breakup, and Chapter VI-A deductions.

The Income Tax Department uses the data in Form 3CD to:

- Cross-check income reported in the ITR against what is disclosed in the audit report

- Identify TDS defaults that trigger automatic disallowances

- Flag mismatches between turnover in Form 3CD and GST returns

- Spot patterns that indicate under-reporting of income or over-claiming of deductions

- Select cases for detailed scrutiny assessment

In short: a Form 3CD filled carefully and accurately protects you. A poorly filled one invites problems.

Who Prepares and Files Form 3CD?

Form 3CD is prepared jointly by the taxpayer (or their finance team) and the Chartered Accountant conducting the audit:

- The taxpayer’s management provides the underlying data, figures, and answers to each clause

- The CA verifies the data against the books of accounts, applies professional judgment, and certifies the correctness of the particulars

- The CA then files the completed Form 3CD electronically on the income tax e-filing portal (incometax.gov.in) using the offline utility and their Digital Signature Certificate (DSC)

- The taxpayer must then log into their own e-filing account and formally accept the submitted audit report. An unaccepted report is treated as not filed.

Before signing the report, the CA must generate a Unique Document Identification Number (UDIN) on the ICAI portal (udin.icai.org). A Form 3CD without a valid UDIN is not considered properly filed for AY 2026-27. The UDIN must be generated on or before the date of signing.

Structure of Form 3CD: Part A and Part B

Form 3CD is divided into two parts:

Part A (Clauses 1 to 8): Basic identification and background details. Part B (Clauses 9 to 44): The substantive disclosures covering income, expenses, compliance, and special items.

The portal requires Part A to be filled and saved before Part B can be accessed.

Part A: Clauses 1 to 8 (Basic Details)

These clauses capture the foundational facts about the assessee and the audit:

| Clause | What It Asks |

| 1 | Name of the assessee |

| 2 | Address of the assessee |

| 3 | Permanent Account Number (PAN) |

| 4 | Whether the assessee is liable to pay indirect tax: GST, excise duty, customs duty, etc. If yes, the registration or GST number |

| 5 | Status of the assessee: individual, HUF, firm, company, co-operative society, AOP, BOI, or other |

| 6 | Previous year: the financial year being audited (for FY 2025-26: 01.04.2025 to 31.03.2026) |

| 7 | Assessment year (for FY 2025-26: AY 2026-27) |

| 8 | Indicate which clause of Section 44AB applies: (a) business turnover exceeds ₹1 crore; (b) professional gross receipts exceed ₹50 lakh; (c) presumptive taxpayer declaring income below prescribed rate |

These are factual disclosures. Errors here (wrong PAN, wrong AY, wrong clause) can create technical defects in the audit report.

Part B: Clauses 9 to 44 (The Substantive Disclosures)

This is the heart of Form 3CD. Here is a clause-by-clause walkthrough of what each covers:

Business Profile and Accounting (Clauses 9 to 14)

- Clause 9: Nature of business or profession carried on during the year. If multiple businesses are carried on, each must be mentioned. Any change in the nature of business during the year must also be reported.

- Clause 10: Details of books of accounts maintained. Whether accounts are maintained on a computer system or manually. The complete address where books are kept, including all branches. Whether books are maintained per Section 44AA requirements.

- Clause 11: Whether books of accounts examined by the CA are in agreement with the Balance Sheet and Profit and Loss Account; any discrepancies or deficiencies found.

- Clause 12: Whether the Profit and Loss Account includes income or expenditure pertaining to any earlier year; details of such items if any.

- Clause 13: Method of accounting followed: cash basis or mercantile (accrual) basis. Whether there was any change in the method during the year. If yes, the financial effect of the change.

- Clause 14: Method of valuation of closing stock: cost price, net realizable value, or another method. Whether there was any change in the valuation method. Effect of the change if applicable.

Capital Assets and Special Transactions (Clauses 15 to 16)

- Clause 15: Whether any capital asset was converted into stock-in-trade during the year. If yes, the date of conversion, cost of the asset, and the amount at which it was converted.

- Clause 16: Amounts not credited to the Profit and Loss Account during the year: capital receipts claimed as exempt, items covered under Section 45 (capital gains), and income charged at special rates like 115BB.

Expenses and Depreciation (Clauses 17 to 20)

- Clause 17: Where standing charges have been debited on personal account or capital account rather than revenue account. This identifies expenses incorrectly classified.

- Clause 18: Depreciation details. This is one of the most detailed clauses in Form 3CD. For each block of assets, the CA must disclose: description of asset, rate of depreciation as per the Income Tax Act, opening WDV (Written Down Value), additions and deletions during the year, asset-wise WDV, depreciation as per books, and depreciation as per Income Tax Act. Any differences between the two are reconciliation items.

- Clause 19: Deductions under Section 32AC (investment in new plant and machinery) and Section 32AD (investment in specified states). Note: As per CBDT’s Eighth Amendment Rules, 2025 (effective from AY 2025-26), several expired sections including 32AC and 32AD have been removed from Form 3CD since their benefit periods have lapsed. Clause 19 now applies mainly to any current eligible deductions under remaining capital investment incentive provisions.

- Clause 20: Amounts admissible under Sections 35AD, 35CCC, and 35CCD relating to deduction for capital expenditure in specified businesses, agricultural extension projects, and skill development projects.

Related Parties and Disallowances (Clauses 21 to 25)

- Clause 21: Amounts paid to relatives or to a business in which the proprietor/partner/director has substantial interest, where the payment is excessive or unreasonable per Section 40A(2)(b). The CA must identify and quantify amounts that are not at arm’s length.

- Clause 22: Amounts inadmissible under Section 40(a). This clause covers the most important disallowance provisions:

- Payments to non-residents without deducting TDS

- Payments where TDS was deducted but not deposited by the due date for filing the return

- Fringe Benefit Tax, income tax, and other taxes paid (not deductible as expense)

- Payments to non-resident sportsmen or sports associations

- Clause 23: Amounts inadmissible under Section 40A(2): payments to related parties (directors, relatives, partner-controlled entities) that exceed what would be paid to an unrelated party for similar services or goods. Also covers Section 40A(3): cash payments above ₹10,000 for business expenses (disallowed if not made through account payee cheque, bank draft, NEFT, RTGS, or similar).

- Clause 24: Amounts paid to Micro and Small Enterprises (MSMEs) beyond the statutory due date under the MSMED Act. From AY 2024-25, Section 43B(h) disallows MSME payments made after the due date unless paid before the ITR filing date. The CA must identify and disclose all such delayed MSME payments.

- Clause 25: Provision for income tax and current tax that has been debited to the Profit and Loss Account, which is not deductible as a business expense.

Section 43B Items: Payment-Basis Deductions (Clause 26)

This is one of the most scrutinised clauses. Section 43B requires certain payments to be actually made (not just accrued) to qualify for deduction. The CA must report:

- Employer contribution to PF, ESI, superannuation, gratuity, and similar funds: deductible only if paid before the due date for filing the return

- Bonus and commission to employees: deductible only when actually paid

- Interest on borrowings from public financial institutions or banks: deductible on actual payment basis

- GST, customs duty, excise, and other indirect taxes: deductible when actually paid

- MSME payments (under the new Section 43B(h))

For each item, the CA reports whether it was paid within the due date and the amount, if any, that qualifies for deduction versus what is to be disallowed.

Prior Period and Miscellaneous Items (Clauses 27 to 30C)

- Clause 27: CENVAT credit (old indirect tax credit, now largely replaced by ITC under GST) availed or utilised; prior period income or expenditure credited or debited in the current year’s accounts.

- Clause 28: Whether the assessee received shares of a closely held company without consideration or for inadequate consideration per Section 56(2)(viia): details of the shares, their fair market value, and the amount treated as income.

- Clause 29 and 29A/29B: Whether any amount is to be included as income from other sources under Sections 56(2)(vii), 56(2)(ix), and 56(2)(x): gifts, property received without consideration, and other deemed income provisions. Details of the property and amounts.

- Clause 30: Loans or deposits taken or repaid above ₹20,000 (under Section 269SS and 269T) otherwise than by account payee cheque or banking channel. Cash loans are illegal above this limit, and any such transactions must be disclosed.

- Clauses 30A, 30B, 30C: Transfer pricing adjustments under Section 92CE (primary adjustment), secondary adjustments under Section 92CE(1), and limitation of interest deductions under thin capitalisation rules (Section 94B). These are relevant primarily for companies with international related-party transactions.

Loans, Deposits, and TDS Compliance (Clauses 31 to 34)

- Clause 31: Details of repayment or acceptance of loans or deposits in cash exceeding ₹20,000 during the year. Disclosures here directly relate to Sections 269SS and 269T.

- Clause 32: Deductions claimed under Chapter VI-A. The CA reports each Section (80G donations, 80-IA, 80-IB, 80-IC, 80-IE, etc.) and certifies the amount and whether eligibility conditions are met.

- Clause 33: Deduction under Section 10AA for units in Special Economic Zones.

- Clause 34: TDS and TCS Compliance. This is one of the most important and most scrutinised clauses in the entire Form 3CD. It has three parts:

- Clause 34(a): Whether TDS was deducted wherever required. Lists each section under which tax should have been deducted (salary: Section 192; interest to residents: Section 194A; contractor payments: Section 194C; professional fees: Section 194J; rent: Section 194I; and all other applicable sections). For each, the CA reports the total amount paid, TDS deducted, TDS deposited, and whether any deduction was short or delayed.

- Clause 34(b): TDS details for payments to non-residents under Sections 192, 194E, 195, 196B, 196C, 196D, and similar.

- Clause 34(c): Whether TCS (Tax Collected at Source) under Chapter XVII-BB was collected and deposited correctly.

Any TDS default identified in Clause 34 automatically signals an expense disallowance under Section 40(a)(ia): 30% of the amount on which TDS was not deducted or not deposited on time is disallowed as a deduction. This is why TDS compliance before the audit is critical.

Miscellaneous Financial Disclosures (Clauses 35 to 44)

- Clause 35: Quantitative details. For businesses dealing in goods (manufacturing and trading), the CA must report opening stock, purchases, sales, closing stock, and shortage/excess. This clause allows the assessing officer to check whether the GP ratio is consistent with industry norms and whether there are unexplained inventory variations.

- Clause 36: Whether the tax audit report contains any opinion expressed or observation made in the report of the audit conducted for an earlier year under Section 44AB; details of qualifications.

- Clause 36A: Whether any amount is assessable as deemed dividend under Section 2(22)(e) based on loans or advances given by a closely held company to a substantial shareholder or a concern in which such shareholder has substantial interest.

- Clause 36B: Share buyback disclosures under Section 46A. Following the taxation changes to share buybacks in Budget 2024, this clause requires details of any buyback of shares during the year and the amounts involved. Introduced or expanded for AY 2024-25 and continuing for AY 2026-27.

- Clauses 37 to 39: Whether a cost audit, Central Excise audit, or service tax audit was conducted during the year; and if so, any disqualifications or disagreements found in those audits.

- Clause 40: Accounting ratios for the current and previous year. These include Gross Profit to Turnover ratio, Net Profit to Turnover ratio, Stock-in-Trade to Turnover ratio, and Material Consumed to Finished Goods Produced ratio (for manufacturers). This clause lets the Income Tax Department compare your profitability ratios against industry benchmarks and flag unusual variations.

- Clause 41: Details of demand or refunds under indirect tax laws (GST, customs, excise) that are pending or received during the year.

- Clause 42: Information about any accounting unit or segment of the business, if separate accounts are maintained.

- Clause 43: Details of payments made outside India where Form 15CA (remittance declaration) was required to be furnished under Section 195. Lists the name of the payee, country of residence, amount remitted, and whether Form 15CA was actually filed.

- Clause 44: GST Breakup of Expenditure. Introduced in 2021 and continuing in full force for AY 2026-27, this is one of the most data-intensive clauses for many businesses. The CA must break down the total expenditure for the year into:

- Amount relating to goods or services registered under GST (with applicable IGST/CGST/SGST separately)

- Amount relating to goods or services from unregistered suppliers

- Amount relating to GST-exempt supplies

- Amount relating to imports

This clause forces a direct reconciliation between the Income Tax balance sheet/P&L and the GST return data. Mismatches between turnover and expenses in Form 3CD versus what is reported in GSTR-1 and GSTR-3B are now a primary trigger for automated scrutiny notices, since the Income Tax Department’s systems cross-match these databases.

The Most Critical Clauses: Where Most Issues Arise

If you had to focus on just a few clauses to get right, these are the ones that matter most for compliance risk:

- Clause 34 (TDS compliance): Any default disclosed here directly results in an expense disallowance and can trigger a Section 201 order. Ensure all TDS is deducted and deposited before the audit.

- Clause 26 (Section 43B payments): Make sure all statutory dues like PF, ESI, GST, and professional tax are paid before the ITR filing due date. Unpaid dues as of that date are disallowed.

- Clause 24 (MSME payments): Section 43B(h) is new and many businesses are still unaware of it. Any payment to a Micro or Small Enterprise that is overdue per the MSMED Act’s payment timeline must be reported and will be disallowed.

- Clause 44 (GST breakup): Reconcile your Income Tax books with your GST returns before the audit begins. The IT Department’s AIS already cross-references GST and income tax data.

- Clause 40 (accounting ratios): If your GP ratio has dropped sharply compared to the prior year or to industry norms, the CA must report it and you should be prepared to explain it if the department asks.

What Is UDIN and Why Does It Matter for Form 3CD?

A UDIN (Unique Document Identification Number) is a number generated by the CA on the ICAI’s UDIN portal (udin.icai.org) for every document they certify or sign. For Form 3CD, the CA must generate a UDIN specifically for the tax audit report under Section 44AB and include it in the report before submission.

UDIN serves as a verification mechanism: any stakeholder (including the Income Tax Department) can verify that the CA actually signed the report and that it has not been tampered with. Tax audit reports submitted without a valid UDIN may be rejected or treated as defective.

For AY 2026-27, UDIN generation is mandatory for all Forms 3CA-3CD and 3CB-3CD.

Due Dates for AY 2026-27 (FY 2025-26)

| Compliance | Due Date |

| Tax audit report (Form 3CA/3CB with Form 3CD) | 30 September 2026 |

| Tax audit report for cases with international transactions (Form 3CEB also required) | 31 October 2026 |

| Income Tax Return filing for audited taxpayers | 31 October 2026 |

The CA must submit the audit report on or before the due date. The taxpayer must accept it through their e-filing portal account before the ITR is filed. The ITR cannot be filed without the accepted audit report.

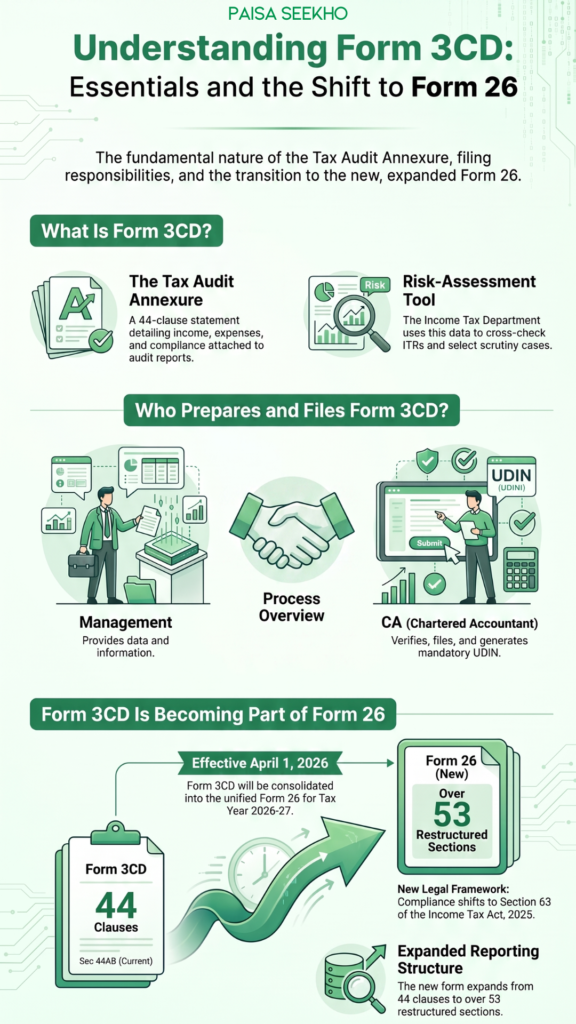

Form 3CD Is Becoming Part of Form 26

For AY 2026-27 (FY 2025-26), Form 3CD continues to apply exactly as described in this article. However, under the Income Tax Act, 2025 (effective from 1 April 2026), Forms 3CA, 3CB, and 3CD are being consolidated into a new unified form called Form No. 26 under Rule 47 of the Income Tax Rules, 2026.

According to the Income Tax Department’s official FAQ on Form 26:

- Form 26 is applicable for Tax Years commencing on or after 1 April 2026 (i.e., from Tax Year 2026-27 onwards)

- The underlying obligation shifts from Section 44AB (old Act) to Section 63 of the Income Tax Act, 2025

- The thresholds remain the same: ₹1 crore for business (₹10 crore with 95% digital transactions), ₹50 lakh for professionals

- Form 26 has an expanded clause structure with 53 or more clauses (compared to 44 in Form 3CD), with restructured sections and updated reporting requirements

- Depreciation disclosure in Form 26 now explicitly segregates assets held for less than 180 days versus 180 days or more

- Quantitative details (inventory reporting) will only be required for trading and manufacturing concerns, not all businesses

- Clause 43 (international remittances) in the new form is integrated more tightly with international taxation reporting

For FY 2025-26 (AY 2026-27): continue using Forms 3CA/3CB and Form 3CD. Our earlier guide on Form 3CA vs Form 3CB covers which audit form applies to your type of entity. The transition to Form 26 only takes effect for income earned from April 2026 onwards.

Common Mistakes to Avoid

Not reconciling Form 3CD turnover with GST returns.

Clause 44 data and your GSTR-1/GSTR-3B data are now cross-matched automatically. A mismatch even of ₹10,000 can trigger a notice.

Missing MSME payment disclosures in Clause 24.

Section 43B(h) is still relatively new, and many businesses and CAs miss MSME-related disallowances. Check all your vendors: if any are registered MSMEs and you paid them beyond the statutory period under the MSMED Act, the amount is disallowable.

Submitting without UDIN.

The UDIN must be generated before the CA signs the report, not after. A report signed without a UDIN is treated as defective.

Taxpayer not accepting the report on time.

After the CA files, the taxpayer has a separate step: they must log in to the e-filing portal and accept the report. If this is not done before the due date, the audit is treated as not filed.

Using the wrong method of accounting disclosure.

If your business uses mercantile basis but the CA accidentally ticks “cash basis” in Clause 13, it creates a factual inaccuracy that can be flagged during scrutiny.

Frequently Asked Questions

1. Is Form 3CD the same as the audit report?

Not exactly. The audit report is either Form 3CA or Form 3CB. Form 3CD is the detailed statement of particulars attached to either of those. Together (3CA + 3CD or 3CB + 3CD) they constitute the complete tax audit submission.

2. Who fills in the data for Form 3CD?

The taxpayer’s management (or their finance team) provides the underlying data and answers to each clause. The CA verifies the data against the books of accounts and certifies its correctness. Both parties are responsible for accuracy.

3. What happens if there are errors in Form 3CD?

A revised Form 3CD can be filed to correct mistakes. However, the revised form must also be filed and accepted on time. Any inaccuracy that leads to understating income or overstating deductions can attract penalty proceedings.

4. Is Form 3CD filed every year?

Form 3CD is filed for each year that a tax audit is required. If your turnover drops below the threshold in a subsequent year and no audit is required, Form 3CD is not filed for that year.

5. How many copies of Form 3CD exist?

There is only one Form 3CD, filed electronically. There is no separate physical Form 3CD to submit to any authority; the e-filing portal submission is the official version.

6. My CA says Form 3CD takes two to three months to prepare. Is that normal?

Yes, for businesses with complex transactions, multiple branches, or high transaction volumes, Form 3CD preparation is time-consuming. Clauses 34 (TDS), 44 (GST breakup), 26 (Section 43B), and 35 (quantitative details) in particular require detailed reconciliation work. Starting the process in June rather than September is strongly advisable.

7. What is the difference between Form 3CD and Form 3CE?

Form 3CE is a separate audit report for non-residents and foreign companies receiving income in India as royalty or fees for technical services under Section 44DA. It is not the same as Form 3CD and is filed in different circumstances.

Key Takeaways

- Form 3CD is the 44-clause statement of particulars filed alongside either Form 3CA or Form 3CB as part of the tax audit report under Section 44AB of the Income Tax Act.

- It is divided into Part A (Clauses 1 to 8): basic identification details, and Part B (Clauses 9 to 44): substantive financial and compliance disclosures.

- The most scrutinised clauses are Clause 34 (TDS/TCS compliance), Clause 26 (Section 43B payments), Clause 24 (MSME delayed payments), Clause 44 (GST breakup), and Clause 40 (accounting ratios).

- The CA must generate a valid UDIN before signing the report. The taxpayer must accept the report on the e-filing portal after the CA files it.

- The tax audit report for FY 2025-26 (AY 2026-27) is due by 30 September 2026. The ITR for audited taxpayers is due by 31 October 2026.

- From Tax Year 2026-27 (income from April 2026 onwards), Form 3CD is replaced by the expanded Form No. 26 under the Income Tax Act, 2025 and Income Tax Rules, 2026. For FY 2025-26, Form 3CD continues to apply unchanged.

Sources: Income Tax Department, Government of India: Form 3CA-3CD User Manual; Income Tax Department: Items Reportable in the Tax Audit Report; Income Tax Department: Form No. 26 FAQ; CBDT Eighth Amendment Rules, 2025 on amendments to Form 3CD, as reported by ClearTax.

This article is for general information only and does not constitute tax or professional advice. Consult a practising Chartered Accountant for guidance specific to your situation.