Quick summary: When an Indian entity sends money above ₹5 lakh to a non-resident and the payment is taxable in India, the bank requires not just the remitter’s self-declaration (Form 15CA Part C) but also an independent certificate from a Chartered Accountant confirming that the tax analysis is correct. That certificate is Form 15CB. Before issuing it, the CA examines the underlying contract, the DTAA between India and the payee’s country, the nature of the income, and the applicable TDS rate. This guide explains what Form 15CB contains, what the CA reviews before issuing it, the role of the Tax Residency Certificate and Form 10F, how DTAA rates are applied, and walks through worked examples for different types of foreign payments.

What Is Form 15CB?

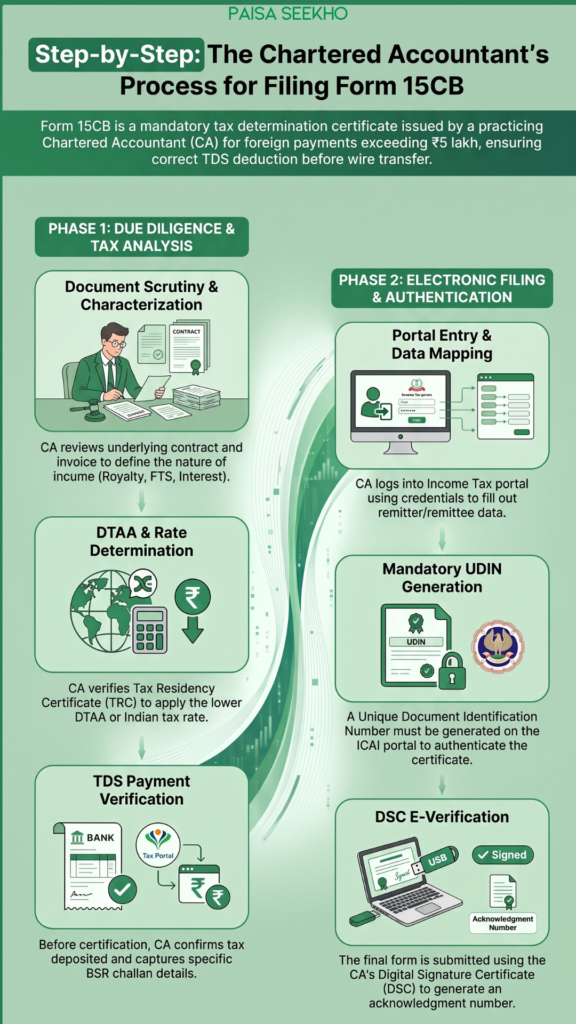

Form 15CB is a tax determination certificate issued by a practising Chartered Accountant (CA) under Section 195(6) of the Income Tax Act, 1961. It is filed electronically on the Income Tax e-filing portal using the CA’s Digital Signature Certificate (DSC) before the remitter files Form 15CA Part C.

The certificate answers one core question: Is this remittance taxable in India, and if so, has the correct tax been deducted?

To answer this, the CA examines the nature of the payment, the country of the recipient, whether a DTAA applies, what the correct TDS rate is, and whether all supporting documents (like a Tax Residency Certificate) are in order. The CA then certifies these findings in Form 15CB, takes professional responsibility for the certificate, and generates a UDIN (Unique Document Identification Number) to authenticate it.

Without a valid Form 15CB, the remitter cannot file Form 15CA Part C, and without Part C, the bank will not process the foreign wire transfer.

Before reading further, note that Form 15CB and Form 15CA work together as a pair. Our previous article on Form 15CA for foreign remittances explains the remitter’s side of this compliance. This article focuses specifically on the CA’s certificate.

When Is Form 15CB Required?

Form 15CB is required when all three of the following conditions are met:

- The remittance is being made to a non-resident individual or foreign company

- The payment is chargeable to tax in India under the Income Tax Act or DTAA

- The aggregate remittances to that non-resident during the financial year exceed ₹5 lakh

When Form 15CB is NOT required:

- When the aggregate remittance to that non-resident during the year is ₹5 lakh or less: only Form 15CA Part A is filed

- When the remitter has obtained an order or certificate from the Assessing Officer (AO) under Section 195(2), 195(3), or Section 197: Form 15CA Part B is filed without Form 15CB

- When the remittance is not chargeable to tax: Form 15CA Part D is filed

- When the remittance falls under the Rule 37BB exempt list or is an individual LRS remittance: neither form is needed

What Does Form 15CB Contain?

Form 15CB is structured around two broad sections: the remittance details and the CA’s tax analysis and certification. Here is what each part captures:

Remitter and remittee details:

- Name, address, and PAN/TAN of the remitter (the Indian entity sending money)

- Name, address, and country of residence of the non-resident recipient

Remittance details:

- Nature and purpose of the remittance (for example: fees for technical services, royalty, interest, salary, capital gains, dividend)

- RBI purpose code under which the remittance is classified

- Amount in foreign currency and in Indian Rupees

- Proposed date of remittance

- Bank through which the remittance is made

Tax analysis by the CA:

- Whether the payment is chargeable to tax in India under the Income Tax Act, and under which specific section

- Whether a DTAA exists between India and the payee’s country

- If DTAA applies: which article of the DTAA governs this income, and the rate specified in that article

- Whether the non-resident has provided a valid Tax Residency Certificate (TRC) and, where required, Form 10F

- Whether the payee has a Permanent Establishment (PE) in India (critical for business income payments)

- The applicable TDS rate (the lower of the Indian rate and the DTAA rate, if applicable)

- The amount of TDS computed on the remittance

- Confirmation that TDS has been deducted at the applicable rate

- Challan details: BSR code, date of deposit, challan serial number, and amount of TDS deposited

CA’s certification:

- A declaration that the CA has examined the remitter’s accounts, books, documents, and information relevant to the remittance

- Certification that the particulars stated in Form 15CB are true and correct to the best of the CA’s knowledge and belief

- CA’s name, address, ICAI membership number, Firm Registration Number (FRN), UDIN, date, and place of signing

What the CA Examines Before Issuing Form 15CB

The CA’s certification is not a formality. Before issuing Form 15CB, a thorough examination is expected. Here is what a CA typically reviews:

1. The underlying contract or invoice

The CA reviews the commercial agreement between the Indian entity and the non-resident. This establishes the nature of the payment: is this a payment for services rendered in India or abroad? Is it a software licence fee (royalty) or a payment for custom software development (technical services)? Is it interest on a loan or a dividend? The characterisation of the income drives everything that follows.

2. The nature of income and applicable section

Based on the contract, the CA determines under which section of the Income Tax Act (Section 9) the income is deemed to accrue or arise in India, and which head of income it falls under. Common categories:

- Royalties: Section 9(1)(vi)

- Fees for Technical Services (FTS): Section 9(1)(vii)

- Interest: Section 9(1)(v)

- Dividends: Section 9(1)(iv) (rare now given dividend taxation changes)

- Capital gains: Section 9(1)(i)

- Salary: Section 9(1)(ii)/(iii)

3. DTAA applicability and the relevant article

The CA checks whether India has a DTAA with the payee’s country. If yes, the CA identifies the article of the DTAA that covers this income type. Different DTAAs have different rates and definitions. For example, the India-USA DTAA, the India-UK DTAA, and the India-Singapore DTAA all have different rates for royalties and FTS.

4. Tax Residency Certificate (TRC)

The TRC is a certificate issued by the foreign country’s tax authority (for example, the US Internal Revenue Service issues Form 6166; the UK’s HMRC issues an apostille certificate; Singapore’s IRAS issues a COR) confirming that the payee is a tax resident of that country during the relevant period.

A valid TRC is mandatory to claim DTAA benefits. Without it, the CA cannot certify eligibility for the reduced DTAA rate, and TDS must be applied at the standard Indian rate (or the higher Section 206AA rate if PAN is unavailable).

The TRC must:

- Be issued by the tax authority of the payee’s country

- Confirm the payee’s name, address, and status as a tax resident

- Cover the relevant financial year or assessment year

5. Form 10F

Form 10F is a self-declaration filed electronically by the non-resident on the Indian Income Tax e-filing portal. It is required when the TRC does not contain all the information that the Indian tax rules require, specifically: status of the taxpayer, nationality, TIN in the home country, address in the home country, and the period for which residency is certified.

From 16 September 2023, Form 10F must be filed electronically on the Income Tax portal by the non-resident (or their authorised representative). A manually signed, paper-based Form 10F is no longer valid.

If the TRC already contains all these required details, a separate Form 10F may not be needed. The CA verifies whether all required details are present in the TRC before deciding if Form 10F is additionally needed.

6. No Permanent Establishment declaration

This matters particularly for business income payments or situations involving royalties and FTS. If the non-resident has a Permanent Establishment (PE) in India, the DTAA usually provides that profits attributable to that PE are taxable in India as Indian business income, and DTAA rate protection may not apply (or applies differently).

The CA obtains a declaration from the non-resident confirming they have no PE or business connection in India. This is sometimes called a “withholding tax declaration” or “no PE declaration.”

7. Proof of TDS deduction and deposit

The CA must verify that the TDS computed has actually been deducted and deposited. This is confirmed through:

- The TDS challan (showing BSR code, date of deposit, challan serial number, and amount)

- Form 26QB (for property purchase from NRI under Section 195, though Section 195 applies here, not 194-IA)

- The TDS return filed (Form 27Q for payments to non-residents)

8. Currency conversion rate

Foreign currency amounts must be converted to Indian Rupees using the Telegraphic Transfer Buying Rate (TTBR) of the State Bank of India as on the last day of the month immediately preceding the month in which the tax was deducted or paid. The CA must use this specific rate, not the invoice rate or any commercial rate. The CA typically takes a screenshot of the SBI TTBR on the relevant date and retains it as documentation.

A Critical Detail: TDS Rate Is Based on the Year of Deduction, Not the Year of Accrual

This is a nuance that trips up many remitters and is important for the CA to flag clearly in Form 15CB.

Under Section 195, TDS must be deducted at the time of payment or credit, whichever is earlier. If a liability is accrued in one financial year but actually paid in a later year, the TDS rate applicable is the rate in force in the year of actual deduction, not the year of accrual.

Example: An Indian company accrued ₹40 lakh as fees for technical services payable to a US entity in FY 2022-23 (when the Finance Act rate for FTS was 10%). The payment is actually made in FY 2023-24 (when the Finance Act increased the rate to 20%). The TDS must be deducted at 20%, not 10%, because that is the rate prevailing at the time of actual deduction.

However, the DTAA rate (which requires TRC and Form 10F) is determined based on the period to which the income relates. So the CA must obtain a TRC valid for FY 2022-23 to support the DTAA claim, while computing TDS at the FY 2023-24 rate if that rate applies.

This means a delayed payment can create a higher TDS obligation, even though the underlying transaction is from an earlier year. The CA must certify the correct rate in Form 15CB accordingly.

Worked Examples: Form 15CB for Different Types of Remittances

Example 1: Fees for Technical Services to a US Consultant

Situation: Infinity Tech Pvt. Ltd. (Indian company) hires a US-based consultant to develop a machine learning model. The consultant invoices $12,000 (approximately ₹10,08,000 at ₹84/$). The aggregate payments to this consultant in FY 2025-26 total $14,000 (approximately ₹11,76,000). The consultant provides a valid TRC (Form 6166 from the IRS) and files Form 10F electronically.

CA analysis:

- Nature of payment: Fees for Included Services under Article 12 of the India-USA DTAA (equivalent to FTS under Indian law)

- Without DTAA: 20% TDS (Finance Act rate for FTS under Section 115A/195)

- DTAA rate (India-USA, Article 12): 15% on FTS paid to US resident

- TRC: Valid Form 6166 for the relevant period, Form 10F on record

- No PE declaration: Obtained from the consultant

- Applicable TDS rate: 15% (lower of Indian rate and DTAA rate)

- TDS = 15% of ₹11,76,000 = ₹1,76,400

- TTBR used: SBI TTBR as on last day of month preceding TDS deduction

- Form 15CB certifies: Income falls under Article 12 of India-USA DTAA, rate 15%, TDS of ₹1,76,400 deducted and deposited

What Form 15CA will show: Part C, referencing the Form 15CB acknowledgement number.

Example 2: Royalty for Software Licence to a UK Company

Situation: A Mumbai-based publisher pays £30,000 as licence fee to a UK software company for using their editorial management software. Aggregate payments in the year: £30,000 (approximately ₹3,22,200 at ₹107.4/£). UK company has a TRC from HMRC and files Form 10F.

CA analysis:

- Nature: Royalty under Section 9(1)(vi) of the IT Act (payment for use of copyright / software)

- Without DTAA: 20% TDS (Finance Act rate)

- India-UK DTAA: Article 13 – royalty taxable in India at 15%

- Whether it’s royalty or business income: the CA must check if this is use of a copyrighted product (royalty) versus purchase of software outright (not royalty). Since this is a licence fee, it qualifies as royalty.

- PE analysis: No PE declaration obtained from UK company

- TDS rate: 15% (DTAA rate is lower)

- TDS = 15% of ₹3,22,200 = ₹48,330

- Form 15CB certifies the above

Note: The characterisation debate (royalty vs business income) for software payments has been a long-standing issue in Indian tax law. A CA must carefully review the nature of the software transaction before classifying it as royalty in Form 15CB.

Example 3: Interest Payment to a German Parent Company

Situation: A German company lent €1,00,000 to its Indian subsidiary at 8% per annum. Interest for FY 2025-26 = €8,000 (approximately ₹7,31,200 at ₹91.4/€). The German parent provides a TRC from the German Federal Central Tax Office (Bundeszentralamt für Steuern) and files Form 10F electronically.

CA analysis:

- Nature: Interest under Section 9(1)(v) of the IT Act

- India-Germany DTAA: Article 11 – interest taxable in India at a limited rate (check the specific article for the exact rate, commonly 10%)

- Without DTAA: 20% (Finance Act rate for interest payments)

- PE analysis: Not directly relevant for interest income, but the CA verifies the loan is not attributable to a PE in India

- Thin capitalisation: The CA checks whether the interest is deductible in India under Section 94B (thin capitalisation rules), which limits deductions on interest paid to associated enterprises in excess of 30% of EBITDA

- TDS rate: 10% (DTAA rate, if applicable and lower)

- TDS = 10% of ₹7,31,200 = ₹73,120

- Form 15CB certifies the applicable DTAA article, rate, and TDS amount

Critical nuance: The CA must also check whether the interest has actually been credited to the foreign parent’s account before the TDS deduction, because Section 195 requires deduction at the time of credit or payment, whichever is earlier. Many Indian subsidiaries accrue interest in their books without formally crediting the parent’s account, which is a common error.

Example 4: NRI Property Sale and Repatriation

Situation: An NRI sold residential property in Chennai for ₹90 lakh. The Indian buyer is required to deduct TDS under Section 195 (not Section 194-IA, which applies to resident sellers). The NRI’s Long Term Capital Gains = ₹40 lakh. The NRI now wants to repatriate the net sale proceeds from their NRO account.

CA analysis at the time of repatriation:

- Nature: Repatriation of sale proceeds after TDS already deducted by buyer

- TDS on capital gains: Should have been deducted by buyer under Section 195 at 20% on LTCG (or at DTAA rate if applicable)

- The CA verifies: TDS challan filed by buyer, Form 27Q filed, TDS visible in NRI’s Form 26AS/AIS

- If TDS was correctly deducted: Form 15CB certifies the remittance, confirming tax has been deducted on the capital gains component

- Form 15CA: Part C if aggregate > ₹5 lakh and CA certificate in place, or Part B if AO certificate (Form 13 / Section 197 order) exists

- The CA must verify whether the NRI obtained a lower/nil withholding certificate under Section 197 before the property sale, which some NRIs arrange in advance to reduce the buyer’s TDS obligation

Practical note: For NRIs, the property sale and repatriation are two separate steps. The TDS deduction happens at the time of sale. The Form 15CB for repatriation is about the completed tax position, not computing fresh TDS.

Example 5: Dividend to Non-Resident Shareholder

Situation: An Indian company distributes a dividend of ₹8,00,000 to a Singapore-based shareholder (a foreign company holding 25% stake).

CA analysis:

- Nature: Dividend under Section 8 / Section 115A of the Income Tax Act

- India-Singapore DTAA: Article 10 – dividends may be taxed in India at 10% if the Singapore company holds at least 25% of shares in the Indian company; otherwise 15%

- TDS under Indian law (Section 194 for residents, Section 195 for non-residents): Standard rate is 20% plus cess

- DTAA rate: 10% (with valid TRC)

- PE analysis: Dividend income from PE may be treated differently

- TDS = 10% of ₹8,00,000 = ₹80,000 (using DTAA rate with valid TRC + Form 10F)

- Form 15CB certifies the above

Documents the Remitter Must Provide to the CA

When engaging a CA for Form 15CB, the following documents should typically be submitted:

- A copy of the invoice or contract for the remittance

- The payee’s Tax Residency Certificate (TRC) covering the relevant period

- Electronically filed Form 10F from the payee (or confirmation it has been filed on the IT portal)

- A “No PE” declaration or withholding tax declaration from the payee

- Proof of TDS deduction: the TDS challan (BSR code, date, serial number, amount)

- Board resolution or internal authorization for the remittance (for companies)

- Any earlier Form 15CB or correspondence with the AO about this payee, if relevant

- Screenshot of SBI TTBR for the relevant date (for the CA’s currency conversion)

A CA typically issues Form 15CB within 1 to 2 working days for straightforward payments like professional fees and interest with a standard DTAA. Royalties, capital gains, and transactions involving PE analysis can take 3 to 5 working days due to the additional complexity.

UDIN: Mandatory for Every Form 15CB

A Unique Document Identification Number (UDIN) is mandatory for every Form 15CB issued by a CA. The CA must:

- Generate the UDIN on the ICAI’s UDIN portal (udin.icai.org) specifically for the Form 15CB

- Incorporate the UDIN in Form 15CB before uploading it to the Income Tax e-filing portal

- A Form 15CB without a UDIN is not valid

The UDIN serves as an authenticity check: anyone can verify on the ICAI portal that the certificate was genuinely issued by the CA and has not been tampered with. This is particularly important since Form 15CB is presented to banks, who rely on it to process high-value wire transfers.

CA’s Professional Responsibility and Penalty Exposure

The CA signing Form 15CB takes on a professional responsibility that goes beyond a standard filing. The Income Tax Act specifically provides for a penalty against CAs:

- Section 271J: A penalty of ₹10,000 can be levied on a CA for furnishing incorrect information in Form 15CB, where the inaccuracy is attributable to the CA’s negligence or incorrect certification

This is separate from the ₹1,00,000 penalty under Section 271-I that falls on the remitter (covered in our Form 15CA article). Both can apply in a case of incorrect certification.

The CA is not responsible for the correctness of the underlying commercial transaction, but is responsible for the accuracy of the tax analysis and certification. If a CA issues Form 15CB based on documents provided by the remitter and later discovers those documents were false, the CA’s liability is reduced, though professional diligence is still expected.

How to File Form 15CB: The CA’s Process

Form 15CB is filed exclusively online, by the CA, using their Digital Signature Certificate. The remitter cannot file Form 15CB.

- Step 1: The CA logs into the Income Tax e-filing portal (incometax.gov.in) using their own PAN and password (not the remitter’s credentials).

- Step 2: Goes to e-File → Income Tax Forms → File Income Tax Forms and selects Form 15CB.

- Step 3: Fills in all required fields: remitter details, remittee details, remittance details, tax analysis (nature, section, DTAA article, TDS rate, amount), and TDS payment challan details.

- Step 4: Generates a UDIN on the ICAI portal and enters it in the form.

- Step 5: E-verifies Form 15CB using their Digital Signature Certificate (DSC). Unlike some other forms that allow EVC (OTP-based verification), Form 15CB requires DSC-based verification by the CA.

- Step 6: On successful submission, an acknowledgement number is generated. The CA provides this acknowledgement number to the remitter, who then uses it while filing Form 15CA Part C.

- Step 7: The remitter files Form 15CA Part C (referencing the Form 15CB acknowledgement), e-verifies it, and presents both acknowledgement numbers to the bank.

Common Errors in Form 15CB

Using the wrong DTAA rate.

The CA must look up the specific DTAA between India and the payee’s country, not apply a generic rate. Rates vary significantly across DTAAs.

Not checking PE status.

For business income or FTS, if the payee has a PE in India, the DTAA business profits or FTS article may not protect them, and the income attributable to the PE may be taxable at normal rates.

Using an expired or invalid TRC.

The TRC must be valid for the relevant financial year. A TRC for the wrong period does not support the DTAA rate claim.

Using the wrong exchange rate.

The SBI TTBR on the last day of the month before deduction is the prescribed rate under Rule 26. Using any other rate (like the invoice date rate or the payment date rate) is technically incorrect.

Characterising income incorrectly.

The most consequential error is mislabelling the income type. A software licence fee classified as “business income” instead of “royalty” can result in the wrong article of the DTAA being applied, the wrong rate being used, and the wrong amount of TDS being deducted.

Not verifying TDS deposit before issuing Form 15CB.

The form must certify that TDS has been deducted and deposited. Issuing Form 15CB before the TDS challan is created is incorrect.

Form 15CB Is Becoming Form 146

Under the Income Tax Act, 2025 (effective from 1 April 2026) and the Income Tax Rules, 2026, Form 15CB is being renamed Form No. 146, while Form 15CA becomes Form 145. This was confirmed by multiple sources including Vakilsearch (May 2026).

The core structure, requirements (TRC, Form 10F, UDIN, DSC filing), and the ₹5 lakh threshold remain unchanged. Only the form number changes. For all remittances and certifications relating to payments made:

- On or before 31 March 2026: Use Form 15CB as described in this article. Historical Form 15CB certifications remain valid compliance records.

- From 1 April 2026 onwards: Form 146 applies under the new framework. Monitor CBDT and ICAI notifications for any procedural updates under the new rules.

Form 15CB vs Form 15CA: A Quick Comparison

| Form 15CB | Form 15CA | |

| What it is | CA’s tax determination certificate | Remitter’s declaration |

| Who files it | Chartered Accountant (using their DSC) | The remitter (Indian entity or individual sending money) |

| When required | Only for Part C (taxable remittance above ₹5 lakh, no AO certificate) | For all reportable remittances (Parts A, B, C, or D) |

| Must be filed before | Form 15CA Part C | The remittance itself |

| What it certifies | Tax analysis, DTAA applicability, TDS rate, TDS deduction confirmation | Declaration of remittance details and tax compliance |

| UDIN required? | Yes, mandatory | No (but DSC/EVC verification required) |

| Penalty for error | ₹10,000 under Section 271J (on the CA) | ₹1,00,000 under Section 271-I (on the remitter) |

| Can be withdrawn? | No specific provision | Yes, within 7 days of Form 15CA submission |

| New name from April 2026 | Form 146 | Form 145 |

Frequently Asked Questions

1. Can the remitter file Form 15CB themselves?

No. Form 15CB can only be prepared and filed by a practising Chartered Accountant with a Certificate of Practice from ICAI. The CA must use their own DSC to file it. The remitter has no access to file Form 15CB.

2. Is Form 15CB required for every remittance above ₹5 lakh?

Only for remittances that are taxable in India and exceed ₹5 lakh in aggregate during the financial year (to the same non-resident), where no AO certificate has been obtained. Non-taxable remittances use Part D of Form 15CA without Form 15CB.

3. How long is a Form 15CB valid?

There is no explicit validity period prescribed for Form 15CB. However, it should be closely tied to the actual remittance and the related TDS deposit. Using a Form 15CB from months ago for a fresh remittance is not advisable; the CA should issue a fresh certificate for each remittance event or for each financial year in which a payment is made.

4. Can one Form 15CB cover multiple invoices from the same payee?

Generally, one Form 15CB is issued per remittance event. If multiple invoices are being settled in a single payment, one Form 15CB covering the aggregate payment is typically acceptable, provided all invoices relate to the same nature of income and the same DTAA treatment.

5. What if the non-resident does not provide a TRC?

Without a TRC, the CA cannot certify DTAA rate eligibility. TDS must be applied at the standard Indian rate under Section 195 read with the Finance Act (typically 20% for FTS and royalties, or 30% for other income). If the payee also lacks a PAN, Section 206AA may push the rate even higher.

6. Can Form 15CB be issued if TDS has not yet been deducted?

Technically, the CA certifies that TDS has been deducted, which means the TDS should precede the Form 15CB. In practice, the sequence is: compute TDS, deposit TDS in the government account, generate the TDS challan, and then the CA uses the challan details to complete Form 15CB.

7. My company makes quarterly interest payments to a foreign lender. Do we need a new Form 15CB each quarter?

Yes, typically. Each payment event where TDS is deducted requires a corresponding Form 15CB (and Form 15CA Part C), since each payment has its own TDS challan and deduction date.

Key Takeaways

- Form 15CB is a CA-certified tax determination certificate required for taxable remittances to non-residents that exceed ₹5 lakh in aggregate during the financial year, where no AO certificate exists.

- The CA examines the contract/invoice, the nature of income, the DTAA between India and the payee’s country, the TRC, Form 10F, and the No PE declaration before issuing the certificate.

- TDS rate in Form 15CB is the lower of the Indian rate (under Section 195 / Finance Act) and the applicable DTAA rate (which requires a valid TRC and Form 10F).

- The TTBR (SBI Telegraphic Transfer Buying Rate) on the last day of the month preceding deduction is the prescribed conversion rate for foreign currency.

- TDS rate is based on the year of deduction, not the year of accrual. Delayed payments can attract the rate prevailing at the time of actual payment.

- UDIN is mandatory for Form 15CB. The CA must generate it on the ICAI portal and embed it in the form before uploading.

- Form 15CB must be filed by the CA using DSC and must precede the remitter’s filing of Form 15CA Part C.

- The CA faces a ₹10,000 penalty under Section 271J for furnishing incorrect information in Form 15CB.

- From 1 April 2026, Form 15CB is renamed Form 146 under the Income Tax Act, 2025. Structure, requirements, and thresholds remain the same.

Sources: Income Tax Department, Government of India: Form 15CA FAQs; Vakilsearch: Form 15CA and 15CB for Foreign Remittance Certification, May 2026; Taxguru: Basic Understanding on Form 15CA and 15CB; CA Rajput: Form 15CB Situation: Rate of Tax Based on Year of Deduction.

This article is for general information only and does not constitute tax or professional advice. For guidance specific to a particular remittance, consult a practising Chartered Accountant with experience in international taxation.