Quick summary: If you earn income from a foreign country and pay tax on it there, India’s tax laws also require you to declare that income in your Indian tax return, because you are a resident Indian and your worldwide income is taxable in India. This can lead to the same income being taxed twice: once in the foreign country and once in India. To prevent this unfairness, the Income Tax Act allows you to claim a Foreign Tax Credit (FTC), which reduces your Indian tax bill by the amount you already paid abroad. To claim this credit, you must file Form 67 on the Income Tax e-filing portal, along with supporting documents from the foreign country. Missing this form means losing the credit entirely.

What Is Double Taxation and Why Does FTC Exist?

Imagine Priya, a software engineer in Pune, who also works as a freelance consultant for a US company. The US company deducts federal withholding tax before paying her. When Priya files her Indian income tax return, she must also declare that US income because she is a Resident and Ordinarily Resident (ROR) Indian, and India taxes its residents on their global income.

Without any relief, Priya would pay tax twice on the same income: once to the US government and once to the Indian government. This is called double taxation, and it would be deeply unfair.

Foreign Tax Credit (FTC) is the mechanism that prevents this. It allows Priya to claim a credit against her Indian tax liability for the tax she already paid in the US. The result: she pays tax on that income only once in effect, not twice.

FTC is not automatic. It must be actively claimed. And to claim it, Form 67 must be filed.

The Legal Framework: Sections 90, 91, and Rule 128

FTC in India rests on two sections of the Income Tax Act, 1961 and one rule:

Section 90: DTAA-based (bilateral) relief

India has signed Double Taxation Avoidance Agreements (DTAAs) with over 90 countries, including the United States, the United Kingdom, Australia, the UAE, Singapore, Canada, Germany, Japan, and many others. When a taxpayer earns income from a country with which India has a DTAA, and that DTAA provides for FTC, the taxpayer can claim credit under Section 90.

Section 91: Unilateral relief

For income from a country with which India does not have a DTAA, Section 91 still provides relief. It is called unilateral relief because India grants it on its own, without a treaty obligation. This is less common but important for income from countries where no DTAA exists.

Rule 128: The procedure

Rule 128 of the Income Tax Rules, 1962 (effective from 1 April 2017) lays down the detailed procedure for claiming FTC: who can claim it, what income qualifies, how to compute the credit, which documents to attach, and the timeline for filing Form 67. Everything covered in this article flows from Rule 128.

Who Can Claim Foreign Tax Credit?

Only resident Indians can claim FTC. Non-Resident Indians (NRIs) are generally taxed in India only on income that accrues or arises in India, so their foreign income is typically not taxable in India. FTC applies when both countries are taxing the same income.

More specifically, the following types of taxpayers are eligible:

- Resident and Ordinarily Resident (ROR) individuals: All foreign income is taxable in India and FTC applies.

- Resident but Not Ordinarily Resident (RNOR) individuals: Only income derived from business controlled from or profession exercised in India is taxable globally; other foreign income has limited taxability. FTC applies to the extent foreign income is taxable in India.

- Companies: FTC can also be claimed by Indian resident companies on foreign income taxed abroad. This includes companies paying tax under MAT (Minimum Alternate Tax under Section 115JB).

What Income Qualifies for FTC?

Not every payment made outside India qualifies for FTC. The credit is available only for:

- Income that is taxable in India (declared in the Indian ITR)

- Income on which income tax was paid in the foreign country

- Income for which the Indian tax year in which it is offered to tax in India is the year for which FTC is claimed

What does NOT qualify:

- Penalties charged by foreign tax authorities

- Interest charged on overdue taxes in the foreign country

- Value Added Tax (VAT) or Goods and Services Tax (GST) paid abroad

- Social security taxes or payroll taxes paid abroad

- US Self-Employment Tax (SE Tax): this is a common misconception among Indian freelancers earning from US clients. The SE Tax is a social security contribution, not an income tax. Only the US federal income tax withheld qualifies for FTC.

- Platform fees or service charges: these are not taxes at all, even if deducted at source by a foreign payment platform

How to Calculate Foreign Tax Credit

The FTC allowed is the lower of:

- The foreign income tax paid on the income (converted to Indian Rupees), or

- The Indian tax payable on that same foreign income (calculated at Indian tax rates)

This ensures you are never better off than if you had paid tax only in India. If you paid more tax abroad than what India would have charged on that income, you only get credit up to the Indian tax amount. The excess foreign tax is not refunded and cannot be carried forward.

Currency conversion rule: Foreign tax is converted to Indian Rupees using the Telegraphic Transfer Buying Rate (TTBR) as on the last day of the month immediately preceding the month in which the tax was deducted or paid in the foreign country. You cannot use any other exchange rate.

FTC is computed separately for each country and each source of income. You cannot pool FTC from one country against income from another country.

A Worked Example

Vikram is an ROR Indian resident working as a freelance data scientist. In FY 2025-26, he earns ₹6,00,000 from Indian clients and USD 10,000 (approximately ₹8,40,000 at ₹84 per USD) from a US client. The US client deducts US federal withholding tax of USD 1,500 (approximately ₹1,26,000 at TTBR).

- Step 1: Compute total Indian income Total income = ₹6,00,000 (India) + ₹8,40,000 (US) = ₹14,40,000

- Step 2: Compute Indian tax on total income (simplified, at applicable slab rate) Say Indian tax on ₹14,40,000 = ₹2,20,000 (this varies by regime and deductions; purely illustrative)

- Step 3: Compute Indian tax on the US income alone Indian tax rate on the last portion of income = say 20% Indian tax on US income of ₹8,40,000 = approximately ₹1,68,000 (illustrative)

- Step 4: Compute FTC allowed Foreign tax paid = ₹1,26,000 Indian tax on foreign income = ₹1,68,000 FTC allowed = lower of the two = ₹1,26,000

- Step 5: Compute net Indian tax payable Indian tax = ₹2,20,000 Less FTC = ₹1,26,000 Net tax payable in India = ₹94,000

Without FTC, Vikram would pay ₹2,20,000 to India plus ₹1,26,000 to the US = ₹3,46,000 in total. With FTC, he pays ₹94,000 to India plus ₹1,26,000 to the US = ₹2,20,000 in total. The credit has saved him ₹1,26,000 in Indian taxes.

This example is simplified for clarity. Actual computations may differ based on slabs, surcharge, cess, deductions, and the specific DTAA provisions applicable.

What Is Form 67?

Form 67 is the prescribed statement under Rule 128 that a resident taxpayer must furnish to claim FTC. It is formally titled “Statement of income from a country or specified territory outside India and Foreign Tax Credit.”

Filing Form 67 is not optional. The Income Tax Department will not allow the FTC claim if Form 67 is not filed within the specified deadline, even if all the supporting documents are in order and the credit is genuinely eligible.

Structure of Form 67

Part A: Contains basic identification details of the assessee (name, PAN or Aadhaar number, address, assessment year) and the core FTC claim details:

- Country or specified territory from which the income arose

- Article number of the DTAA used (if claiming under Section 90)

- Nature of the income (salary, professional fees, dividend, interest, capital gains, etc.)

- Amount of income in foreign currency

- Amount of income in Indian Rupees (converted using the applicable rate)

- Amount of foreign tax paid (in foreign currency and in Indian Rupees at TTBR)

- Indian tax payable on that foreign income

- FTC claimed (lower of the two)

If you have income from multiple countries or multiple sources within the same country, each combination gets a separate row in Part A.

Part B: Contains details relevant to two specific situations:

- Foreign tax refunded as a result of carry-backward of losses in the foreign country, affecting FTC claimed in an earlier year

- Details of disputed foreign tax (tax that is under appeal or litigation in the foreign country)

FTC cannot be claimed for disputed foreign tax. If the dispute is resolved in the taxpayer’s favour (tax is refunded), or if the tax is confirmed and paid, a revised claim needs to be made.

Verification section: A self-declaration by the taxpayer (or authorised person) confirming that the information provided is true and correct to the best of their knowledge.

Attachments section: Where you attach the supporting documents (details below).

Documents Required to File Form 67

The following documents must be attached when filing Form 67:

1. Certificate or statement from the foreign tax authority: An official document from the government of the foreign country confirming the nature of income and the amount of tax deducted or paid. For example, a Form 1042-S or Form W-2 from the US, a P60 or payslip showing UK PAYE deductions, or a Tax Deduction Certificate from a foreign company.

2. Proof of payment of foreign tax: A receipt, challan, or bank statement showing the actual payment of tax to the foreign government. For withholding taxes, this is typically already included in the certificate from the employer or payer.

3. Foreign employer certificate (for salaried employees on deputation abroad): A certificate from the foreign employer specifying the amount of TDS deducted from salary, the period it covers, and the nature of the tax.

4. Dividend or interest income: Broker statements, dividend vouchers, or Form 1099-DIV/1099-INT (in the case of US income) showing tax withheld.

5. Foreign income tax return (if filed): If you filed a tax return in the foreign country and paid taxes as per that assessment, attach a copy of the foreign ITR and the payment proof.

All documents in a foreign language should be accompanied by a certified English translation.

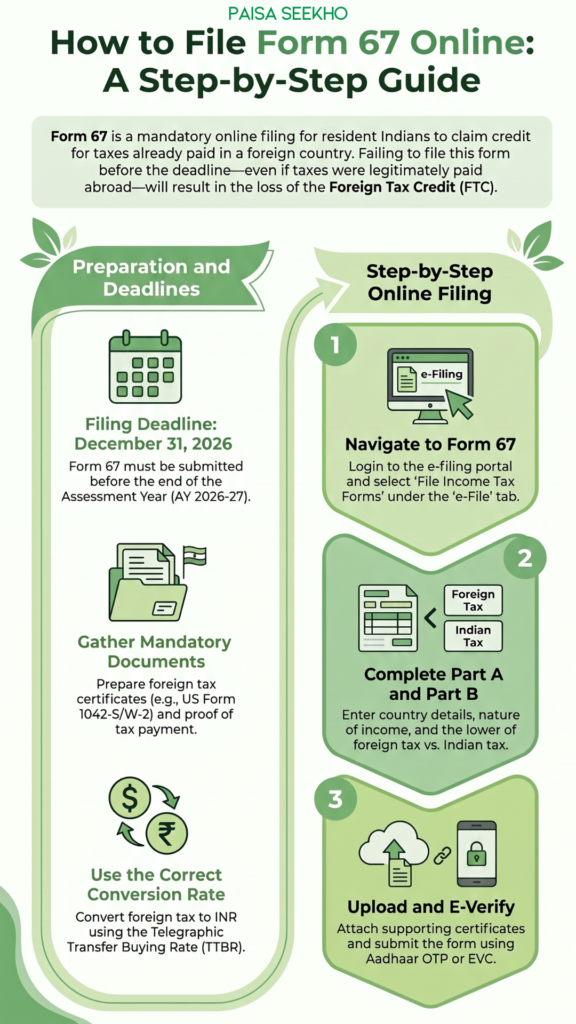

Due Dates for Form 67 (AY 2026-27)

This is where many people get confused, because the due date rule changed in 2022. Here is the current position as per Rule 128(9), as amended by the Income Tax (Twenty-Seventh Amendment) Rules, 2022 (with retrospective effect from 1 April 2022):

Form 67 must be filed on or before the end of the assessment year in which the foreign income is offered to tax in India, provided the income tax return has been filed within the time specified under Section 139(1) (original return) or Section 139(4) (belated return).

What this means for FY 2025-26 (AY 2026-27):

- The assessment year 2026-27 ends on 31 December 2026

- Form 67 must be filed on or before 31 December 2026

- This applies even if your ITR is filed by the standard due date (31 July 2026 for non-audit cases or 31 October 2026 for audit cases)

Special case: Updated return under Section 139(8A):

If you file an updated return to include previously omitted foreign income, Form 67 for that income must be filed on or before the date of filing the updated return (not the end of the assessment year).

Important exception for Section 90 relief:

For claiming relief specifically under Section 90 (DTAA-based FTC), some interpretations require Form 67 to be filed before the end of the assessment year strictly. To be safe, file Form 67 before you file your ITR, which is the recommended practice in any case.

Best practice:

File Form 67 before or on the same day as your ITR. Do not wait until December. Filing it early eliminates any ambiguity about deadlines and ensures everything is in order before the return is processed.

How to File Form 67 Online: Step by Step

Form 67 can only be filed online. There is no physical or offline option.

- Step 1: Log into the Income Tax e-filing portal (incometax.gov.in) using your PAN and password.

- Step 2: Go to e-File → Income Tax Forms → File Income Tax Forms.

- Step 3: Under the category “Persons with No Business Income” (or Business Income, as applicable), search for and select Form 67.

- Step 4: Select the relevant Assessment Year (AY 2026-27 for FY 2025-26) and click Let’s Get Started.

- Step 5: Fill in Part A: your basic details, and then for each source of foreign income, enter the country name, nature of income, income amount in foreign currency and INR, foreign tax paid in foreign currency and INR (at TTBR), Indian tax on that income, and the FTC claimed.

- Step 6: Fill in Part B if applicable (disputed tax or loss carry-back situations).

- Step 7: Proceed to the Verification section. Complete the self-declaration.

- Step 8: Upload the supporting attachments (certificate of foreign tax, proof of payment, etc.) in the Attachments section.

- Step 9: Click Preview to review the entire form. If everything looks correct, proceed to Submit.

- Step 10: E-verify the form using Aadhaar OTP, net banking EVC, or other available modes.

- Step 11: An acknowledgement number is generated. Save this carefully.

After Form 67 is filed and accepted, you can file your ITR and claim the FTC in Schedule TR (Tax Relief) of your ITR (along with reporting foreign income in Schedule FSI and foreign assets in Schedule FA).

Where to Claim FTC in Your ITR

Filing Form 67 is only one part of the FTC claim. The ITR itself must also reflect the foreign income and the credit:

- Schedule FSI (Foreign Source Income): Report each source of foreign income separately: country name, head of income, gross income, taxes paid in the foreign country, and taxes payable in India.

- Schedule TR (Tax Relief): Claim the actual FTC based on what you have filed in Form 67. The figures in Schedule TR must match Form 67.

- Schedule FA (Foreign Assets): If you hold any foreign assets (bank accounts, investments, property, insurance, etc.), they must be disclosed in Schedule FA, regardless of whether they generated income. Non-disclosure of foreign assets carries severe penalties and potentially criminal prosecution under the Black Money Act, 2015.

Applicable ITR forms:

- ITR-2: For individuals and HUFs with foreign income but no business income (most salaried employees and investors)

- ITR-3: For individuals with foreign income plus business or professional income (freelancers, consultants)

- ITR-6: For companies

Common Situations Where Form 67 Is Needed

1. Indian IT professionals on deputation to US, UK, or other countries:

If you spent part of the year abroad working, and tax was withheld there, and you are still an Indian tax resident (ROR), Form 67 is required to claim credit for the tax withheld in that country.

2. Freelancers and consultants earning from foreign clients:

If a US company, UK company, or any foreign client withholds tax from your payment (for example, US 30% withholding tax under Chapter 3 of the Internal Revenue Code), you can claim FTC for the income tax portion of that withholding. Platform deductions (Upwork fees, PayPal charges) are not taxes and do not qualify.

3. Indians holding US stocks or ETFs:

If you own US stocks or ETFs (through the LRS route or international mutual fund FoF) and receive dividends on which 25% or 30% US dividend withholding tax is deducted, you can claim FTC for that tax against your Indian tax on the same dividend income. For more on how international investments work, see our guide on how to invest in international mutual funds in India.

4. Former NRIs returning to India:

If you have returned to India and become a tax resident, any foreign income (such as rental income from a property abroad, dividends from foreign stocks, or pension from a foreign employer) is now taxable in India. FTC applies for taxes paid on this income in the source country.

5. Indian students or professionals who filed returns abroad:

If you filed a tax return in a foreign country and paid tax there, and the income is also reportable in India (because you became a resident), Form 67 covers the credit for that tax paid.

Key Rules to Remember

FTC is capped at Indian tax on that income.

If you paid 30% tax in the US on income and India’s tax rate on that income is 20%, you can claim only 20% as FTC. The excess 10% is not refunded and cannot be carried forward to future years.

FTC is computed source by source, country by country.

You cannot offset FTC from US income against Indian tax on UK income, or mix FTC from dividends with FTC from salary.

Disputed foreign tax does not qualify.

If you are contesting a tax demand in a foreign country, you cannot claim FTC for that amount while the dispute is pending.

Only income tax qualifies.

Social security, payroll tax, VAT, withholding on gross receipts (not income), platform charges, these all do not qualify as FTC.

Form 67 must be filed before the end of the assessment year.

Missing this deadline means losing the FTC claim for that year. You may apply for condonation of delay with a valid reason, but there is no guarantee it will be granted.

Form 67 Is Becoming Form 44

Under the Income Tax Act, 2025 (effective from 1 April 2026), Form 67 has been renumbered as Form No. 44. As confirmed by Tax2win based on the notified Income Tax Rules, 2026: “Form 67 has now been renumbered as Form 44 under the Income Tax Act 2025. The revised form will come into effect from 1st April 2026.”

For FY 2025-26 (AY 2026-27): Foreign income earned up to 31 March 2026 falls under the old Income Tax Act, 1961. Continue using Form 67 as described in this article. The AY 2026-27 ends on 31 December 2026, which is your deadline for filing Form 67.

For Tax Year 2026-27 (income from April 2026 onwards): Form 44 under the new Income Tax Act, 2025 applies. Keep an eye on the Income Tax Department’s notifications for the exact format and procedure when they are released.

Frequently Asked Questions

1. Is Form 67 mandatory even if I have DTAA protection?

Yes. Even if India has a DTAA with the country where you paid tax, you must still file Form 67 to formally claim the FTC. DTAA protection does not make the form optional.

2. I paid tax in the UAE. There is no income tax there. Can I claim FTC?

If there was no actual income tax paid in the UAE (since the UAE introduced corporate tax only in 2023 and personal income tax does not exist there), there is no foreign tax to credit. FTC only applies when you have actually paid foreign income tax. You would need to verify if any tax was withheld at source in the UAE on any specific income.

3. I forgot to file Form 67 along with my ITR. Can I still claim FTC?

Under the amended Rule 128(9), you have until the end of the assessment year (31 December 2026 for AY 2026-27) to file Form 67, even if your ITR has already been filed. File it as soon as possible. If the assessment year has passed, you would need to apply for condonation of the delay with a valid reason. There is no guarantee of acceptance.

4. Can a company claim FTC?

Yes. Indian resident companies that earn foreign income taxed abroad can claim FTC by filing Form 67. This applies even when the company pays tax under MAT (Minimum Alternate Tax) under Section 115JB. For more on MAT, see our article on Form 29B explained under MAT provisions.

5. My US client deducted 30% withholding tax. Can I claim all of it as FTC?

Not necessarily. FTC is capped at the Indian tax payable on that income. If India’s effective tax rate on your US income is, say, 20%, you can claim only 20% of the income as FTC (which equals 20% of your US income in INR terms), not the full 30% deducted in the US. The excess 10% is not creditable and is not refunded by either country.

6. Do I need to file Schedule FA even if I only have a foreign bank account with a small balance?

Yes. Schedule FA requires disclosure of all foreign assets, including bank accounts, regardless of the balance. Non-disclosure of even a small foreign asset can attract a penalty of ₹10 lakh per year under the Black Money Act, 2015. This is separate from Form 67 and FTC claims.

7. What is the TTBR and where do I find it?

TTBR stands for Telegraphic Transfer Buying Rate. It is the rate at which the State Bank of India (SBI) buys foreign currency. For income tax purposes, you use the TTBR as on the last day of the month preceding the month in which the foreign tax was deducted or paid. You can find historical TTBR rates on the SBI website or through CBDT notifications.

8. Can I claim FTC on foreign taxes paid in a previous year?

FTC is claimed in the year the income is taxed in India. If you earned income in a foreign country in FY 2024-25 and paid tax there, but the same income is taxed in India in FY 2025-26 (for example, due to accounting differences), you claim FTC for AY 2026-27. FTC is linked to the Indian tax year, not the foreign tax year.

Key Takeaways

- Form 67 is the mandatory statement filed by resident Indian taxpayers to claim Foreign Tax Credit (FTC) for taxes paid abroad on income that is also taxable in India.

- It is filed under Rule 128 of the Income Tax Rules, 1962, and the FTC is claimed under Section 90 (DTAA countries) or Section 91 (non-DTAA countries) of the Income Tax Act.

- Only income tax paid abroad qualifies. Penalties, social security, VAT, platform fees, and US Self-Employment Tax do not qualify.

- FTC equals the lower of the foreign tax paid (in INR at TTBR) or the Indian tax payable on the same income. Excess foreign tax is neither refunded nor carried forward.

- FTC is computed separately for each country and each income source. Cross-country or cross-source netting is not allowed.

- Form 67 must be filed before the end of the assessment year (31 December 2026 for AY 2026-27), provided the ITR was filed on time. Best practice: file Form 67 before or along with your ITR.

- After filing Form 67, also report foreign income in Schedule FSI, claim the FTC in Schedule TR, and disclose foreign assets in Schedule FA of your ITR.

- From Tax Year 2026-27 (income from April 2026 onwards), Form 67 is renamed Form No. 44 under the Income Tax Act, 2025.

Sources: Income Tax Department, Government of India: Form 67 User Manual; Income Tax Department: Rule 128, Income Tax Rules, 1962; Tax2win: Form 67 of Income Tax Act Explained; ClearTax: Form 67 and Claim of Foreign Tax Credit.

This article is for general information only and does not constitute tax or legal advice. For guidance specific to your situation, including country-specific DTAA provisions, consult a practising Chartered Accountant or a tax professional experienced in international taxation.