Quick summary: Every time an Indian resident or company sends money to a non-resident individual or foreign company, Indian tax law requires the remitter to first ensure that any applicable tax has been deducted. To formally communicate this to the Income Tax Department, the remitter files an online declaration called Form 15CA before making the payment. In many cases, a Chartered Accountant must also certify the tax position in Form 15CB before Form 15CA is filed. Banks and Authorised Dealers will not process a foreign wire transfer without these forms, where applicable. This guide explains what Form 15CA is, its four parts, when Form 15CB is required, which remittances are exempt, and how to file.

What Is Form 15CA?

Form 15CA is an online declaration filed by the remitter (the person or entity in India making a payment to a non-resident) before remitting money outside India. It is governed by Section 195(6) of the Income Tax Act, 1961, read with Rule 37BB of the Income Tax Rules, 1962.

The word “remittance” here means any payment from India to a person outside India: salary to a foreign employee, fees to a foreign consultant, royalties to a foreign company, interest to a foreign lender, dividends, or even maintenance money sent to a relative living abroad.

Section 195 requires tax (TDS) to be deducted from any payment made to a non-resident if that payment is chargeable to tax in India. Form 15CA is the mechanism by which the remitter formally tells the Income Tax Department: “I am making this payment, here are the details, and here is what I have done about TDS.”

Banks and Authorised Dealers (ADs) who process outward foreign exchange transfers are required to collect Form 15CA from the remitter and submit it to the Income Tax Department for any tax-related proceedings. Without the Form 15CA acknowledgement number (and Form 15CB, where required), most banks will not process an outward SWIFT wire transfer.

What Is Form 15CB and How Does It Relate to Form 15CA?

Before going into the parts of Form 15CA, it helps to understand Form 15CB, because the two are interdependent.

Form 15CB is a certificate issued by a practising Chartered Accountant under Section 195(6). In it, the CA examines the nature of the remittance, the relevant Double Taxation Avoidance Agreement (DTAA) provisions, the applicable TDS rate, and certifies whether the tax deduction has been correctly computed.

The CA must examine:

- The contract or invoice underlying the payment

- The country of the payee and whether India has a DTAA with that country

- The nature of the income (royalty, professional fees, interest, salary, capital gains, etc.)

- Whether a lower TDS rate applies under DTAA

- If the payee has a Tax Residency Certificate (TRC) or Form 10F to claim DTAA benefits

When Form 15CB is required, it must be completed and certified by the CA before the remitter files Form 15CA, because Part C of Form 15CA requires details from the Form 15CB (such as the CA’s name, membership number, and the Form 15CB acknowledgement number).

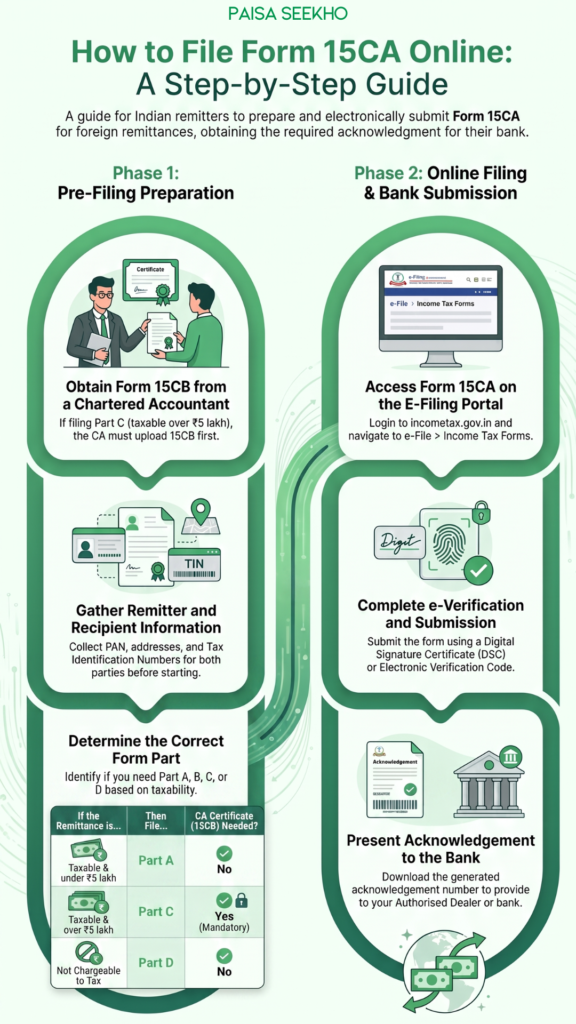

The Four Parts of Form 15CA

Form 15CA is divided into four parts. Which part you fill depends on two filters: (1) the total amount remitted to that non-resident during the financial year, and (2) whether the remittance is taxable and how the taxability has been determined.

Part A: Taxable remittance below ₹5 lakh

When to use: When the remittance or the aggregate of all remittances to that non-resident during the financial year does not exceed ₹5 lakh, and the remittance is taxable under the Income Tax Act.

Is Form 15CB required? No.

The remitter self-declares the details of the payment and the TDS deducted, without needing a CA certificate. This covers smaller payments for which the compliance burden is kept minimal.

Part B: Taxable remittance above ₹5 lakh with an Assessing Officer certificate

When to use: When the remittance or its aggregate exceeds ₹5 lakh during the financial year, and the remitter has obtained an order or certificate from the Assessing Officer under:

- Section 195(2): AO determines the proportion of the amount actually chargeable to tax

- Section 195(3): AO grants a certificate that the payee’s total income justifies lower or nil TDS deduction

- Section 197: AO issues a lower deduction certificate for the payee

Is Form 15CB required? No. The AO certificate replaces the CA certificate.

This route is used when the remitter has gone to the tax department directly to get clarity on the TDS obligation.

Part C: Taxable remittance above ₹5 lakh with Form 15CB from a CA

When to use: When the remittance or its aggregate exceeds ₹5 lakh during the financial year, the remittance is taxable, and the remitter has obtained a Form 15CB certificate from a Chartered Accountant.

Is Form 15CB required? Yes, mandatory.

This is the most commonly used part for businesses and professionals making foreign payments above ₹5 lakh. The sequence is: engage a CA, CA issues Form 15CB, remitter then files Form 15CA Part C using the Form 15CB details, and presents both acknowledgements to the bank.

Part D: Remittance not chargeable to tax

When to use: When the remittance is not chargeable to tax in India under the Income Tax Act, for reasons other than those covered by the Rule 37BB exemption list (where no Form 15CA is needed at all).

Is Form 15CB required? No.

Part D is used for remittances like capital account transactions, gifts to close relatives, and other payments that are genuinely outside the tax net in India but still need to be declared to the bank. The remitter declares the nature of the payment and that it is not taxable.

Choosing the Right Part: A Decision Tree

Use this sequence to determine which part of Form 15CA applies:

Step 1: Is the remittance in the Rule 37BB exemption list (33 specified categories) or is it an LRS remittance by an individual that does not require RBI approval?

- If YES: No Form 15CA or 15CB required at all. Stop here.

- If NO: Go to Step 2.

Step 2: Is the remittance chargeable to tax in India?

- If NOT chargeable to tax: File Part D.

- If chargeable to tax: Go to Step 3.

Step 3: Does the aggregate remittance to this non-resident during the financial year exceed ₹5 lakh?

- If NO (total under ₹5 lakh): File Part A (no Form 15CB needed).

- If YES (total exceeds ₹5 lakh): Go to Step 4.

Step 4: Do you have an order/certificate from the Assessing Officer under Section 195(2), 195(3), or 197?

- If YES: File Part B (no Form 15CB needed).

- If NO: Get Form 15CB from a CA and file Part C.

When Is Form 15CA NOT Required?

Rule 37BB(3) specifies two broad categories of remittances that are completely exempt from the Form 15CA requirement:

Category 1: Individual LRS remittances

Remittances made by an individual that do not require prior approval of the Reserve Bank of India (under Section 5 of FEMA read with Schedule III to the Foreign Exchange Current Account Transactions Rules, 2000) do not require Form 15CA. This covers personal remittances under the Liberalised Remittance Scheme (LRS), which allows resident individuals to remit up to $250,000 per year for permitted purposes.

Common LRS-purpose examples that do not need Form 15CA:

- Sending money to a child studying abroad (tuition and maintenance)

- Medical treatment abroad

- Personal travel expenses

- Gifting money to a close relative abroad

- Investing in foreign stocks or ETFs under LRS

Category 2: The Rule 37BB list of 33 exempt payments

This is a schedule of specific payment categories that are by their nature either not income for the recipient or already addressed through other compliance mechanisms. The list was expanded from 28 to 33 categories by CBDT Notification No. 93/2015. Key examples include:

- Payment for imports covered under a Bill of Entry (most trade payments for goods imported into India)

- Pre-payment for imports

- Business travel expenses incurred by Indian companies abroad

- Payment of salaries to Indian nationals deputed abroad

- Operating expenses of Indian business offices abroad

- Operating expenses of Indian embassies and consulates

- Repayments of loans taken by Indian companies from abroad (principal repayment)

- Refunds and rebates on export invoices

- Payments to foreign embassies in India

- Contributions to international organisations (like the UN, IMF, World Bank) by the Government of India

If the remittance falls under any of these 33 categories, neither Form 15CA nor Form 15CB is required. Banks generally map the RBI purpose code of the remittance against this list to determine applicability. If the purpose code corresponds to an exempt category, no forms are needed.

A Practical Example

Precision Technologies Pvt. Ltd., an Indian company, has hired a US-based software consultant for a project. The consultant has invoiced $15,000 (approximately ₹12,60,000) for services rendered. India has a DTAA with the United States.

- Step 1: Is it in the Rule 37BB exempt list? Payments for professional/technical services to a non-resident are not in the exempt list. So Form 15CA is required.

- Step 2: Is it taxable? Yes. Fees for technical services to a non-resident are taxable in India under Section 195 read with the India-USA DTAA. The applicable withholding rate under Article 12 of the India-USA DTAA is typically 15% on royalties and fees for included services.

- Step 3: Does the aggregate exceed ₹5 lakh? Yes, ₹12,60,000 exceeds ₹5 lakh.

- Step 4: Does Precision Technologies have an AO certificate? No.

- Conclusion: Precision Technologies must obtain a Form 15CB from its CA, then file Form 15CA Part C, deduct TDS at the applicable rate, and present both acknowledgements to its bank before the wire transfer is processed.

What Information Does Form 15CA Contain?

Regardless of which part is filed, Form 15CA captures:

- Remitter details: Name, address, PAN, TAN (if applicable), and email/phone

- Recipient details: Name, address, country of residence, email/phone, and PAN or Tax Identification Number of the non-resident (if available)

- Remittance details: Nature of the remittance (salary, royalty, professional fees, interest, dividend, capital gains, gift, etc.), amount in foreign currency and Indian Rupees, currency name, and the proposed date of remittance

- Bank details: Name of the bank and branch through which the remittance is being made

- Tax details (for taxable remittances): Whether TDS has been deducted, the TDS rate applied, the amount of TDS, the basis for the rate (Indian tax law or DTAA), whether a DTAA applies, and the relevant DTAA article

- Form 15CB details (for Part C): CA’s name, membership number, and the Form 15CB acknowledgement number

For Part D (not taxable), the remitter declares the specific reason the remittance is not chargeable to tax.

How to File Form 15CA Online: Step by Step

Form 15CA is filed exclusively online. There is no physical or offline submission.

- Step 1: If Form 15CB is required (Part C), ask your CA to prepare and upload Form 15CB on the Income Tax e-filing portal first. Obtain the Form 15CB acknowledgement number from the CA.

- Step 2: Log into the Income Tax e-filing portal (incometax.gov.in) using your PAN and password.

- Step 3: Go to e-File → Income Tax Forms → File Income Tax Forms. Search for and select Form 15CA.

- Step 4: Select the correct part (A, B, C, or D) based on the decision tree above.

- Step 5: Fill in all the required fields. For Part C, enter the Form 15CB details provided by your CA.

- Step 6: Submit the form and e-verify it using your Digital Signature Certificate (DSC) or EVC (Electronic Verification Code). If a DSC is registered for the entity, e-verification must be done using DSC.

- Step 7: On successful submission, an acknowledgement number is generated. Download and save this, along with the PDF of the submitted form.

- Step 8: Present the Form 15CA acknowledgement number (and Form 15CB if applicable) to your bank or Authorised Dealer when initiating the foreign wire transfer.

Timing: Form 15CA must be filed before the remittance is made. There is no prescribed earlier deadline, but the form must be submitted and acknowledged before the bank processes the transfer.

Withdrawal: If the remittance ultimately does not go through, Form 15CA can be withdrawn within 7 days from the date of submission. The withdrawal link is available on the portal during this window. After 7 days, withdrawal is not possible.

What Does the Bank Do With Form 15CA?

Under the revised Rule 37BB, banks and Authorised Dealers are obligated to:

- Collect the Form 15CA acknowledgement from the remitter before processing the transfer (for applicable remittances)

- Submit the received Form 15CA data to the Income Tax Department for any proceedings under the Income Tax Act

- Refuse to process the transfer if applicable forms are not provided

This is why banks ask for the Form 15CA number on their outward remittance request forms (such as the A2 form required for SWIFT transfers). The bank’s compliance officers verify the acknowledgement number online before releasing the funds.

NRO to NRE Account Transfers and Form 15CA

A situation that frequently comes up for NRIs: when transferring money from an NRO (Non-Resident Ordinary) account to an NRE (Non-Resident External) account, Form 15CA is typically required.

NRO accounts hold income earned in India (rent, salary, dividends, capital gains). When an NRI wants to repatriate this money by moving it to an NRE account, the source income (interest, rent, capital gains, etc.) is taxable in India under Section 195. So the compliance chain applies: assess the tax on the NRO income (TDS is usually already deducted by the bank or tenant), obtain Form 15CB from a CA, and file Form 15CA Part C or D as applicable.

The bank managing the NRI’s account will typically require Form 15CA and Form 15CB before processing the repatriation. This is separate from the TDS already deducted on the NRO income itself.

For the receiving end, when a foreign person (non-resident) earns income from India and those taxes are already withheld in India, that person can claim foreign tax credit in their home country for the Indian taxes deducted. Our guide on Form 67 for foreign tax credit covers the Indian side of this equation, where resident Indians claim credit for taxes paid abroad.

Form 15CA and the Tax Audit: Clause 43

For businesses that are required to get a tax audit done under Section 44AB, Clause 43 of Form 3CD requires disclosure of all payments made outside India for which Form 15CA was required to be furnished. This includes the name of the payee, the country, the amount remitted, and whether Form 15CA was actually filed.

Any mismatch (remittance made but Form 15CA not filed, or Form 15CA filed with incorrect details) noted in Clause 43 can trigger scrutiny from the Income Tax Department. For more on what Form 3CD covers, see our Form 3CD tax audit report guide.

Penalty for Non-Filing or Incorrect Filing

Under Section 271-I of the Income Tax Act, failing to furnish Form 15CA or furnishing inaccurate particulars attracts a penalty of ₹1,00,000 per default. This penalty applies even if the remittance itself was made correctly and TDS was deducted accurately. The breach is the failure to file the form, not just the failure to deduct tax.

The penalty is per instance of default, not per financial year. So if a company made five non-compliant remittances, the potential penalty is ₹5,00,000.

Common Mistakes to Avoid

Filing the wrong part:

Using Part D (not chargeable to tax) when the remittance is actually taxable, to avoid Form 15CB, is a serious compliance error. The bank may process the transfer, but the Income Tax Department can subsequently flag it.

Not obtaining Form 15CB before filing Part C:

The sequence is fixed: Form 15CB must come first. You cannot file Part C of Form 15CA and then get the CA to certify later.

Using the wrong TDS rate:

Check the applicable DTAA rate carefully. Paying at 20% (the standard rate without DTAA) when the DTAA rate is 10% or 15% means the remitter over-deducts, and the non-resident has to claim a refund.

Not filing when importing:

Many companies assume that all import payments are exempt. While imports under a valid Bill of Entry (goods already cleared through customs) are exempt, pre-payments for imports without a Bill of Entry may still require Form 15CA. Check the purpose code carefully.

Forgetting to present the form to the bank:

Form 15CA must be submitted to the bank before the transfer. An online-submitted but bank-not-presented Form 15CA is incomplete compliance.

Important: Form 15CA Is Becoming Form 145

Under the Income Tax Act, 2025 (effective from 1 April 2026) and the Income Tax Rules, 2026, Form 15CA has been renamed Form No. 145 and Form 15CB has been renamed Form No. 146. As confirmed by Vakilsearch and Eztax:

- The governing section shifts from Section 195 (old Act) to Section 393(2) [Table: S.No. 17] of the Income Tax Act, 2025

- The four-part structure of the form remains unchanged

- The ₹5 lakh threshold remains unchanged

- The Rule 37BB exemption list remains unchanged

- Only the form numbers change from 15CA/15CB to 145/146

For all remittances made on or before 31 March 2026: continue using Forms 15CA and 15CB as described in this article.

For remittances made from 1 April 2026 onwards (Tax Year 2026-27): use Forms 145 and 146. Historical Form 15CA and 15CB submissions before April 2026 remain valid records of compliance. Keep an eye on the Income Tax Department’s official notifications for the exact format and portal process under the new forms. Our article on April 2026 financial rule changes covers the broader transition to the new Income Tax Act.

Form 15CA vs Form 15CB: Quick Reference

| Form 15CA | Form 15CB | |

| What it is | Declaration by the remitter | Certificate by a Chartered Accountant |

| Who files | The person or company making the remittance | A practising CA appointed by the remitter |

| When required | Before every reportable remittance to a non-resident | Only when remittance exceeds ₹5 lakh and is taxable (Part C) |

| Legal basis | Section 195(6), Rule 37BB | Section 195(6) |

| Filed on | Income Tax e-filing portal (by the remitter) | Income Tax e-filing portal (by the CA using DSC) |

| Sequence | Filed after Form 15CB (if 15CB is needed) | Filed before Form 15CA Part C |

| Can be withdrawn? | Yes, within 7 days | No specific withdrawal provision |

| Penalty for default | ₹1,00,000 per instance (Section 271-I) | ₹1,00,000 per instance (Section 271-I) |

| New name from April 2026 | Form 145 | Form 146 |

Frequently Asked Questions

1. Is Form 15CA required for every payment to a non-resident?

No. Payments that fall under the 33 exempt categories in Rule 37BB, or that are LRS remittances by individuals not requiring RBI approval, do not require Form 15CA. For all other payments to non-residents that are chargeable to tax, Form 15CA is required.

2. What if I send money to a relative abroad as a gift?

If you are an individual and the remittance is within the LRS limit ($250,000 per year) and does not require prior RBI approval, no Form 15CA is required. A gift to a close relative abroad under LRS for maintenance falls in this category.

3. My company is importing goods from the US. Do I need Form 15CA to pay the supplier?

Payments for imports where a Bill of Entry has been filed (goods already cleared at customs) are on the Rule 37BB exempt list. No Form 15CA is needed in this case. However, advance payments for imports before a Bill of Entry is filed may still require Form 15CA, depending on the purpose code. Check with your bank and CA.

4. Can I file Form 15CA after making the remittance?

No. Form 15CA must be filed before the remittance. Banks will not process the transfer without the Form 15CA acknowledgement (where applicable). Filing it after the fact does not cure the non-compliance.

5. Does Form 15CA apply to payments in Indian Rupees to a non-resident’s NRO account?

Generally, payments in Indian Rupees credited directly to an NRO account (such as TDS-deducted rent or bank interest) do not require Form 15CA, because the money stays within India’s banking system. Form 15CA becomes relevant when the NRI wants to repatriate the accumulated NRO balance to an NRE account or remit it outside India.

6. What is a Tax Residency Certificate (TRC) and when is it needed?

A TRC is a certificate issued by the tax authority of the payee’s country confirming that the payee is a tax resident of that country. It is required when claiming a lower DTAA rate in the Form 15CB. Without a TRC, the CA cannot certify eligibility for the reduced rate. The payee (non-resident) must provide the TRC and, where required, Form 10F to the remitter.

7. Is there a time limit for filing Form 15CA?

There is no specific prescribed time limit beyond “before the remittance.” However, withdrawal is only possible within 7 days of submission. For practical purposes, file it close to the actual remittance date to keep the acknowledgement valid.

8. My bank says Form 15CA is not needed for this payment but my CA says it is. Who is right?

Banks rely on the RBI purpose code to determine applicability. If the purpose code corresponds to an exempt Rule 37BB category, the bank may waive the requirement. Your CA’s analysis is based on the actual legal nature of the transaction. In case of doubt, filing Form 15CA (especially Part D if not taxable) is conservative and protects you from a penalty.

Key Takeaways

- Form 15CA is a mandatory online declaration filed by the remitter (the person or entity in India making the payment) before remitting money to a non-resident, under Section 195(6) of the Income Tax Act read with Rule 37BB.

- It has four parts: Part A (taxable, under ₹5 lakh), Part B (taxable, over ₹5 lakh with AO certificate), Part C (taxable, over ₹5 lakh with Form 15CB from a CA), and Part D (not chargeable to tax).

- Form 15CB is a CA certificate required only for Part C. It must be prepared and submitted by the CA before the remitter files Part C of Form 15CA.

- No Form 15CA or 15CB is needed for: (a) LRS remittances by individuals not requiring RBI approval, and (b) payments covered by the 33 exempt categories listed in Rule 37BB (including imports under Bill of Entry, business travel, medical treatment, education, and maintenance of relatives abroad).

- Form 15CA must be filed before the remittance and can be withdrawn within 7 days if the remittance does not proceed.

- Penalty: ₹1,00,000 per default for non-filing or inaccurate filing under Section 271-I.

- From 1 April 2026, Form 15CA is renamed Form 145 and Form 15CB is renamed Form 146 under the Income Tax Act, 2025. The structure, thresholds, and exemptions remain the same.

Sources: Income Tax Department, Government of India: Form 15CA FAQs; Income Tax Department, Government of India: Rule 37BB, Income Tax Rules, 1962; Vakilsearch: Form 15CA and 15CB for Foreign Remittance Certification Under Section 195, May 2026; ClearTax: Form 15CA and 15CB under Rule 37BB.

This article is for general information only and does not constitute tax or legal advice. For guidance specific to your remittance situation, consult a practising Chartered Accountant with experience in international taxation.