Quick summary: While Form 24Q handles the tax deducted from employee salaries, almost every other kind of domestic payment where TDS applies gets reported through a different quarterly return: Form 26Q. If your business pays rent to a landlord, professional fees to a consultant, commission to an agent, interest to a lender, or payments to a contractor, and TDS is deducted on any of these, Form 26Q is the return that reports it to the Income Tax Department. This guide explains exactly what falls under Form 26Q, its due dates for FY 2025-26, the filing process, a new requirement for partnership firms introduced this year, and what changes from April 2026.

What Is Form 26Q and Who Must File It?

Form 26Q is a quarterly statement of tax deducted at source, filed under Section 200(3) of the Income Tax Act, 1961, read with Rule 31A of the Income Tax Rules, 1962. It covers TDS on all payments made to resident Indians other than salary.

Any individual, organisation, or entity responsible for deducting TDS on non-salary payments to Indian residents must file this return quarterly. Both government and non-government deductors are covered, and a valid TAN (Tax Deduction and Collection Account Number) is mandatory to file it. Non-government deductors must quote their PAN on the form, while government deductors quote “PANNOTREQD” instead.

It is important to note that not only companies file Form 26Q. Any individual or HUF required to perform a tax audit must also deduct TDS and file Form 26Q when making specified payments like rent or professional fees, even though they are not a company or a large business entity.

Which Sections and Payment Types Does Form 26Q Cover?

Form 26Q is genuinely a multi-purpose return. Unlike Form 24Q, which handles only one type of payment (salary), Form 26Q consolidates a wide range of different payment categories under one quarterly filing. As of FY 2025-26, it covers TDS under Sections 193, 194, 194A, 194B, 194BB, 194C, 194D, 194EE, 194F, 194G, 194H, 194I, 194J, and 194LA, among others.

Here are the most commonly encountered payment categories reported through Form 26Q:

| Nature of Payment | Section | Typical TDS Rate |

| Interest other than on securities (FD, RD interest) | 194A | 10% |

| Payments to contractors | 194C | 1% (individual/HUF) or 2% (others) |

| Commission or brokerage | 194H | 5% |

| Rent on land, building, furniture | 194I | 2% (plant/machinery) or 10% (land/building) |

| Professional or technical fees | 194J | 10% (professional) or 2% (technical services) |

| Interest on securities | 193 | 10% |

| Winnings from lottery, crossword puzzles | 194B | 30% |

| Winnings from horse races | 194BB | 30% |

| Insurance commission | 194D | Varies |

| Payments on National Savings Scheme deposits | 194EE | 10% |

| Commission on sale of lottery tickets | 194G | 5% |

| Compensation on compulsory acquisition of immovable property | 194LA | 10% |

For businesses, the everyday relevance is straightforward: if you pay a landlord for office space, a freelance consultant for their services, a delivery contractor for logistics, or an agent their commission, and the payment crosses the applicable threshold, TDS applies under one of these sections, and it gets reported through Form 26Q.

For a detailed explanation of the professional fees and technical services split under Section 194J, and how the TDS certificate for these payments works, see our Form 16A guide.

What Is New for FY 2025-26: Section 194T for Partnership Firms

This is a genuinely important update that many partnership firms and their accountants may not yet be tracking closely.

Partnership firms must now use Form 26Q to report salary, bonus, or interest paid to their partners under the new Section 194T. Previously, payments from a partnership firm to its own partners (in the form of salary, remuneration, bonus, commission, or interest on capital) fell outside the standard TDS net, since partners were not treated the same way as third-party employees or vendors for withholding tax purposes.

From FY 2025-26, this has changed. Partnership firms making qualifying payments to partners must now deduct TDS under Section 194T and report it through the same Form 26Q used for all other non-salary payments. If your firm has been paying partners without deducting TDS on these specific payment types, this is worth reviewing with your CA immediately, since the requirement is newly applicable this financial year.

What Information Does Form 26Q Actually Contain?

Unlike Form 24Q, which has two (or three) annexures, Form 26Q contains only one consolidated annexure structure. It requires:

- Deductor details: TAN, PAN, name, and address of the person or entity deducting TDS

- Challan details: BSR code, date of payment, and total amount for every TDS deposit challan used during the quarter

- Deductee details: PAN, name, amount paid or credited, date of deduction, TDS amount deducted, and the specific section under which the deduction was made, for each payee

- Nature of payment code: identifying which of the covered sections (194C, 194J, 194I, 194H, 194A, and so on) applies to each individual payment entry

What Are the Due Dates for Form 26Q for FY 2025-26?

| Quarter | Period | Due Date |

| Q1 | April to June 2025 | 31 July 2025 |

| Q2 | July to September 2025 | 31 October 2025 |

| Q3 | October to December 2025 | 31 January 2026 |

| Q4 | January to March 2026 | 31 May 2026 |

These are the same quarterly deadlines that apply to Form 24Q (salary TDS) and Form 27Q (TDS to non-residents), so if your organisation is filing multiple TDS returns each quarter, they all fall due together.

Before you can file the quarterly return, the deducted tax itself must already be deposited with the government. For non-government deductors, the standard TDS deposit deadline is the 7th of the following month. The single exception is TDS deducted in March, for which the deposit deadline extends to 30 April of the following financial year.

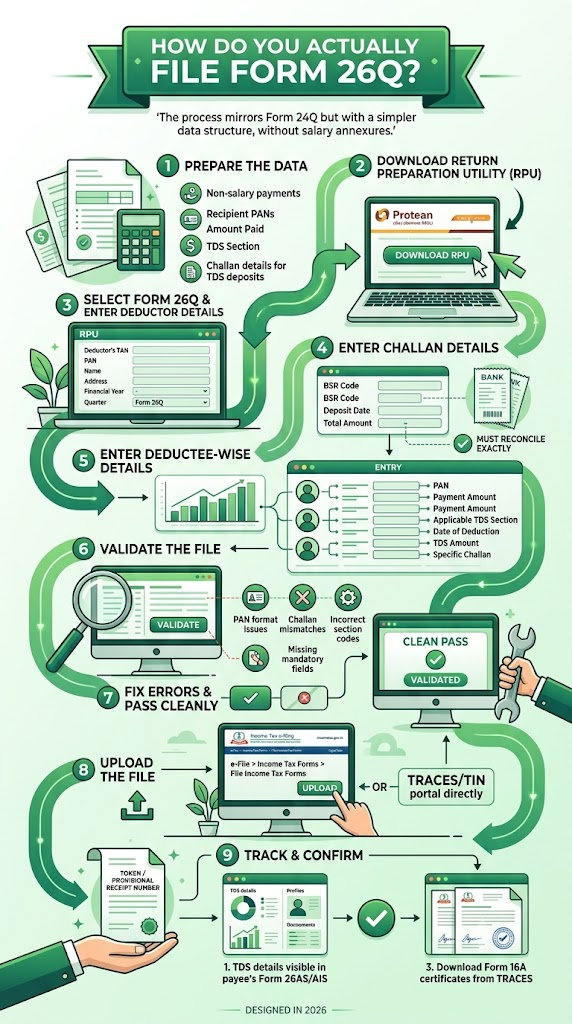

How Do You Actually File Form 26Q?

The process closely mirrors Form 24Q, since both use the same underlying utility and portal infrastructure, but Form 26Q’s data structure is somewhat simpler since it does not carry the salary-computation annexures.

- Step 1: Prepare the data. Collect details of every non-salary payment made during the quarter that attracted TDS: the PAN of each recipient, the amount paid, the section under which TDS was deducted, and the challan number and details for every corresponding TDS deposit.

- Step 2: Download the Return Preparation Utility (RPU) from the Protean eGov (formerly NSDL) website.

- Step 3: Select Form 26Q in the RPU and enter the deductor’s TAN, PAN, name, and address, along with the financial year and quarter being filed.

- Step 4: Enter challan details. For every TDS challan deposited during the quarter, enter the BSR code, deposit date, and total amount. This must reconcile exactly with your bank-generated challan receipts.

- Step 5: Enter deductee-wise details. For each payee, enter their PAN, the payment amount, the applicable TDS section, the date of deduction, the TDS amount, and the specific challan against which it was deposited.

- Step 6: Validate the file. Run the entered data through the File Validation Utility (FVU) to check for errors: PAN format issues, challan mismatches, incorrect section codes, and missing mandatory fields.

- Step 7: Fix any errors flagged during validation until the file passes cleanly.

- Step 8: Upload the file. Log in to the Income Tax e-filing portal (incometax.gov.in) using your TAN, navigate to e-File > Income Tax Forms > File Income Tax Forms, and upload your validated file. Alternatively, filing can be done through the TRACES/TIN portal directly.

- Step 9: Track and confirm. After upload, you receive a token or provisional receipt number. Once processed, the TDS details become visible in each payee’s Form 26AS and AIS, and you can download Form 16A certificates for each payee from TRACES.

What Happens If You Deposit TDS Under the Wrong Section?

This is a common, entirely fixable error. If TDS is deposited under the wrong section, for example, if a payment was actually a rent payment under Section 194I but was mistakenly recorded and deposited under Section 194J (professional fees), the fix is to file a correction return in TRACES to update the section using the consolidated file, following the same correction process used for any other Form 26Q amendment: download the consolidated file for that quarter, correct the section reference in the RPU, revalidate, and upload the correction statement.

This kind of error matters because the deductee’s Form 26AS entry will show the TDS credited under the wrong head, which can create complications when they file their own return and try to reconcile their income and TDS credits.

What Penalties Apply for Late or Incorrect Filing?

The penalty structure for Form 26Q mirrors that of Form 24Q, since both fall under the same general TDS compliance framework.

Late filing fee (Section 234E):

₹200 per day of delay, accumulating until it equals the total TDS amount for that quarter. This fee must be paid via challan before the return submission is even accepted by the portal.

Interest for late deduction:

1% per month from the date TDS should have been deducted until the actual date of deduction.

Interest for late deposit:

1.5% per month from the date of deduction to the actual date of deposit.

Discretionary penalty (Section 271H):

The Assessing Officer may levy a penalty ranging between ₹10,000 and ₹1,00,000 for failure to file within the prescribed time, or for furnishing incorrect information in the return. As with Form 24Q, this penalty can generally be avoided if the deductor pays the TDS, applicable fee, and interest, and files the statement within the current relief window applicable for the assessment year in question.

A large penalty is specifically levied if a deductor fails to both file the TDS return and deposit the corresponding amount within one year of the actual due date, so prolonged non-compliance compounds the financial exposure significantly beyond the standard late fee.

Form 26Q vs Form 24Q vs Form 27Q: What Is the Difference?

| Form 26Q | Form 24Q | Form 27Q | |

| What it covers | Non-salary payments to residents | Salary payments | Non-salary payments to non-residents |

| Governing sections | 193, 194, 194A, 194C, 194H, 194I, 194J, and others | 192 | 195, 196B, 196C, 196D, and others |

| Certificate generated | Form 16A | Form 16 | Form 16A (with different fields for non-residents) |

| Annexure structure | Single annexure | Annexure I (all quarters), Annexure II and III (Q4 only) | Single annexure |

| TAN required? | Yes | Yes | Yes |

A business that pays employee salaries, contractor invoices, and rent for its office premises will typically be filing Form 24Q and Form 26Q every quarter, both using the same TAN. If that business also makes payments to a foreign vendor or consultant, Form 27Q comes into the mix as well.

Do Individuals and HUFs Ever File Form 26Q?

Generally, individuals and HUFs who are not subject to a tax audit are exempt from the TAN-based TDS system entirely, since specific carve-outs exist for their common transaction types:

- Property purchase (Section 194-IA): individuals use Form 26QB with their PAN, no TAN needed

- Rent payments above ₹50,000/month (Section 194-IB): individuals use Form 26QC with their PAN, no TAN needed

- Contractor or professional payments above ₹50 lakh (Section 194M): individuals use Form 26QD with their PAN, no TAN needed

These specific carve-outs exist precisely so that ordinary individuals do not need to obtain a TAN or file quarterly Form 26Q returns for these particular transaction types. For a deeper look at these individual-specific challan-cum-statement forms, see our guides on Form 26QB, Form 26QC, and Form 26QD.

However, if an individual or HUF is subject to a tax audit under Section 44AB, this exemption does not apply. Such individuals and HUFs must obtain a TAN and file Form 26Q like any other business deductor, for payments like rent or professional fees that fall outside the specific individual carve-out sections above.

Important: Form 26Q Is Becoming Form 140

This is one of the more structurally significant changes taking effect under India’s new tax framework, and it is worth understanding in some detail because of how thoroughly the underlying section numbering changes.

Under the Income Tax Act, 2025 (effective from 1 April 2026) and the Income Tax Rules, 2026, the entire 194-series of TDS sections is retired. In their place, the new Act consolidates TDS provisions into three parent sections: Section 392 covers salary TDS (replacing Section 192), Section 393 covers all other TDS payments to both residents and non-residents (replacing the entire 194-series, including 194C, 194J, 194I, 194H, 194A, 194D, 194DA, 194N, 194R, 194S, and others), and Section 394 covers all TCS provisions.

Alongside this, TDS challans and return filings now use numeric payment codes (ranging from 1001 to 1092) instead of the old section numbers. For example, payments to resident contractors that previously cited Section 194C now use specific codes depending on whether the payee is an individual or a company. Professional fees that previously cited Section 194J at 10% now use a different code from technical services that attracted 2% under the same old section, since the two categories that used to share Section 194J are now explicitly split into separate payment codes with distinct rates.

Using an old section number, such as 194C or 194J, when filing a return for a payment made on or after 1 April 2026 will trigger system-level validation errors at the time of filing, requiring a correction statement to fix.

The certificate generated from these filings also changes: Form 16A (the certificate for non-salary TDS) becomes Form 131 under the new framework, and the return itself, currently Form 26Q, becomes Form 140.

One important carve-out to note: Section 194-IA transactions (property purchase TDS) are not folded into the new Form 140. A separate return form continues to apply for that specific transaction type under the new framework, distinct from the general non-salary TDS return.

For FY 2025-26 (payments made up to 31 March 2026):

Continue using Form 26Q and the existing 194-series section numbers exactly as described in this article, under the old Income Tax Act, 1961.

For Tax Year 2026-27 (payments made from 1 April 2026 onwards):

Use Form 140, referencing the new Section 393 payment codes rather than the old 194-series section numbers. Update your accounting and payroll software before your first quarterly filing under the new framework, since old section references will not validate correctly on the portal for new-year transactions.

Frequently Asked Questions

1. What is the difference between Form 26Q and Form 24Q?

Form 24Q is strictly for reporting TDS deducted on employee salary payments under Section 192. Form 26Q covers TDS on all other domestic payments to residents, including rent, professional fees, contractor payments, commission, and interest, spanning multiple different sections of the Income Tax Act.

2. Do I need a TAN to file Form 26Q?

Yes. A Tax Deduction Account Number is mandatory for filing Form 26Q. This differs from certain individual-specific transactions (like property purchase, rent above ₹50,000/month, or high-value contractor payments by non-audited individuals/HUFs), which use PAN-based forms instead and do not require a TAN.

3. My partnership firm pays partners a monthly remuneration. Do I need to deduct TDS on this now?

Potentially, yes, starting FY 2025-26. Under the new Section 194T, partnership firms are now required to deduct TDS on qualifying salary, bonus, commission, or interest payments made to partners, and report these through Form 26Q. Review your firm’s payment structure with a Chartered Accountant to confirm whether Section 194T applies to your specific payments.

4. I accidentally deposited TDS under Section 194J instead of Section 194I. How do I fix this?

File a correction return through TRACES. Download the consolidated file for the relevant quarter, update the section reference for the affected deductee entry in the RPU, revalidate, and upload the corrected FVU file as a correction statement.

5. Does an individual who is not running a business need to file Form 26Q?

Generally no, unless that individual is subject to a mandatory tax audit under Section 44AB. Individuals not subject to audit use the specific PAN-based challan-cum-statement forms (Form 26QB for property, Form 26QC for rent, Form 26QD for contractor/professional payments) instead, which do not require a TAN or quarterly Form 26Q filing.

6. Is Form 26Q filed monthly or quarterly?

Quarterly. The underlying TDS deposits happen monthly (by the 7th of the following month, with a March exception extending to 30 April), but the return itself, consolidating that quarter’s deductions and deposits, is filed once per quarter by the prescribed due date.

7. What replaces Form 26Q from April 2026?

Form 140, under the Income Tax Act, 2025 and Income Tax Rules, 2026. It uses new numeric payment codes referencing Section 393 instead of the old 194-series section numbers, though the fundamental structure of quarterly non-salary TDS reporting remains conceptually the same.

Key Takeaways

- Form 26Q is the quarterly TDS return for all payments other than salary made to resident Indians, filed under Section 200(3) of the Income Tax Act, covering sections including 194A, 194C, 194H, 194I, 194J, and several others.

- It requires a TAN and applies to any deductor, business or individual, above the applicable thresholds, with a specific exception for non-audited individuals/HUFs using PAN-based forms (26QB, 26QC, 26QD) for specific transaction types.

- New for FY 2025-26: partnership firms must now report TDS on salary, bonus, or interest paid to partners under the new Section 194T through Form 26Q.

- FY 2025-26 due dates: Q1: 31 July 2025, Q2: 31 October 2025, Q3: 31 January 2026, Q4: 31 May 2026, matching the Form 24Q schedule.

- Form 16A is the TDS certificate generated from Form 26Q filings, downloadable from TRACES for each deductee.

- Penalties mirror Form 24Q: ₹200/day under Section 234E, interest for late deduction and deposit, and a discretionary ₹10,000 to ₹1,00,000 penalty under Section 271H.

- From Tax Year 2026-27 (payments from April 2026 onward), Form 26Q is replaced by Form 140, with the entire 194-series of sections retired in favour of numeric payment codes under the new Section 393 of the Income Tax Act, 2025.

Sources: Motilal Oswal: Form 26Q, TDS Return for Non-Salary Payments, FY 2025-26; ClearTax: TDS and TCS Changes from April 2026; ComputaxOnline: TDS Changes from April 2026, Income Tax Act 2025 Guide, April 2026; FutureX Solutions: TDS and TCS Changes from April 2026, New Sections and Forms, May 2026.

This article is for general information only and does not constitute tax or professional advice. For guidance specific to your TDS compliance, consult a practising Chartered Accountant.