Quick summary: Whenever an Indian resident or business pays rent to an NRI landlord, buys property from an NRI seller, pays professional fees to a foreign consultant, or transfers interest on an overseas loan, tax must be deducted at source under Section 195 of the Income Tax Act before the money changes hands. The quarterly return that reports all of this to the government is Form 27Q. It is functionally similar to Form 26Q, but exclusively for payments flowing to non-residents rather than resident Indians, and it comes with its own distinct rate structure, DTAA considerations, and compliance nuances. This guide explains what Form 27Q covers, the crucial “grossing up” rule, how DTAA rates work, and what changes from April 2026.

What Is Form 27Q and Who Must File It?

Form 27Q is the quarterly statement of tax deducted at source on payments, other than salary, made to non-residents and foreign companies, filed under Section 195 of the Income Tax Act, 1961, read with Section 200(3) and Rule 31A of the Income Tax Rules, 1962.

Any person, whether an individual, a firm, an HUF, or a corporate entity, who makes a payment to a non-resident and deducts TDS under Section 195 or related provisions must file Form 27Q. This is a broad obligation: there is no minimum threshold below which TDS does not apply. TDS under Section 195 applies from the first rupee of taxable income, unlike many resident-payment sections that have specific exemption thresholds.

Before deducting any TDS under this section, the payer must first obtain a TAN (Tax Deduction Account Number) under Section 203A, since the entire Form 27Q filing framework, like Form 24Q and Form 26Q, is built around TAN-based reporting.

What Kinds of Payments Does Form 27Q Cover?

Section 195 is deliberately broad and residual: it is designed to catch any payment, other than salary, made to a non-resident that is taxable in India, where a more specific TDS section does not already apply. Common categories reported through Form 27Q include:

- Interest paid to NRIs or foreign lenders

- Royalty payments to foreign licensors

- Fees for technical services (FTS) paid to foreign consultants or service providers

- Rent paid to NRI landlords

- Professional fees paid to foreign professionals or freelancers

- Capital gains on the sale of property, shares, or other assets by NRIs

- Payments to non-resident sportsmen or sports associations

- Software licence fees and similar payments, subject to the specific classification rules discussed below

- Any other sum chargeable to tax in India and payable to a non-resident, not otherwise specifically covered

Section 195 is genuinely the workhorse section for NRI and foreign-entity TDS: it accounts for the vast majority of all TDS transactions reported through Form 27Q, since it functions as the catch-all provision for non-resident payments.

What is explicitly excluded:

TDS returns under Form 27Q do not include payments like dividends paid to NRIs, or interest income covered under the specific bond-related sections 194LB, 194LC, and 194LD, since those are reported under their own dedicated provisions rather than the general Section 195 umbrella.

What Are the TDS Rates Under Section 195?

Unlike domestic TDS sections, which typically apply flat percentage rates, Section 195 rates vary by the nature of the payment, and there are two rate systems running in parallel: the Finance Act rates and the DTAA rates.

Finance Act rates (base rates as per the Income Tax Act):

- Long-term capital gains on property (held over 24 months): 12.5% for FY 2025-26, following the Budget 2024 rate change effective 23 July 2024, which reduced this from the earlier 20%

- Short-term capital gains on property (held 24 months or less): taxed at the NRI’s applicable income tax slab rate

- Interest, royalty, and fees for technical services: rates vary depending on the specific nature and applicable provisions, generally in the range of 10% to 20%

- Any other income where no specific rate is prescribed: 20% as a general default under Chapter XVII-B, or higher in certain circumstances

Important on surcharge and cess:

Rates prescribed under the Finance Act must be increased by the applicable surcharge (where the payment or the payee’s income crosses relevant thresholds, such as ₹50 lakh or ₹1 crore) and a 4% health and education cess. If the payment amount is relatively small, surcharge may be nil, but the 4% cess is always mandatory regardless of amount.

DTAA rates:

If India has a Double Taxation Avoidance Agreement with the payee’s country of residence, and that treaty specifies a more favourable rate for the specific type of income, the NRI can opt for the DTAA rate instead of the Finance Act rate. Critically, surcharge and cess are not required to be added to DTAA rates, only to Finance Act rates. This makes the DTAA route often meaningfully cheaper even before comparing the base percentage.

No PAN available:

If the non-resident payee does not have a valid PAN, TDS must be deducted at the higher of the rate prescribed under Chapter XVII-B or 20%, under Section 206AA, regardless of what the DTAA might otherwise allow.

How Do DTAA Rates Actually Work in Practice?

To claim a DTAA rate instead of the standard Finance Act rate, the non-resident must provide the payer with a Tax Residency Certificate (TRC) issued by the tax authority of their country of residence, along with a Form 10F self-declaration (filed electronically on the Indian Income Tax e-filing portal) if the TRC does not already contain all the details the Indian rules require.

A worked example:

A person resident in Oman derives dividend income from an Indian company. Under the general provisions of the Income Tax Act, such a payment might attract TDS at 20% and be taxable at slab rates in India. However, under the India-Oman DTAA, a rate of 12.5% applies to dividend income. If the recipient furnishes a valid TRC to the paying company, the company can withhold tax at the lower 12.5% DTAA rate instead of 20%.

India has DTAA treaties with approximately 90 countries, and these treaties typically cover payments related to royalty, dividend, technical services, and interest, each with its own specified rate for that country.

What Is the “Grossing Up” Rule and Why Does It Matter?

This is one of the most commonly misunderstood aspects of Section 195 compliance, and getting it wrong leads to under-deduction.

If a contract specifies that the payer will bear the tax burden themselves (a “net of tax” arrangement, where the non-resident is guaranteed to receive a specific fixed amount regardless of TDS), the payment must be grossed up before TDS is calculated. This means the TDS is computed not on the contracted payment amount alone, but on a higher notional amount that, after TDS deduction, would still leave the non-resident with their originally agreed net amount.

A simplified illustration:

If a contract guarantees a foreign consultant a net payment of ₹9,00,000, and the applicable TDS rate is 10%, the payer cannot simply calculate TDS as 10% of ₹9,00,000. Instead, the payment must be grossed up so that after deducting TDS at 10% from the grossed-up figure, the consultant still receives exactly ₹9,00,000 net. This results in a higher TDS amount, and correspondingly a higher total cost to the payer, than a straightforward percentage calculation on the stated contract value would suggest.

Failing to gross up correctly in a “net of tax” contract results in under-deduction of TDS, which carries the same penalty exposure as any other TDS shortfall. This is a particularly important check for businesses negotiating fixed-fee contracts with foreign vendors or consultants.

What Information Does Form 27Q Contain?

Form 27Q is organised around three main components:

Voucher and transaction statistics:

The return categorises all transactions during the quarter into correctly recorded, inadequately recorded, and incorrectly recorded categories, helping the department and the deductor both track data quality issues before final submission.

Deductor and deductee details:

The PAN and TAN of the person making the payment, and the identifying details of the non-resident recipient. If the NRI’s PAN is not available, additional details must be furnished instead: their Tax Identification Number (TIN) from their home country, permanent address, country of residence, email, and contact details.

Payment and deduction details:

The nature of the payment (interest, royalty, technical fees, or other income excluding salary), the exact amount paid, the TDS rate applied (specifying whether it is the Finance Act rate or the DTAA rate), the amount of TDS deducted, and the challan details (BSR code, challan serial number, and date of deposit) through which the deducted tax was paid to the government.

If the non-resident has obtained a certificate under Section 197 permitting a lower or nil TDS deduction (discussed below), the specific certificate number must also be quoted in the return.

What Is Form 13 and How Does It Reduce TDS for the NRI?

A non-resident recipient can apply for a lower or nil TDS deduction certificate if they believe the payment they are due to receive is either not taxable in India, only partially taxable, or taxable at a rate lower than the standard withholding rate that would otherwise apply. To do this, the non-resident submits Form 13 to their jurisdictional Assessing Officer.

The Assessing Officer examines the application, verifies the underlying facts, and, if satisfied, issues a certificate under Section 197 permitting the payer to deduct tax at the lower or nil rate specified in that certificate, rather than the default statutory rate.

If such a certificate exists, the payer must quote the certificate number in Form 27Q when reporting that specific payment. This route is commonly used by NRIs selling property in India, where the standard TDS rate on the gross sale value (rather than just the capital gain) would otherwise result in significant excess tax being withheld, requiring the NRI to wait for a refund after filing their Indian tax return.

What Are the Due Dates for Form 27Q for FY 2025-26?

| Quarter | Period | Due Date |

| Q1 | April to June 2025 | 31 July 2025 |

| Q2 | July to September 2025 | 31 October 2025 |

| Q3 | October to December 2025 | 31 January 2026 |

| Q4 | January to March 2026 | 31 May 2026 |

These dates match the standard quarterly schedule that also applies to Form 24Q and Form 26Q. The underlying TDS deposit deadline follows the same monthly pattern: the 7th of the following month for most deductions, extending to 30 April for TDS deducted in March.

After filing Form 27Q, the payer must issue Form 16A (the TDS certificate) to the non-resident within 15 days of the due date for filing that quarter’s return.

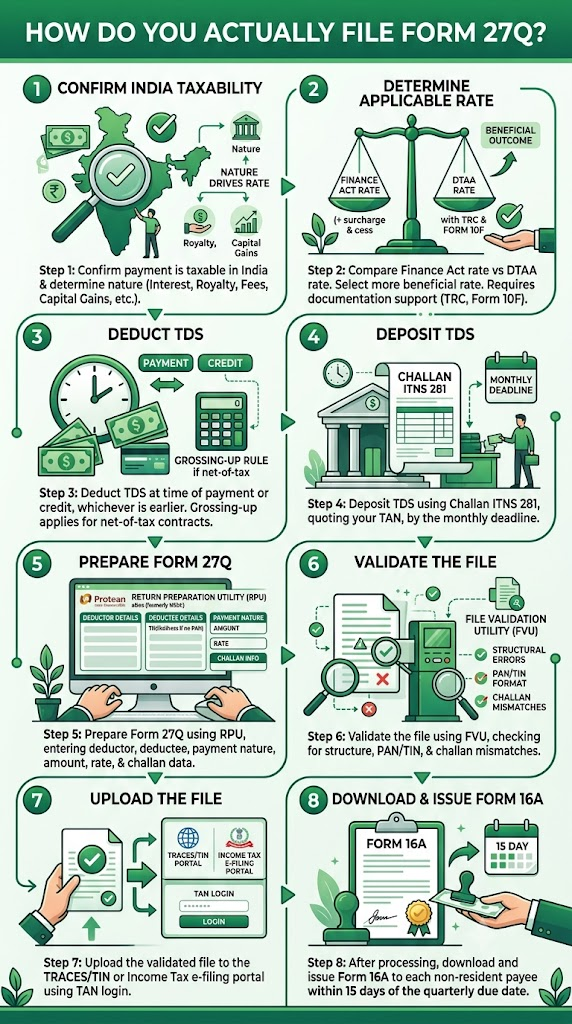

How Do You Actually File Form 27Q?

- Step 1: Confirm the payment is taxable in India and determine its nature (interest, royalty, technical fees, capital gains, or other income), since this classification drives the applicable rate.

- Step 2: Determine the applicable rate, comparing the Finance Act rate (plus surcharge and cess) against any available DTAA rate (with TRC and Form 10F on file), and select whichever is more beneficial to the non-resident, provided the required documentation supports the DTAA claim.

- Step 3: Deduct TDS at the time of payment or credit to the payee’s account, whichever is earlier, applying the grossing-up rule if the contract is structured on a net-of-tax basis.

- Step 4: Deposit the TDS using Challan ITNS 281, quoting your TAN, by the applicable monthly deadline.

- Step 5: Prepare Form 27Q using the Return Preparation Utility (RPU) from Protean eGov (formerly NSDL), entering deductor details, deductee details (including TIN and address details if PAN is unavailable), payment nature, amount, applicable rate, and challan information.

- Step 6: Validate the file using the File Validation Utility (FVU), checking for structural errors, PAN/TIN format issues, and challan mismatches.

- Step 7: Upload the validated file to the TRACES/TIN portal or the Income Tax e-filing portal using your TAN login.

- Step 8: After processing, download and issue Form 16A to each non-resident payee within 15 days of the quarterly due date.

Does Buying Property From an NRI Use Form 27Q or Form 26QB?

This is a common point of confusion for anyone buying real estate in India, because the process looks similar on the surface but is structurally different depending on the seller’s residency status.

If you buy a property from a resident Indian seller, TDS under Section 194-IA applies, and you use Form 26QB, a simplified PAN-based challan-cum-statement that does not require a TAN.

If you buy a property from an NRI seller, the entire framework changes: TDS falls under Section 195, not Section 194-IA. You must obtain a TAN, and you must file the quarterly Form 27Q, not Form 26QB. The TDS rate is also different and generally higher: instead of the flat 1% that applies to resident sellers under Section 194-IA, NRI property sales attract TDS based on the nature of the gain, 12.5% on long-term capital gains (after Budget 2024) or slab rates on short-term gains, and this is calculated on the capital gain amount in principle, though in practice many buyers deduct on the full sale consideration unless the NRI has obtained a Section 197 lower-deduction certificate specifying the actual gain-based figure.

For more on the resident-seller version of this transaction, see our Form 26QB guide.

How Does Form 27Q Connect to Form 15CA and Form 15CB?

If the payment to the non-resident is also being remitted out of India (for example, wiring the sale proceeds of a property back to an NRI’s overseas account, or paying a foreign vendor via international bank transfer), a separate compliance layer applies on top of the Form 27Q TDS reporting: Form 15CA and, where the remittance exceeds ₹5 lakh, Form 15CB certified by a Chartered Accountant.

Form 27Q reports the TDS deduction itself to the Income Tax Department on a quarterly basis. Form 15CA and Form 15CB are separately required at the time of the actual remittance, confirming to the bank handling the transfer that the appropriate tax position has been assessed and, where applicable, TDS has been correctly deducted. These are related but distinct compliance obligations, and a foreign remittance connected to a Section 195 payment will typically require both. For a complete breakdown of this separate compliance layer, see our guides on Form 15CA and Form 15CB.

What Is New for FY 2025-26: Section 194T for Non-Resident Partners

Similar to the update covered in our Form 26Q guide, Form 27Q has also been revised to incorporate the new Section 194T, which covers payments made to non-resident partners of a firm (salary, remuneration, bonus, commission, or interest on capital). The updated form includes a specific new entry for Section 194T alongside the existing, dominant Section 195 provisions. If your partnership firm has non-resident partners receiving such payments, this new requirement applies from FY 2025-26 onward and should be reviewed with your CA.

What Penalties Apply for Non-Compliance?

The consequences for Section 195 non-compliance are structured similarly to other TDS provisions, with one additional business-specific consequence worth flagging separately.

Expense disallowance:

If TDS is not withheld or deposited within the prescribed time on a payment that is otherwise a deductible business expense, that expense will be disallowed for the year in which it should have been deducted, and will only become allowable in the year the TDS default is actually corrected. This can materially affect a business’s taxable profit computation for the year of the original payment.

Interest for late deduction:

1% per month from the date TDS was deductible to the date it is actually deducted, under Section 201(1A).

Interest for late deposit:

1.5% per month from the date of deduction to the date of actual deposit, if TDS is deducted but not paid to the government within the due date.

Penalty under Section 271C:

May be levied equal to the amount of TDS that was not deducted or paid at all.

Penalty for short deduction:

In cases where TDS was deducted but at a lower rate than required (for example, applying a DTAA rate without valid TRC documentation), a penalty may be levied equal to the amount of the shortfall.

Beyond the direct financial penalties, delays or errors in Form 27Q filing can also cause real practical difficulties for the NRI recipient: since the deducted TDS only appears in the non-resident’s Form 26AS and AIS once the return is filed and processed, a missed or delayed filing can hold up their ability to claim TDS credit or seek a refund when filing their own Indian tax return.

Important: Form 27Q Is Becoming Form 144

Under the Income Tax Act, 2025 (effective from 1 April 2026) and the Income Tax Rules, 2026, Form 27Q is being renamed Form 144. As with the broader TDS restructuring covered in our Form 26Q guide, the underlying Section 195 provision is being consolidated into the new Section 393(2) of the Income Tax Act, 2025, alongside the retirement of the old 194-series and 195 section references in favour of numeric payment codes.

From Q1 of Tax Year 2026-27, Form 27Q filings must reference the new section numbers and payment codes; the CPC (Centralised Processing Centre) will reject filings that continue to use old section codes for transactions dated on or after 1 April 2026. Form 16A, the certificate generated from these filings, also becomes Form 131 under the new framework, matching the renumbering applied to the resident-payment TDS certificate.

For FY 2025-26 (payments made up to 31 March 2026):

Continue using Form 27Q and Section 195 references exactly as described in this article.

For Tax Year 2026-27 (payments made from 1 April 2026 onwards):

Use Form 144, referencing Section 393(2) and the corresponding new payment codes. Update your TDS software and internal compliance checklists ahead of your first quarterly filing under the new framework.

Frequently Asked Questions

1. Is there a minimum payment amount below which TDS under Section 195 does not apply?

No. Unlike many resident-payment TDS sections that carry specific exemption thresholds, Section 195 applies from the first rupee of taxable income paid to a non-resident, provided that income is chargeable to tax in India.

2. I am buying a flat from an NRI. Can I use Form 26QB like I would for a resident seller?

No. Property purchases from NRI sellers fall under Section 195, not Section 194-IA. You must obtain a TAN and file the quarterly Form 27Q, not Form 26QB, and the applicable TDS rate structure is also different from the flat 1% used for resident sellers.

3. Do I need to add surcharge and cess to the DTAA rate?

No. Surcharge and the 4% health and education cess apply only to rates prescribed under the Finance Act. If a DTAA rate is being applied instead (with valid TRC and Form 10F documentation), no surcharge or cess is added on top of that treaty rate.

4. What happens if the NRI does not have a PAN?

If the payee does not furnish a valid PAN, TDS must be deducted at the higher of the rate prescribed under Chapter XVII-B or 20%, under Section 206AA, regardless of any lower DTAA rate that might otherwise apply. In this scenario, additional identifying details (TIN, address, country of residence) must be furnished in Form 27Q instead of a PAN.

5. Can the TDS rate be reduced if the NRI’s actual tax liability is lower than the standard withholding rate?

Yes, through a Section 197 lower or nil deduction certificate. The NRI applies using Form 13 to their Assessing Officer, and if approved, the payer deducts TDS at the reduced rate specified in that certificate, quoting the certificate number in Form 27Q.

6. What is the “grossing up” rule and when does it apply?

It applies when a contract guarantees the non-resident a fixed net amount, with the payer bearing the TDS burden. In such cases, TDS must be calculated on a higher, grossed-up figure so that the non-resident’s guaranteed net amount is preserved after deduction, rather than calculating TDS as a straightforward percentage of the stated contract value.

7. Is Form 27Q connected to Form 15CA and Form 15CB?

They are related but separate requirements. Form 27Q is the quarterly TDS return reporting the deduction to the Income Tax Department. Form 15CA (and Form 15CB, where the remittance exceeds ₹5 lakh) is required separately at the time of the actual outward remittance, and is what your bank will ask for before processing the transfer.

Key Takeaways

- Form 27Q is the quarterly TDS return for non-salary payments to non-residents and foreign companies, filed under Section 195 of the Income Tax Act, and requires the payer to hold a valid TAN.

- There is no minimum threshold; Section 195 TDS applies from the first rupee of taxable income paid to a non-resident.

- TDS can be deducted at either the Finance Act rate (plus surcharge and 4% cess) or the DTAA rate (no surcharge or cess added), whichever is more beneficial, provided the non-resident furnishes a valid TRC and Form 10F.

- Property purchases from NRI sellers use Form 27Q, not Form 26QB, and require a TAN, unlike purchases from resident sellers.

- The grossing up rule applies to net-of-tax contracts and results in a higher effective TDS deduction than a simple percentage calculation on the stated contract value.

- FY 2025-26 due dates: Q1: 31 July 2025, Q2: 31 October 2025, Q3: 31 January 2026, Q4: 31 May 2026, with Form 16A due to the payee within 15 days of each quarterly deadline.

- New for FY 2025-26: Form 27Q now also captures Section 194T payments to non-resident partners.

- Form 27Q compliance connects to a separate Form 15CA/15CB requirement whenever the payment is also being remitted abroad.

- From Tax Year 2026-27, Form 27Q is replaced by Form 144, referencing the new Section 393(2) of the Income Tax Act, 2025.

Sources: Motilal Oswal: Form 27Q, TDS Return for NRI Payments; Tax2win: Form 27Q, TDS Return for NRI Payments, Due Dates, April 2026; Tax Garden: TDS on Payments to Non-Residents, Section 195/393 Complete Guide for FY 2026-27; IndiaFilings: Form 27Q Filing for NRI TDS Return, Detailed Guide, June 2026.

This article is for general information only and does not constitute tax or professional advice. For guidance specific to a cross-border payment, consult a practising Chartered Accountant experienced in international taxation.