Quick summary: Most people are familiar with TDS, tax deducted at source by whoever pays them. Far fewer understand its mirror image, TCS, tax collected at source by whoever sells to them. If your business sells alcohol, scrap, timber, high-value motor vehicles, or specified minerals, or if you are an authorised dealer processing foreign remittances under the Liberalised Remittance Scheme, you may be legally required to collect TCS from your buyer and report it quarterly through Form 27EQ. This guide explains exactly what falls under Section 206C, the current TCS rates, how Form 27EQ differs from the TDS return forms covered elsewhere in this series, and the significant restructuring taking effect from April 2026.

What Is TCS, and How Is It Different From TDS?

Tax Collected at Source (TCS) is tax that a seller collects from a buyer at the time of receiving payment for specified goods or transactions, and then deposits with the government. This is the reverse mechanism of TDS: with TDS, the person making a payment deducts tax before paying the recipient; with TCS, the person receiving payment (the seller) adds tax on top of the sale price and collects it from the person paying (the buyer).

A simple worked example:

Mr. A sells goods worth ₹1,00,000 to Mr. B, and TCS applies at 1%. Mr. A collects ₹1,01,000 from Mr. B (the ₹1,00,000 sale price plus 1% TCS of ₹1,000). Mr. A is responsible only for collecting this tax and depositing it with the government; he is not responsible for paying it out of his own pocket, since the buyer bears the actual cost of the TCS.

TCS is governed by Section 206C of the Income Tax Act, 1961, and its purpose is to widen the tax base and create a documented paper trail in specific categories of high-risk or high-value trade, particularly transactions where buyers (especially firms or associations of persons) have historically been difficult for the tax department to trace after the fact.

What Is Form 27EQ?

Form 27EQ is the quarterly statement that a TCS collector must file, reporting the tax collected at source during that quarter and confirming that it has been deposited with the Central Government. It falls under Section 206C and, like the TDS return forms covered elsewhere in this series, requires the collector to hold a valid TAN (Tax Deduction and Collection Account Number, the same identifier used for TDS purposes).

Both government and non-government collectors must file this form. Non-government collectors must quote their PAN in the return; government collectors quote “PANNOTREQD” instead, following the same convention used across Form 24Q, Form 26Q, and Form 27Q, all covered in our earlier articles in this series.

The details reported in Form 27EQ flow directly into the buyer’s Form 26AS and Annual Information Statement, allowing the buyer to claim credit for the TCS collected from them, just like TDS credit, when they file their own income tax return.

Who Is Required to Collect TCS and File Form 27EQ?

Any individual, company, government department, firm, or other entity that collects tax at source on a specified transaction under Section 206C is required to file Form 27EQ. In practice, this most commonly applies to sellers, traders, manufacturers, and authorised dealers dealing in the specific categories of goods and transactions listed below.

What Transactions and Goods Actually Attract TCS?

Section 206C applies to a defined, specific list of transactions, not to general sales of goods broadly. Here are the current categories and rates, reflecting the Finance Act 2025 changes effective from 1 April 2025:

| Category | TCS Rate | Threshold |

| Alcoholic liquor for human consumption | 1% | On the full sale value |

| Tendu leaves | 5% | On the full sale value |

| Timber obtained under a forest lease | 2.5% | On the full sale value |

| Timber obtained by any mode other than forest lease | 2.5% | On the full sale value |

| Any other forest produce (not timber or tendu leaves) | 2.5% | On the full sale value |

| Scrap | 1% | On the full sale value |

| Minerals (coal, lignite, iron ore) | 1% | On the full sale value |

| Parking lot, toll plaza, or mining and quarrying lease/licence | 2% | On the full sale value |

| Sale of motor vehicles (including luxury goods notified by CBDT) | 1% | Value exceeding ₹10 lakh per vehicle |

| Overseas tour package under LRS | 5% (reduced to 2% for FY 2025-26 as proposed) | On the full package value, subject to applicable threshold |

| LRS remittances for education (loan-funded) | Nil | N/A |

| LRS remittances for education (self-funded) or medical treatment | 5% (reduced to 2% as proposed) | On amount exceeding ₹7 lakh |

| LRS remittances for other purposes | 20% | On amount exceeding ₹7 lakh |

Important note on rates:

TCS rates are revised periodically through Finance Acts, and the table above reflects rates applicable for FY 2025-26. Some sources report a further increase in the scrap TCS rate from 1% to 2% and similar adjustments effective from 1 April 2026 under the new tax framework discussed later in this article. Always verify the current rate applicable to your specific transaction date, since a rate change mid-year (as has happened with several of these categories in recent years) directly affects how much TCS you must collect and report.

If the buyer does not furnish PAN or Aadhaar:

TCS must be collected at a higher rate, generally 5% or twice the prescribed rate, whichever is higher, under the higher-rate provisions built into Section 206C.

What About Section 206C(1H): TCS on Sale of Goods Above ₹50 Lakh?

This provision, introduced by the Finance Act 2020, requires sellers with turnover exceeding ₹10 crore in the preceding financial year to collect TCS when receiving more than ₹50 lakh from a single buyer in a financial year, for the sale of goods generally (not limited to the specific categories listed in the table above). This became one of the broadest TCS provisions in practice, since it potentially captured any large seller-buyer relationship crossing the threshold, rather than being limited to niche categories like liquor or timber.

Exclusions from Section 206C(1H)

Include exports, imports, goods already covered under the specific categories in Sections 206C(1), 206C(1F), or 206C(1G) (to avoid double TCS on the same transaction), transactions where the buyer is already subject to TDS on the same purchase, and government entities, embassies, and foreign trade representations.

A significant structural change:

This specific provision, Section 206C(1H), has been permanently omitted and is not carried forward into the new Income Tax Act, 2025. This is a meaningful simplification for businesses that had to track this broad, general provision alongside their more specific TCS obligations.

What Is Form 27D and How Does It Relate to Form 27EQ?

Once a collector files Form 27EQ for a quarter, they must issue a TCS certificate, Form 27D, to each buyer (referred to as the “collectee” in the statutory language) whose tax was collected and reported in that quarter. This is the exact mirror of how Form 16A works for TDS: the return (Form 27EQ) is filed with the government first, and the certificate (Form 27D) is then generated and issued to the person from whom tax was collected, as proof they can use to claim credit in their own tax filing.

Timing: Form 27D must be issued to the buyer within 15 days from the date of filing the corresponding quarterly Form 27EQ.

What Are the Due Dates for Form 27EQ and the Underlying TCS Deposit?

| Quarter | Period | Form 27EQ Due Date |

| Q1 | April to June | 15 July |

| Q2 | July to September | 15 October |

| Q3 | October to December | 15 January |

| Q4 | January to March | 15 May |

Notice that Form 27EQ’s due dates (the 15th of the month following quarter-end, except for Q4) are slightly different from the pattern used by Form 24Q, Form 26Q, and Form 27Q, which are generally due by month-end. Do not assume the same calendar applies across all your TDS and TCS filings; check each form’s specific due date separately.

The underlying TCS deposit deadline is monthly, separate from the quarterly return: TCS collected during a month must be deposited by the 7th of the following month, except for TCS collected in March, which must be deposited by 30 April. Payment of TCS should always be completed before filing the corresponding quarterly Form 27EQ; the return effectively reports on deposits that should already have been made.

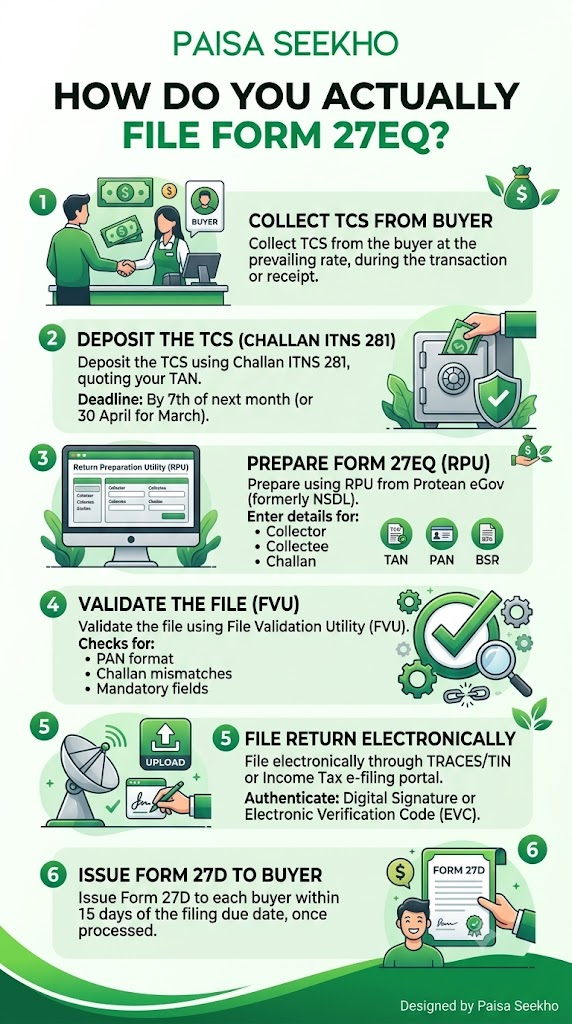

How Do You Actually File Form 27EQ?

The filing process closely parallels the TDS return process covered in our earlier articles on Form 24Q, Form 26Q, and Form 27Q, since all of these returns share the same underlying utility and portal infrastructure.

- Step 1: Collect TCS from the buyer at the prevailing rate, at the time of the transaction or receipt of payment, as applicable to the specific category.

- Step 2: Deposit the TCS using Challan ITNS 281, quoting your TAN, by the 7th of the following month (or 30 April for March collections).

- Step 3: Prepare Form 27EQ using the Return Preparation Utility (RPU) from Protean eGov (formerly NSDL), entering collector details (TAN, PAN or “PANNOTREQD” for government collectors), collectee details (PAN, name, amount, applicable section, and rate), and challan details (BSR code, deposit date, and amount).

- Step 4: Validate the file using the File Validation Utility (FVU), checking for PAN format issues, challan mismatches, and missing mandatory fields.

- Step 5: File the return electronically, signing it digitally or authenticating it using an Electronic Verification Code (EVC), through the TRACES/TIN portal or the Income Tax e-filing portal.

- Step 6: Issue Form 27D to each buyer within 15 days of the filing due date, once the return is processed.

What Penalties Apply for Non-Compliance?

The penalty structure for Form 27EQ mirrors the TDS return penalty framework covered elsewhere in this series, with the same core provisions applying to TCS instead of TDS.

Interest for failure to collect TCS on time:

1% per month, or part of a month, from the date the tax should have been collected to the date it is actually collected.

Interest for late deposit of collected TCS:

1% per month from the date of collection to the date of actual deposit with the government.

Late filing fee (Section 234E):

₹200 per day of delay in filing Form 27EQ, from the due date until the actual filing date, capped at the total TCS amount for that quarter. This fee is mandatory and cannot be waived by any authority, including the Assessing Officer, and must be paid via challan before the return can even be submitted on the portal.

Discretionary penalty (Section 271H):

An additional penalty of ₹10,000 to ₹1,00,000 may be levied for furnishing incorrect information or for prolonged non-filing beyond the standard late fee, at the discretion of the Assessing Officer.

Disallowance consequence:

Interest and penalties arising from a TCS default are not allowable as a business expense when computing the collector’s own taxable income, meaning this cost cannot be used to reduce the collector’s tax liability, unlike many ordinary business expenses.

Form 27EQ vs Form 24Q, Form 26Q, and Form 27Q: What Is the Difference?

| Form 27EQ | Form 24Q | Form 26Q | Form 27Q | |

| What it covers | Tax collected at source (TCS) on specified goods and transactions | Tax deducted at source on salary | Tax deducted at source on non-salary payments to residents | Tax deducted at source on payments to non-residents |

| Governing section | Section 206C | Section 192 | Various sections in the 194-series | Section 195 |

| Who files | Sellers of specified goods, authorised dealers processing LRS remittances | Employers | Any deductor making qualifying non-salary payments to residents | Any payer making qualifying payments to non-residents |

| Certificate issued | Form 27D | Form 16 | Form 16A | Form 16A (with non-resident-specific fields) |

| Standard due dates | 15th of the month after quarter-end (except Q4: 15 May) | Month-end (varies by quarter) | Month-end (varies by quarter) | Month-end (varies by quarter) |

For details on the other three forms, see our guides on Form 24Q for TDS on salary, Form 26Q for non-salary TDS, and Form 27Q for NRI payments.

Important: Form 27EQ Is Becoming Form 143

Under the Income Tax Act, 2025 (effective from 1 April 2026) and the accompanying Finance Act 2026 amendments, Form 27EQ is being renamed Form No. 143, and the underlying provision shifts from Section 206C of the old Act to Section 394 of the new Act.

Several substantive changes accompany this restructuring:

- Alcoholic liquor TCS rate increased from 1% to 2%

- Tendu leaves TCS rate reduced from 5% to 2%

- Scrap TCS rate increased from 1% to 2%

- Minerals (coal, lignite, iron ore) TCS rate increased from 1% to 2%

- LRS remittances for education or medical treatment: TCS rate reduced to 2% on the amount exceeding ₹10 lakh (up from the earlier ₹7 lakh threshold), with a continued nil rate where the remittance is funded through an education loan

- Overseas tour packages: a uniform 2% TCS rate, with no differing slabs based on package value

- Section 206C(1H) (TCS on general sale of goods above ₹50 lakh) is permanently omitted and does not appear in the new Act

- Sections 206AB and 206CCA (which required higher TDS/TCS rates for non-filers of income tax returns) are not reproduced in the new Act, meaning collectors and deductors will no longer need to check a payee’s ITR filing status to determine whether a higher rate applies

- A new time limit for correction statements: 2 years from the end of the relevant tax year

- Lower or nil TCS collection certificates continue to be available, now under Section 395(3) of the new Act

For FY 2025-26 (transactions up to 31 March 2026): continue using Form 27EQ, Section 206C, and the rates described earlier in this article.

For Tax Year 2026-27 (transactions from 1 April 2026 onwards): use Form 143, referencing Section 394 and the updated rates and thresholds outlined above.

Frequently Asked Questions

1. What is the basic difference between TDS and TCS?

TDS is deducted by the person making a payment (for example, an employer deducting tax from salary, or a company deducting tax from a contractor’s invoice). TCS is collected by the person receiving a payment, specifically the seller of certain specified goods or the provider of certain specified transactions, from the buyer. Form 27EQ reports TCS; Forms 24Q, 26Q, and 27Q report various categories of TDS.

2. Do I need a TAN to file Form 27EQ?

Yes. Filing Form 27EQ requires the collector to hold a valid TAN, the same identifier used for TDS compliance under Section 203A.

3. My business sells scrap. Do I need to collect TCS on every sale?

If your business sells scrap and the transaction falls within the categories specified under Section 206C, TCS applies at the prescribed rate on the sale value. Unlike the now-omitted Section 206C(1H), which had a ₹50 lakh threshold for general goods, TCS on scrap under the specific Section 206C category generally applies without a similar high-value threshold, so check the applicable provision carefully with your CA.

4. Can the buyer claim credit for TCS collected from them?

Yes. Once the collector files Form 27EQ, the TCS details appear in the buyer’s Form 26AS and Annual Information Statement, and the buyer can claim credit for this amount, just like TDS credit, when filing their own income tax return.

5. Is TCS on foreign remittances under LRS the same as TCS on sale of goods?

They fall under the same overarching Section 206C framework and are both reported through Form 27EQ, but they are distinct sub-categories with their own specific rates and thresholds. LRS remittance TCS is collected by authorised dealers (typically banks) processing the outward remittance, not by a goods seller.

6. What happens if a Section 206C(1H) transaction occurred in FY 2025-26 but the corresponding Form 27EQ is filed after 1 April 2026?

The transaction itself, having occurred before 31 March 2026, remains governed by the old Income Tax Act, 1961 and Section 206C(1H), even if the actual filing happens slightly after the new Act comes into force. The provision’s omission from the new Act only affects transactions occurring from 1 April 2026 onwards; it does not retroactively remove the obligation for earlier transactions.

7. What replaces Form 27EQ from April 2026?

Form 143, under the Income Tax Act, 2025 and the Finance Act 2026, referencing Section 394 instead of the old Section 206C. Several TCS rates change simultaneously, and two provisions widely used for compliance checks, Section 206C(1H) and Sections 206AB/206CCA, are not carried forward into the new framework.

Key Takeaways

- Form 27EQ is the quarterly TCS return filed under Section 206C by sellers and authorised dealers who collect Tax Collected at Source on specified goods (liquor, scrap, timber, minerals) and transactions (motor vehicle sales above ₹10 lakh, LRS remittances).

- TCS is collected by the seller from the buyer, the reverse mechanism of TDS, and the seller is responsible only for collecting and depositing it, not for bearing the cost.

- A valid TAN is required to file Form 27EQ.

- Due dates follow a distinct pattern from the other TDS return forms: 15 July, 15 October, 15 January, and 15 May (Q4), rather than the month-end pattern used by Forms 24Q, 26Q, and 27Q.

- After filing, collectors must issue Form 27D to each buyer within 15 days of the filing due date.

- Penalties mirror the standard TDS framework: ₹200/day under Section 234E (mandatory, capped at the TCS amount), interest for late collection and deposit, and a discretionary ₹10,000 to ₹1,00,000 penalty under Section 271H.

- From Tax Year 2026-27, Form 27EQ is replaced by Form 143 under Section 394 of the Income Tax Act, 2025, alongside several rate changes and the permanent omission of Section 206C(1H) (general sale of goods TCS) and Sections 206AB/206CCA (higher rates for ITR non-filers).

Sources: Taxguru: TCS Return Form 27EQ, Due Dates, Challan and Penalties, July 2025; ClearTax: Tax Collected at Source (TCS), Rates, Payment and Exemption, May 2026; DisyTax: TCS Explained, Applicability, Collection Process, and Due Dates, April 2026; Eztax: TCS on Receipts, Form 143 (aka Form 27EQ) Filing, April 2026.

This article is for general information only and does not constitute tax or professional advice. For guidance specific to your TCS compliance, consult a practising Chartered Accountant.