Quick summary: If you received salary arrears, advance salary, gratuity, or pension money that belongs to past years but landed in your bank account this year, you may end up paying extra tax just because all that money got “bunched up” in one year. Section 89(1) of the Income Tax Act lets you fix this. But you can only claim this relief if you file Form 10E online, before you file your Income Tax Return (ITR). Skipping this step means the Income Tax Department will reject your claim, even if you mention it in your ITR.

This guide explains what Form 10E is, who needs it, how the relief is calculated, and how to file it step by step.

What Is Section 89(1) of the Income Tax Act?

Income tax in India is calculated using slabs, the more you earn in a year, the higher the tax rate on the additional income. This works fine when your income is steady. But problems start when you suddenly receive a large chunk of money that actually belongs to an earlier year.

For example, imagine your company revised your salary in 2024, but the increased pay (the difference, called arrears) was only credited to your account in 2026. That arrear amount gets added to your current year’s income. Since your current year’s income is now higher, you might get pushed into a higher tax slab and end up paying more tax than you would have if you had received that money on time, in the year it was actually due.

Section 89(1) exists to prevent this unfair situation. It allows the government to recalculate your tax as if you had received the money in the year it was originally due, and gives you relief (a reduction) equal to the extra tax you paid only because of the timing of the payment.

This relief applies to:

- Salary or family pension received in arrears or in advance

- Gratuity for past service

- Compensation received on termination of employment

- Commuted pension (a lump sum you get instead of monthly pension payments)

What Is Form 10E?

Form 10E is the official form you must submit on the Income Tax Department’s e-filing portal to formally claim relief under Section 89(1). It is not optional paperwork, it’s the only way the tax department recognises your claim.

A few important points about Form 10E, straight from the Income Tax Department’s own guidance:

- It can be filed online only, there is no offline or paper version.

- It is mandatory to file Form 10E before you claim relief under Section 89 in your ITR.

- All registered individual users on the e-filing portal can file it, as long as their PAN status is “Active.”

- If you claim Section 89 relief in your ITR without filing Form 10E first, your ITR will still be processed, but the relief you claimed will be disallowed, and you may also get a notice from the department asking why you claimed something you weren’t entitled to.

Why Is Filing Form 10E Mandatory?

Many salaried employees assume that since their employer has already adjusted TDS (Tax Deducted at Source) for the arrears, they don’t need to do anything extra. This is a costly mistake.

The relief under Section 89(1) is a claim you make to the tax department, not something your employer can finalise on your behalf. The department needs your detailed calculations (covered in Form 10E) showing exactly how much extra tax you paid because of bunching, and for which earlier years the arrears belong to. Without this form, the system has no record to validate your claim, so it gets rejected automatically.

Who Should File Form 10E?

You should consider filing Form 10E if, in the current financial year, you received any of the following:

| Type of receipt | Example |

| Salary arrears | A pay revision from an earlier year, credited now |

| Advance salary | Salary for a future period paid early |

| Family pension arrears | Pending pension payments cleared in a lump sum |

| Gratuity | A lump sum on leaving a job after long service |

| Compensation on termination | A severance payout after losing your job |

| Commuted pension | A one-time lump sum instead of monthly pension |

Not everyone who receives such payments actually needs to file Form 10E. You should only claim relief if your total tax liability for the year actually increased because of the lump sum payment. If, after calculation, there’s no extra tax burden, there’s nothing to claim, and filing for relief you’re not eligible for can attract scrutiny.

How Is Relief Under Section 89(1) Calculated?

The calculation method is laid down under Rule 21A of the Income Tax Rules. It sounds complicated on paper, but it really boils down to comparing “tax with arrears” versus “tax without arrears,” in both the year you received the money and the year(s) it was actually due. Here’s the simplified version:

- Step 1: Calculate the tax payable on your total income for the current year, including the arrears. Call this A.

- Step 2: Calculate the tax payable on your total income for the current year, excluding the arrears. Call this B.

- Step 3: Find the difference: A − B. This is the extra tax you’re paying this year because of the arrears.

- Step 4: Now go back to the earlier year(s) the arrears actually belong to. Calculate the tax payable on that year’s income including the arrear amount that belongs to that year. Call this C.

- Step 5: Calculate the tax payable on that same earlier year’s income, excluding the arrear amount. Call this D.

- Step 6: Find the difference: C − D. This is what the extra tax would have been if you’d received the money on time.

- Step 7: Your relief = (A − B) − (C − D). If this number is positive, that’s the amount of relief you can claim. If it’s zero or negative, you’re not eligible for any relief.

A simple example

Say Aditi received ₹1,20,000 as salary arrears in FY 2025-26, which actually belonged to FY 2023-24.

- Tax on her FY 2025-26 income with the arrears = ₹1,85,000 (A)

- Tax on her FY 2025-26 income without the arrears = ₹1,60,000 (B)

- Extra tax this year because of arrears = A − B = ₹25,000

- Tax on her FY 2023-24 income if the arrears had been included that year = ₹95,000 (C)

- Tax on her FY 2023-24 income as originally filed (without arrears) = ₹80,000 (D)

- Extra tax she would have paid that year = C − D = ₹15,000

- Relief = (A − B) − (C − D) = ₹25,000 − ₹15,000 = ₹10,000

Aditi can claim ₹10,000 as relief under Section 89(1) by filing Form 10E. (Note: this is a simplified illustration to explain the concept, your own numbers will depend on actual slab rates for each relevant year.)

You don’t have to do this calculation manually. The e-filing portal’s Form 10E auto-calculates the relief once you enter your income figures for the relevant years, based on the annexure you select.

Documents You’ll Need Before Filing

Keep these ready before you start filing, so the process goes smoothly:

- Form 16 for the current financial year and the earlier year(s) the arrears relate to

- Salary slips or arrear payment statement from your employer (showing how much belongs to which year)

- Copies of ITRs filed for the earlier relevant years (if available)

- PAN and login credentials for the e-filing portal

- Details of any other income or deductions for the relevant years, if your tax computation needs them

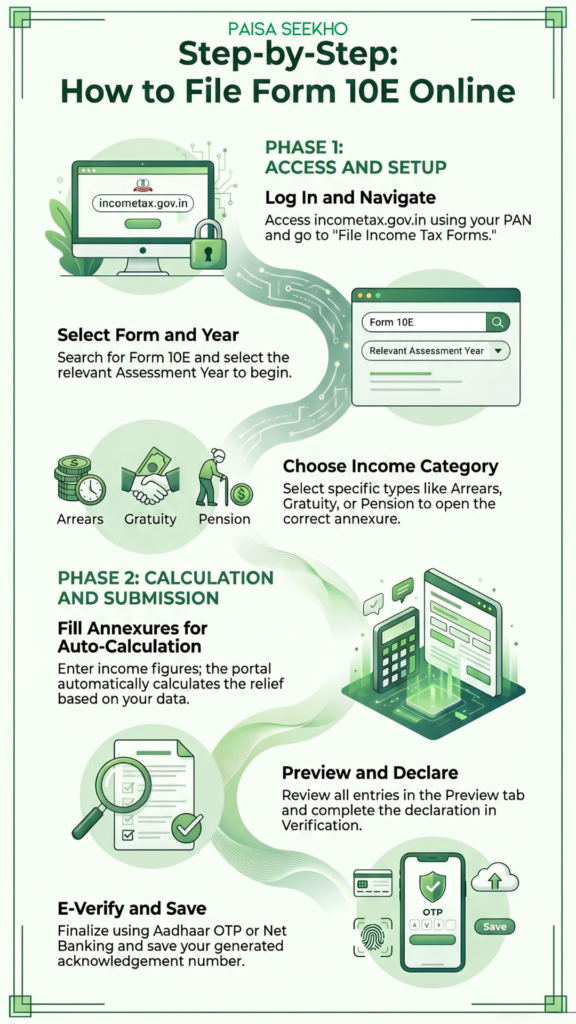

Step-by-Step: How to File Form 10E Online

Form 10E can only be filed through the official Income Tax Department e-filing portal at incometax.gov.in. Here’s the process:

- Log in to the e-filing portal using your PAN as the User ID and your password.

- Go to e-File → Income Tax Forms → File Income Tax Forms.

- Search for and select Form 10E.

- Choose the relevant Assessment Year and click Continue, then click “Let’s Get Started.”

- Select the type(s) of income you’re claiming relief for, Arrears Salary, Advance Salary, Gratuity, Compensation on Termination, or Commutation of Pension, based on what you actually received. Each has its own annexure (Annexure I, II/IIA, III, or IV).

- Confirm your personal information tab (make sure your residential status and contact details are updated under “My Profile”).

- Fill in the details under each applicable annexure, this includes entering your income figures for the current year and the earlier year(s) the arrears relate to. The portal calculates the relief automatically.

- Once all applicable sections are filled and saved, go to the Verification tab, tick the declaration checkbox, enter your place, and save.

- Click Preview to review everything. If it looks correct, proceed to e-Verify.

- Complete e-verification using Aadhaar OTP, net banking, or another available mode.

- Once verified, an acknowledgement number is generated and sent to your registered email and mobile number. Keep this safe.

After this, you can go ahead and claim the Section 89(1) relief while filing your ITR.

Important: Form 10E Is Becoming Form 39

Here’s something to keep in mind if you’re filing for a more recent period. India’s tax law is changing, the Income Tax Act, 2025 has replaced the older Income Tax Act, 1961, effective from 1 April 2026. Under the new Act, the same relief (now under Section 157 instead of Section 89) will be claimed using a new form called Form 39, not Form 10E.

However, this transition doesn’t affect most people filing right now. As clarified by the Income Tax Department: for Assessment Year 2026-27 (covering income earned in FY 2025-26), your return is still governed by the old Income Tax Act, 1961, so you must continue using Form 10E, not Form 39. Form 39 will only apply from Tax Year 2026-27 onwards (income earned from April 2026), for returns that will be filed in 2027.

In short: if you’re filing your ITR for AY 2026-27 (due by 31 July 2026 for most salaried taxpayers, as notified by the CBDT), use Form 10E as described above.

Does the Old or New Tax Regime Matter?

No, you can claim relief under Section 89(1) by filing Form 10E whether you’re under the old tax regime or the new tax regime. The relief itself isn’t tied to which regime you choose; it simply corrects the unfair tax impact of receiving past income in a lump sum.

Common Mistakes to Avoid

- Filing Form 10E after the ITR, or not at all. It must be filed before you submit your return. Filing it late or skipping it altogether leads to the relief being denied.

- Claiming relief without checking eligibility. Run the calculation first, if there’s no extra tax burden from the bunching, there’s no relief to claim.

- Mixing up assessment years. Make sure you select the correct AY when filing, matching the year in which you actually received the arrears (not the year they relate to).

- Not keeping past Form 16s and ITRs handy. You’ll need income details from earlier years to complete the relevant annexures accurately.

- Forgetting to e-verify. An unverified Form 10E is treated as not filed.

Frequently Asked Questions

1. Is it mandatory to file Form 10E to claim relief under Section 89(1)?

Yes. The Income Tax Department has made it mandatory. Even if your employer has factored in the relief while calculating TDS, you must still file Form 10E and claim the relief yourself in your ITR.

2. What happens if I claim Section 89 relief in my ITR without filing Form 10E?

Your ITR will still be processed, but the relief claimed will not be allowed, and you may receive a notice from the tax department.

3. Is there a separate due date for Form 10E?

There’s no fixed standalone due date, but it must be filed before you file your Income Tax Return for that assessment year.

4. Do I need to submit Form 10E to my employer?

No. You only need to submit it on the income tax e-filing portal. However, it’s a good idea to inform your employer if you’re claiming this relief, since it can also affect how much TDS they deduct from your salary.

5. Can I claim relief under Section 89(1) under the new tax regime?

Yes. The relief is available under both the old and new tax regimes.

6. What is Form 39, and does it replace Form 10E?

Form 39 is the new version of Form 10E under the Income Tax Act, 2025, applicable from Tax Year 2026-27 onwards (for returns filed in 2027 and after). For AY 2026-27 (the return due by 31 July 2026), you still need to use Form 10E.

7. What if my arrears relate to multiple past years?

You can include details for each relevant year in the relevant annexure, the portal calculates the tax difference year-wise and arrives at the total relief.

Key Takeaways

- Section 89(1) protects you from paying extra tax just because past income (arrears, gratuity, advance salary, termination pay, or commuted pension) was paid to you in a lump sum.

- Form 10E is how you formally claim this relief, and it’s mandatory, online-only, and must be filed before your ITR.

- Relief is only available if the bunching of income actually increased your total tax liability.

- For AY 2026-27 (return due 31 July 2026), continue using Form 10E. Form 39 takes over only from Tax Year 2026-27 onwards under the new Income Tax Act, 2025.

- Keep your past Form 16s and salary records handy, they make the filing process much faster.

Sources:

Income Tax Department, Government of India – Form 10E User Manual; Income Tax Department – Income Tax Forms FAQs; Income Tax Department – Income Tax Returns FAQs; Business Standard, “Use Section 89(1) to reduce tax burden arising from arrears: Experts.”

Disclaimer

This article is for general information and does not constitute tax advice. For your specific situation, consult a chartered accountant or tax professional.